SWISS PORTFOLIO

September 2025 Results

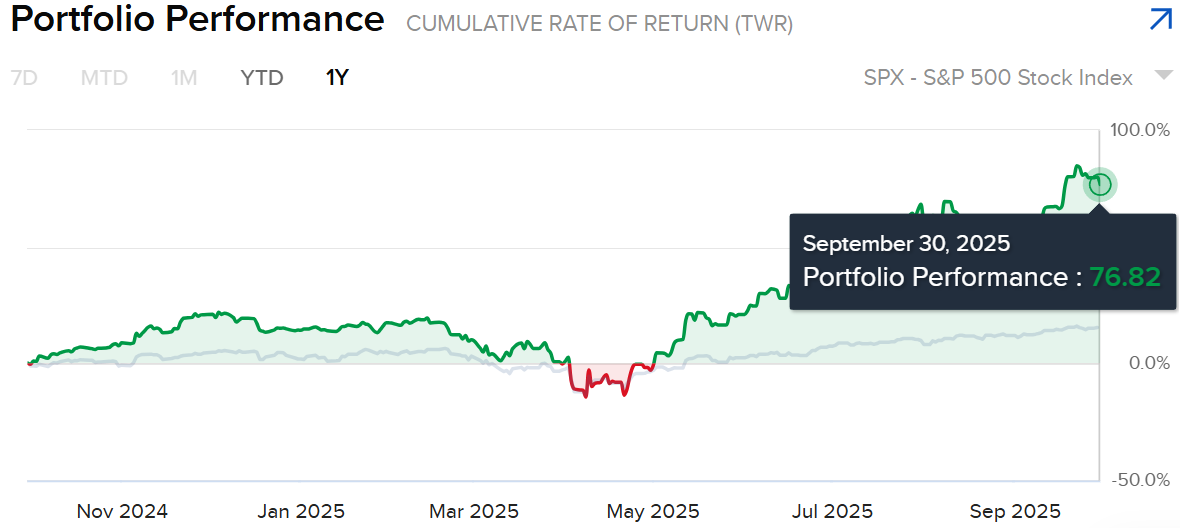

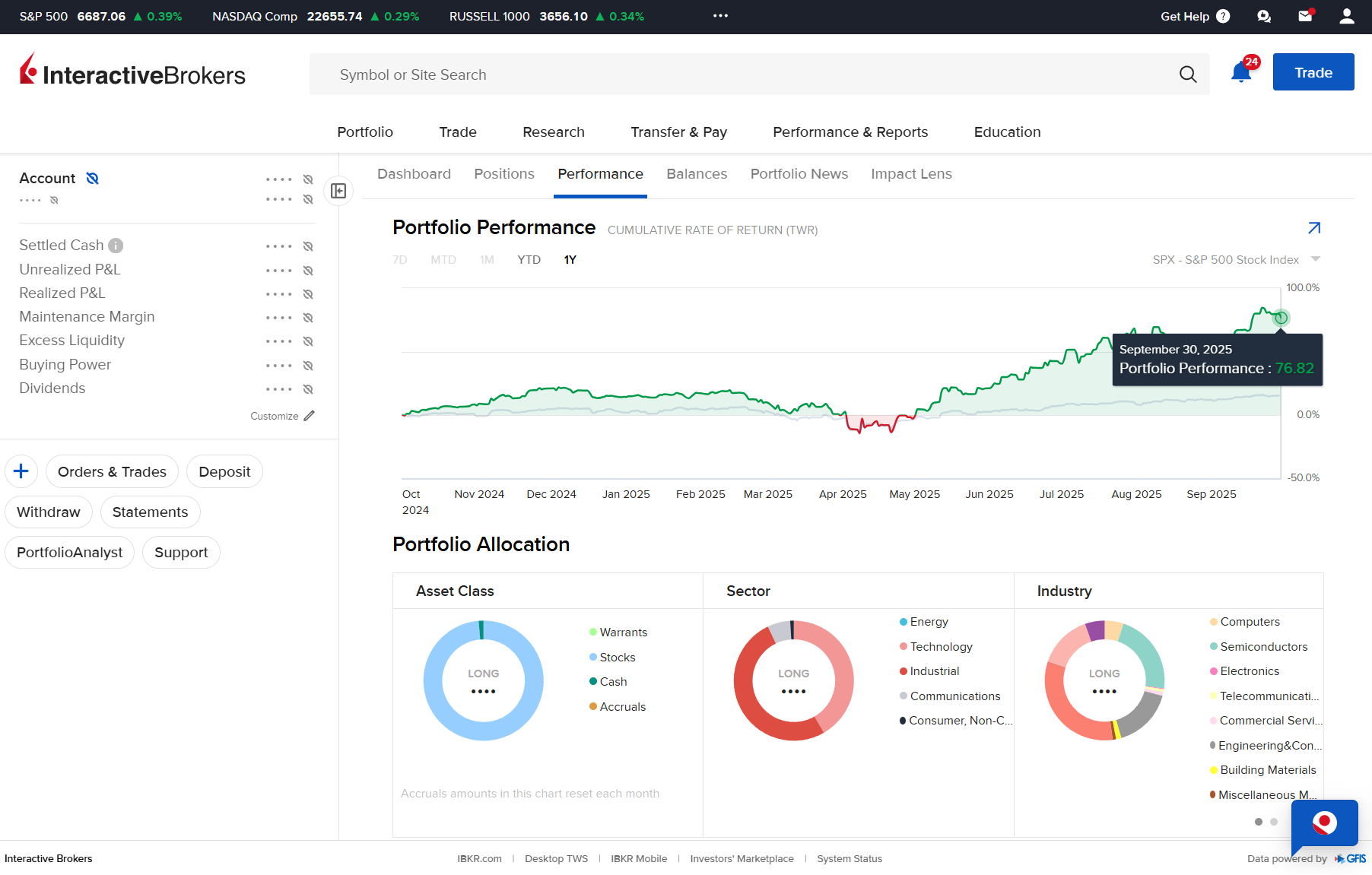

Portfolio Performance

Let’s start with a wonderful scoreboard:

August 2025 YoY Returns: +61.97%

September 2025 YoY Returns: +76.82%

Swiss Portfolio unchanged since August 7.

Last Swiss Portfolio changes were made in August 7, when we executed 2 trims and a new entry. Since then? We simply let the portfolio work, and it did. Up another +14% in a month, peaking at +85% before settling at +76%.

That’s 5-6x the S&P 500, shown directly from our IBKR account. Not just fancy graphs or beautiful hard-to-believe tables.

And these returns come with zero leverage, no derivatives, no exotic strategies. We do occasionally highlight special situations that can deliver fast-fat gains, like this one:

But the Swiss Portfolio’s core engine is, and will remain, a cautious Swiss risk-reward allocation.

September brought plenty of noise: the Fed cut 25 bps to 4.00-4.25% and telegraphed two further cuts this year (implying a terminal range near 3.50-3.75%), which would add a healthy tailwind for both our positions and equities broadly. Swiss discipline remains our compass, but momentum is clearly on our side.

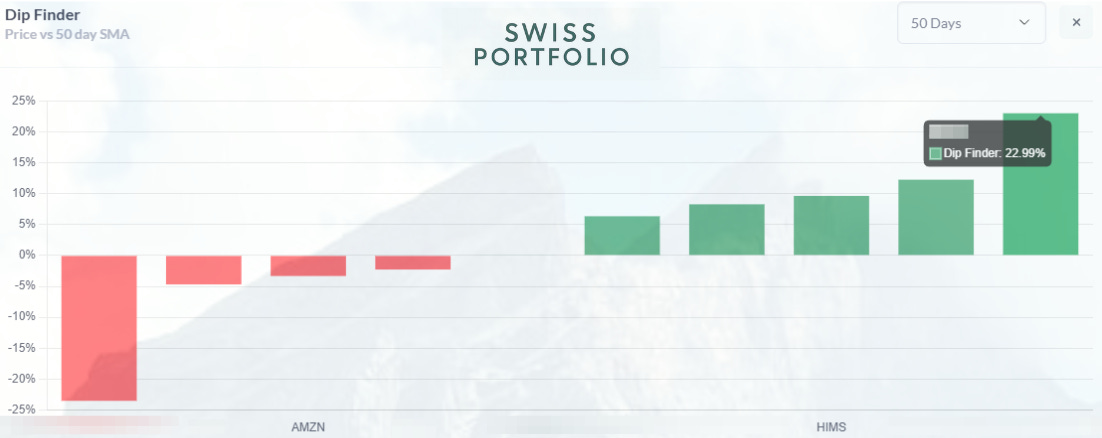

The post-earnings season results were clear: our 11 holdings delivered stronger outcomes than ever. Half cooled off under the 50-day SMA, half sprinted above it. Translation? Amazon is quietly setting up the next asymmetric shot, while HIMS, for instance, continue running hot. Exactly the kind of barbell structure we like.

The chart below illustrates how our returns maintain a dramatic lead versus the S&P 500, over 6x in relative performance. It’s yet another validation of our focus on high-conviction ideas. But, as always, we proceed with measured optimism and discipline.

In this write-up, we’ll walk through how each of our 11 holdings fared in September, while maintaining our mission unchanged:compound capital far above the market, and share every step, wins and setbacks, with full transparency.

Index:

Transparency & Skin in the Game

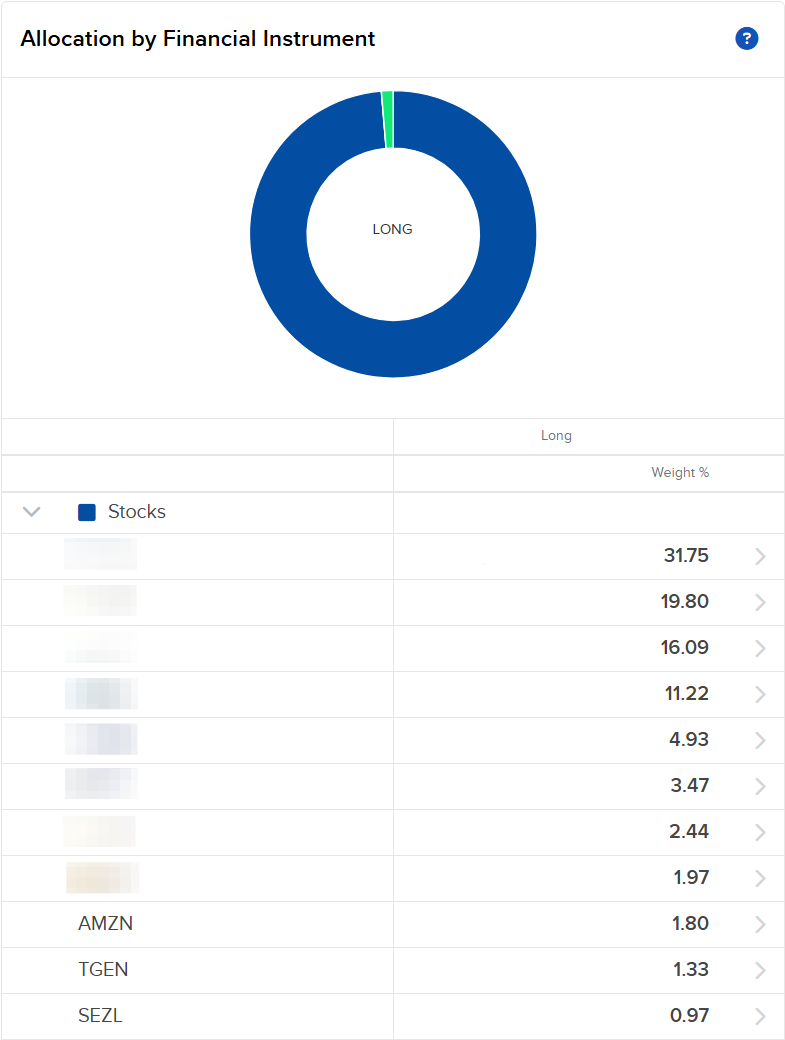

Top 11 Holdings Recap

Portfolio Allocation & Structure

Entry Prices

Strategy & Positioning Update

Transparency & Skin in the Game

In finance, credibility is everything. Too often we read bullish market commentary from analysts who never show their cards, no portfolio disclosures, no real “skin in the game”, all while charging three-figure annual memberships or selling courses. At Swiss Portfolio, we think differently. We show our cards. Every month, we publish a full portfolio update, sharing exactly where our capital is deployed and, more importantly, why. And we do it for a symbolic $39.99 annual fee, not as a profit center, but as a way to justify the work and keep delivering value. Our goal is simple: more transparency, more substance, and more value than most three-figure memberships, but at a fraction of the cost.

Our allocation snapshot (see next picture) reflects that philosophy in action. Two of our earliest Equity Research ideas, $PSIX and $IESC,

have evolved into concentrated bets within a deliberately concentrated portfolio. We’ll break down the full structure in the next chapter, but the message is simple: we don't just write about high-conviction ideas, we back them. Visibly. Publicly. This is real skin in the game. At Swiss Portfolio, we practice what we preach.

Top 11 Holdings Recap

#11 🔻 SEZL (~0.97% allocation): Our smallest holding but perhaps the wildest ride. You can revisit our full research and Financial & Valuation Model inside:

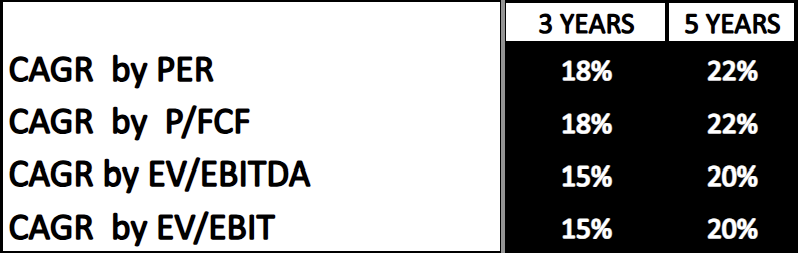

The stock is +80% YTD, and -13% since our research and entry position around 1% allocation.

If you bet the story will keep compounding at the same pace over the next 5 years, you’re targeting a +20% CAGR at current levels.

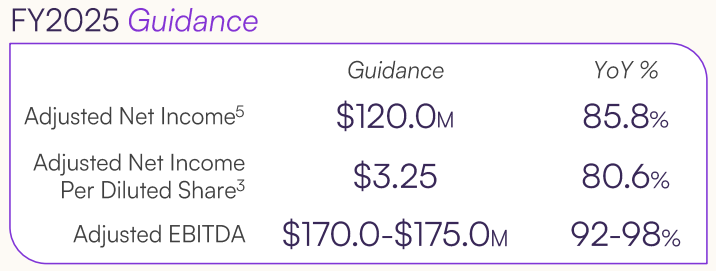

This BNPL upstart surprised skeptics with ~76% revenue growth in Q2 and even raised its full-year guidance, backing it with a hefty $125 million share buyback plan, a bold move that telegraphs management’s confidence in future growth.

Still, September reminded everyone that high-flyers don’t move in straight lines. Sezzle’s shares got caught in a risk-off downdraft and short-term sentiment turned sour on fintech. Adding fuel, the market seems to be bracing for the uncertain outcome of its legal trial with Shopify, a shadow that could overhang valuation until resolved.

But we’re focused on the fundamentals: a scrappy fintech with positive cash flow (TTM free cash flow margin ~18%) and an aggressive shareholder return strategy. Volatility aside, Sezzle is executing beautifully. If the market keeps discounting the name on sentiment and legal fears, we’ll happily hold, turbulence is often the price of a wonderful asymmetric setup worth monitoring.

#10 🔺 TGEN (~1.33% allocation): You can revisit our full research and Financial & Valuation Model inside:

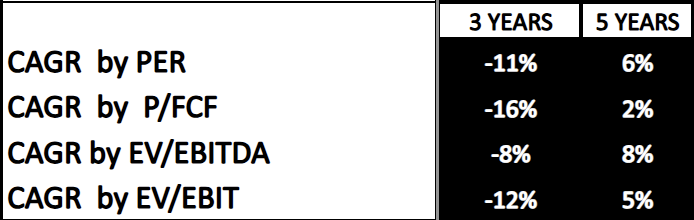

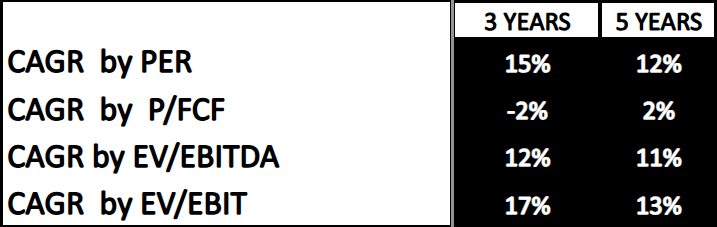

After the recent stock price hike, re-running the numbers at $8.81 per share, assuming uncertain but meaningful revenue growth, margin improvement, and a fair multiple, yields a modest ~5% CAGR over the next five years.

This idea undoubtedly carries more risks than certainties, but with an initial position of less than 1%, one that is gaining momentum and could be scaled over time, the setup may surprise on the upside. And if the current letters of intent (LOI) ultimately materialize, the outcome could be very explosive.

Until that happens, or until the price offers a wider margin of safety, TGEN will remain a speculative position: high risk, but with potentially outsized reward.

For a company straddling clean energy and AI-era infrastructure (their chillers to cool data centers), that is a wonderful place to be with a 1% position for us.

#9 🔻 AMZN (~1.80% allocation): You can revisit what we forecasted before earnings season in July, with our full research and Financial & Valuation Model inside:

Rerun the numbers today, with conservative growth, modest margins, and a fair multiple, and Amazon still points to a +10% CAGR over the next 5 years. Not spectacular in a bull market, but in an indestructible, incredible business with unmatched scale and optionality, that math is more than enough.

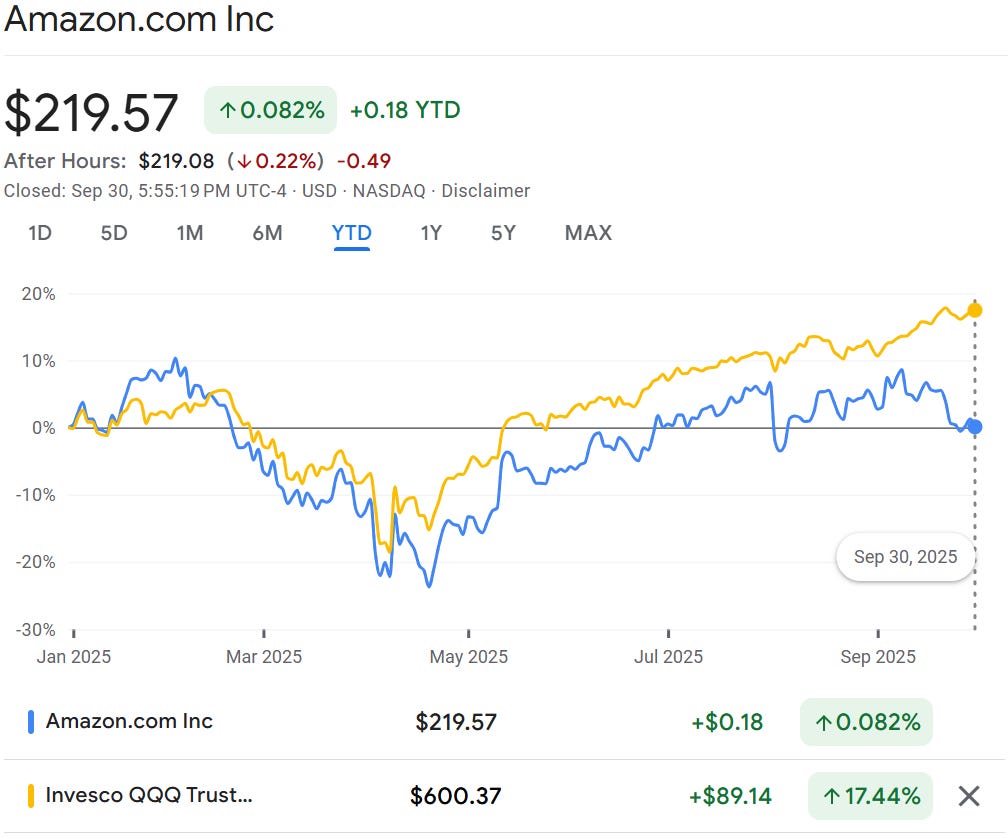

The truth is Amazon has gone nowhere this year, flat, while its tech peers in the QQQ marched ahead with +17% YTD gains.

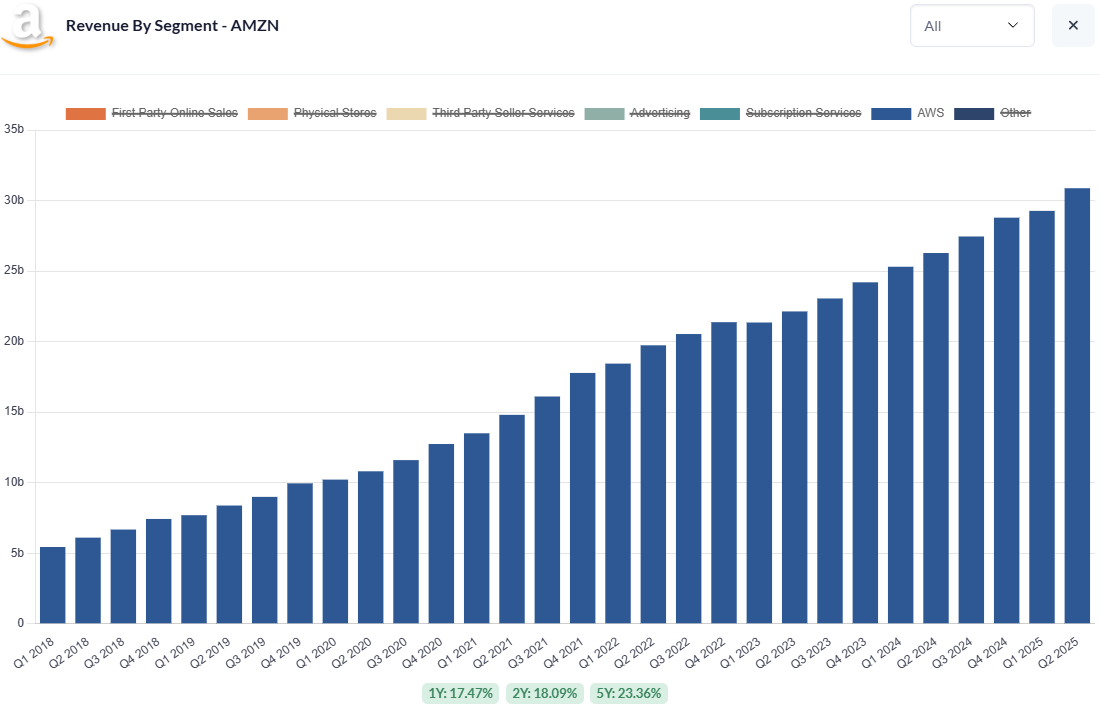

The market punished Andy Jassy’s Q2 comment on AWS growing slower than Microsoft and Google Cloud, and the stock dipped after July 31. But calling AWS “slower” is misleading. It still grew ~17.5% YoY to nearly $31B in quarterly revenue, the law of large numbers, not a broken engine.

Where Amazon stands apart is breadth. While Azure boasts deep penetration into the Fortune 500 (≈85%), AWS serves a broader and more diversified base, more than a million customers across startups, SMBs, and enterprises. That’s a bigger funnel, less concentrated risk, and more durable growth. The narrative that AWS lags its competitors misses this fundamental truth: its reach is unparalleled.

Then comes the optionality stack. Amazon’s in-house chips, Trainium and Inferentia, are quietly cutting the cost of AI workloads and are already embedded in AWS offerings.

Its logistics network, now powered by over a million robots, is being rewired with AI, squeezing delivery times and costs in ways that competitors simply cannot replicate.

Zoox, Amazon’s autonomous vehicle bet, is already live on the streets of Las Vegas in pilot rides.

How long until it moves both passengers and packages without a driver? Add to that the advertising engine, $15B+ in quarterly revenue, growing over 20% YoY, with Prime Video ads now expanding globally, and you see how Amazon keeps building new profit levers inside an already massive ecosystem.

And then there’s Prime. Think of it less like a membership and more like a habit. Over 220M households worldwide interact with it daily and weekly: commerce, video, music, delivery. Like Netflix or Spotify, it’s recurring lifetime value, but tied to essentials rather than entertainment. And none of these surfaces, whether retail, streaming, or ads, are close to fully optimized.

Re-run our numbers with conservative growth and margin assumptions, and you still get a +10% CAGR over the next five years. That might sound boring compared to AI moonshots, but boring compounding at Amazon scale is anything but. While the market remains indifferent for now, the fundamentals point to expanding capacity, proprietary chips, robotics, advertising, and autonomy. Amazon is not a case of missed growth, but rather the beginning of a new margin expansion cycle, one that is already taking shape beneath the surface.

When you’re the market leader and you’re still operating with a “Day 1” startup mindset, it’s a potent combination. We’re content to keep Amazon as one of our positions, it provides stable exposure to AI and automation at scale. If the market wants to fret over AWS growth rates, we’ll happily hold (and potentially add on more dips). Amazon’s structural moat, the world’s largest robotic workforce, unparalleled data/compute infrastructure, and an ecosystem that touches 200M+ Prime subscribers, makes it one of the best-positioned companies for the AI era, period.

Big news at Swiss Portfolio

Enjoying these portfolio updates?

Full access is just $39.99/year, less than a Swiss train ticket & more value and transparency than most $300+ memberships out there.

💥 2025 Special: Join this year and lock in $39.99/year for life. No future price hikes, your rate stays fixed forever. Don’t miss it. Click the button above.

Over the past 12 months, our portfolio has returned close to 6x the S&P 500, and we publish every move with full transparency. In a world where most of finance hides behind paywalls and vague claims, we do things Swiss-transparently.

That’s not by chance. It’s the result of deep research, disciplined capital allocation, and a focus on durable, capital-light compounders, with strong management, sector tailwinds, and attractive valuations, often well before they’re widely recognized.

Become a member and you’ll gain full access to:

✅ Full access to Swiss Portfolio positions + monthly allocation updates.

✅ At least 1 high-conviction Equity Research every month.

✅ Downloadable financial models to follow and stress-test each thesis.

✅ Live idea tracking once they spike, plus an S&P tracking template.

✅ Exclusive Swiss-based insights on investing, residence, and tax optimization.

✅ Special Situations: asymmetric opportunities, arbitrage plays and odd-lot tenders.

🧠 The $39.99 subscription pays for itself a few times over, sometimes in just one Equity Research idea. This isn’t about hype. It’s about transparency, consistency, and long-term compounding.

If you share our philosophy of identifying scalable compounders in high-quality jurisdictions backed by durable megatrends, we strongly encourage you to explore how past ideas have performed (current date 2.10 before market open) :👇

Incredible name so far, right? Want to see our Top 8? These are the concentrated bets truly driving Swiss Portfolio performance. Become a member and support our work for just $39.99/year, offering more value and transparency at a fraction of the cost of most three-figure memberships. For our early members, Join in 2025, and we’ll lock you in that price for life.

💥 2025 Special: Join this year and lock in $39.99/year for life. No future price hikes, your rate stays fixed forever. Don’t miss it. Click the button above.

🚀 Coming soon on the Substack:

👉 In upcoming posts, We’ll cover:

Research collaborations with other incredible writers here on Substack.

More strategies to track your finances and build a clear 5-year financial plan.

How to optimize taxes when investing from Switzerland, a huge advantage vs US & EU.

Continued Equity Research on asymmetric opportunities we’re tracking, including my recents Azeus deep dive, Tetragon deep dive or Sezzle deep dive.

The “move to Switzerland” playbook for investors and entrepreneurs (paid).

The Sentiment tracker of our holdings and watchlist (Monthly, paid).

The Swiss Portfolio allocation strategy, which has returned 60%+ in a year and 30% CAGR over the past 5 years (Monthly, paid).

Why members joined us?

We’ve crossed 1,000+ members, apparently, Swiss discipline and transparency still sell. Every day, more investors join, finding real value in our best-in-class Equity Research and high-quality updates. Cautious risk-reward, asymmetric upside, just Swiss Portfolio style.

🫶 A huge thank you to everyone who’s already supporting the project in its early stages, whether through a subscription or the symbolic $39.99 annual fee. Your trust makes this possible and keeps us motivated to continue sharing deep research and strategic thinking over time.

The goal is simple: to consistently beat the S&P 500 through high-conviction investments, executed with discipline, backed by data, and aligned with the Swiss mindset: careful risk, long-term focus and best-in-class quality.

📬 Read us. Join us. Sleep well.📈✨

Keep reading with a 7-day free trial

Subscribe to Swiss Transparent Portfolio to keep reading this post and get 7 days of free access to the full post archives.