West Pharmaceutical Services ($WST)

A Moat Built on Rubber and Regulations

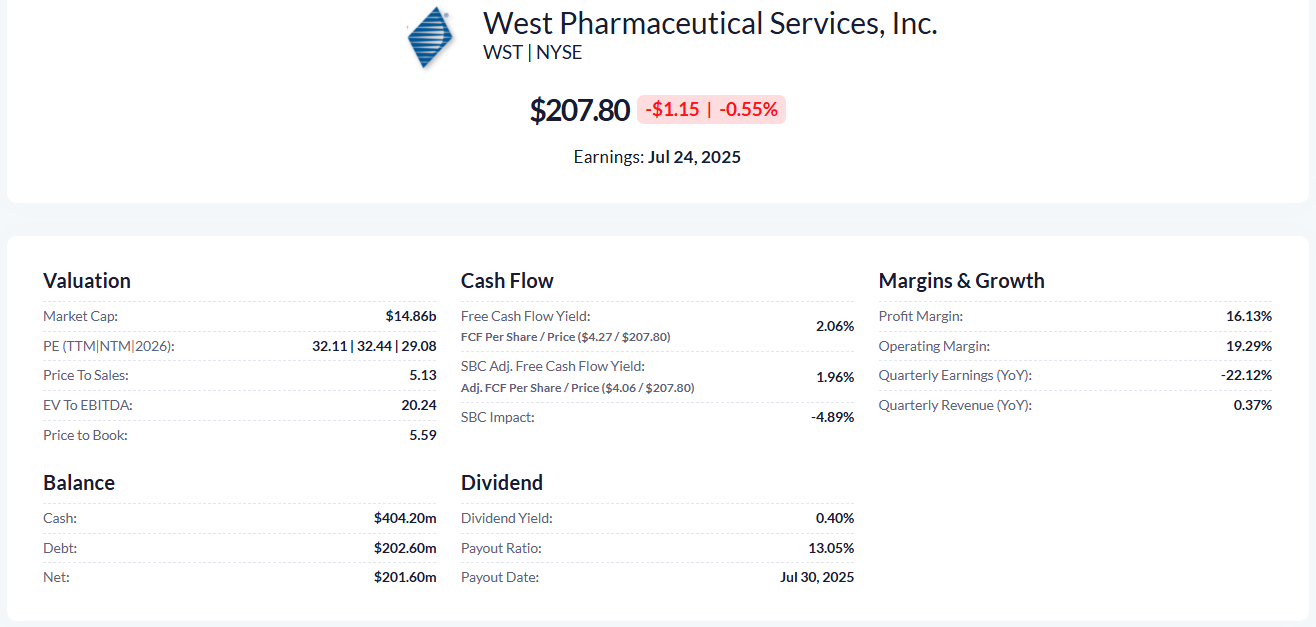

Sentiment: Attractively priced ✅. West Pharmaceutical Services ($WST) is a century-old market leader in injectable drug packaging and delivery components, with dominant market share, deep customer entrenchment, and promising long-term growth drivers. Near-term headwinds (post-pandemic inventory unwinding, currency swings) have bruised recent results – and the stock price – providing a potentially attractive entry point. Despite a rich valuation, West’s strategic positioning and strong moat justify a bullish long-term view, albeit with eyes open to risks.

1/8 Investment Thesis at a Glance

Dominant Market Position: West commands an estimated ~70% share of the global elastomeric components market for injectable drug packaging. Its nearest competitors (e.g. Swiss firm Dätwyler, and Aptar Group) remain distant seconds, as West’s century of expertise, high-quality reputation, and regulatory embeddedness create formidable barriers to entry.

Robust Moat: Pharmaceutical clients are extremely hesitant to switch packaging suppliers due to strict regulations and the costly re-validation process (the Drug Master File lock-in) required for even “commodity” components. This gives West a sticky customer base and pricing power for its critical yet low-cost healthcare components.

Secular Growth Drivers: The proliferation of biologic drugs, vaccines, and injectable therapies (e.g. the booming GLP-1 obesity/diabetes treatments) underpins steady long-term demand for West’s products. West is even the world’s largest manufacturer of insulin auto-injectors, positioning it to benefit from surging use of injectable biologics. Additionally, pharma companies increasingly outsource high-value processes (like sterile packaging and self-injection devices) to West, expanding West’s value-add per unit. It is estimated West controls ~60% share in this fast-growing self-injection device segment, as mentioned critical exposure to GLP‑1 and biologics tailwinds.

Financial Resilience and Shareholder Returns: While 2024 saw a dip after two years of pandemic-fueled highs, West still delivered nearly $2.9B in sales with healthy profitability.

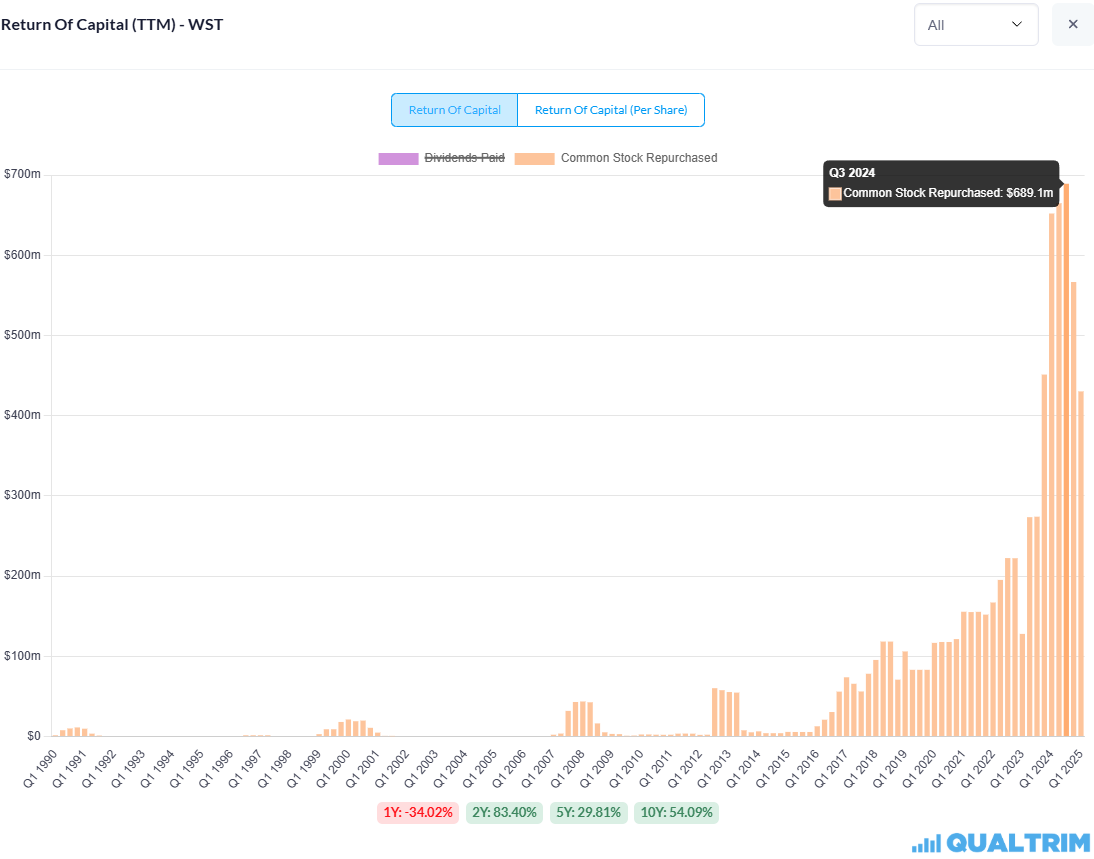

The company has a strong balance sheet and generates solid cash flows, funding buybacks and dividends. It has paid 217 consecutive quarterly dividends since 1970 (albeit at a modest current yield) and opportunistically repurchases shares (e.g. > $0.6M in shares repurchased in Q3 2024 alone).

This shareholder-friendly capital allocation, combined with management’s own stock ownership requirements (CEO must hold 6x base salary in stock), suggests decent alignment with investors.

Valuation and Upside: After a sharp sell-off, WST trades around $208 per share (~32x trailing earnings). That multiple, while not cheap, is at the low end of West’s historical range for its growth profile. With destocking pressures easing and high-margin products resuming growth, earnings should rebound beyond 2025. We view West as a high-quality franchise worth accumulating for the long haul.

2/8 Company Overview – A Century-Long Monopoly in Drug Delivery Infrastructure

West Pharmaceutical Services has quietly become the unsung hero behind billions of injections and vials. Founded in 1923, West spent a century mastering the art and science of rubber stoppers, seals, plungers, syringes, and other containment and delivery components that ensure drugs remain safe and effective until they reach patients. These may be humble widgets, but a single low-quality stopper can ruin an entire batch of life-saving medicines. Pharma companies know this, and most trust West above all to get it right.

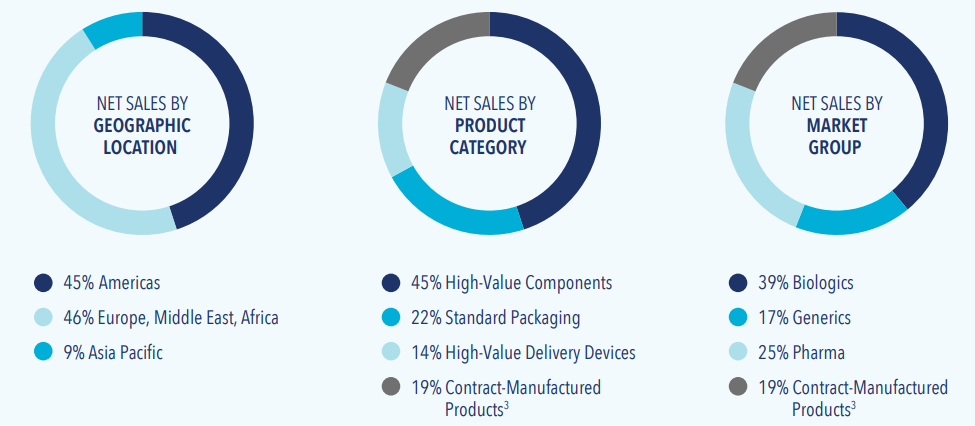

Today West’s business is divided into two big blocks: Proprietary Products (roughly 80% of revenue) and Contract-Manufactured Products (~19%). The Proprietary segment covers West’s own catalog of primary containment solutions and delivery systems – everything from basic rubber vial stoppers to high-tech self-injection devices and packaging. The Contract Manufacturing segment, by contrast, is when West is a behind-the-scenes maker of devices designed by pharma or medtech clients (for example, auto-injector pens that a drug company patented).

West’s Proprietary Products drive the lion’s share of profit and growth. This includes standardized components sold in huge volumes (over 40 billion pieces annually) as well as premium offerings that go through additional processing for higher quality. Over the past decade West has deliberately moved up the value chain: instead of just selling raw rubber bits, it increasingly washes, sterilizes, coats, inspects, and even pre-fills or integrates components for customers. Each extra step raises West’s share of the value (and margins) while saving big pharma the hassle. For instance, a plain rubber stopper (~$0.02 average selling price) might carry ~13% gross margin, whereas a high-end coated and sterilized stopper (e.g. Westar® RU or NovaPure®) at ~$0.30 ASP can earn >50% margin. And a complex wearable injector device (West’s SmartDose®) might sell for ~$100 with ~60% margin. The strategy: make West’s offering increasingly indispensable, yet still a tiny fraction of the drug’s cost – so pharma gladly pays up for the assurance of quality and convenience. As West noted,

“the cost of West’s components is a rounding error in the final drug price, but the drug’s quality cannot be jeopardized”.

This is a beautiful pricing dynamic for West.

By contrast, Contract Manufacturing is a lower-margin, service-oriented business – basically acting as a reliable third-party manufacturer for client-owned designs.

Still, it has its bright spots: West’s trusted manufacturing know-how makes it a partner of choice for complex devices. For example, West produces auto-injector pens for several insulin and biologic drugs (the company is the top producer globally of such pens), which ties West into the megatrend of rising biologics and new injection therapies. In Q1 2025, West’s Contract Manufactured segment actually saw increased orders for self-injection devices for obesity and diabetes treatments – a nod to the explosive growth of GLP-1 drugs (like Novo Nordisk’s Wegovy and Ozempic) that require sophisticated delivery pens. This segment’s revenue grew slightly in Q1 to $135M while proprietary product sales were ~$563M, underscoring that West’s future is still predominantly in its proprietary innovations, but contract work can augment growth in key areas.

Geographically, West is truly global: in 2024, 55% of sales came from outside the U.S.. Europe and Asia are significant markets, and West keeps expanding its footprint to be close to customers. For example, it recently opened a new facility in South Korea to serve local pharma, and it’s investing in Ireland with new manufacturing lines in Dublin operational since 2025. These investments should bolster capacity and reduce supply chain bottlenecks as demand grows.

3/8 Financial Performance – Near-Term Pain, Long-Term Gain

After a pandemic-fueled boom in 2020–2021, West’s financials have hit an air pocket – but the turbulence looks temporary. FY2024 (the year ended Dec 31, 2024) saw Net Sales of $2,893.2 million, a 1.9% decline from 2023.

This drop was primarily due to a decline in High-Value Product (HVP) sales as certain pharma customers worked down excess inventory built up during COVID.

It’s telling that one major customer accounted for ~10.9% of West’s sales in 2023 – likely related to COVID vaccine components or a big biotech – and that customer significantly curtailed orders in 2024. The hangover was evident in profits: Gross Profit fell 11.6% to $998.5M (gross margin down to 34.5% from 38.3% in 2023), reflecting lower factory utilization and an unfavorable product mix (fewer high-margin HVP orders). Operating Profit dropped 15.7% to $569.9M, and Net Income came in at $492.7M, down from $593.4M in the prior year. On the bottom line, EPS for 2024 was $6.69, a ~15% drop from $7.88 in 2023. In short, 2024 was a rare step backward for West, a company that typically posts steady growth.

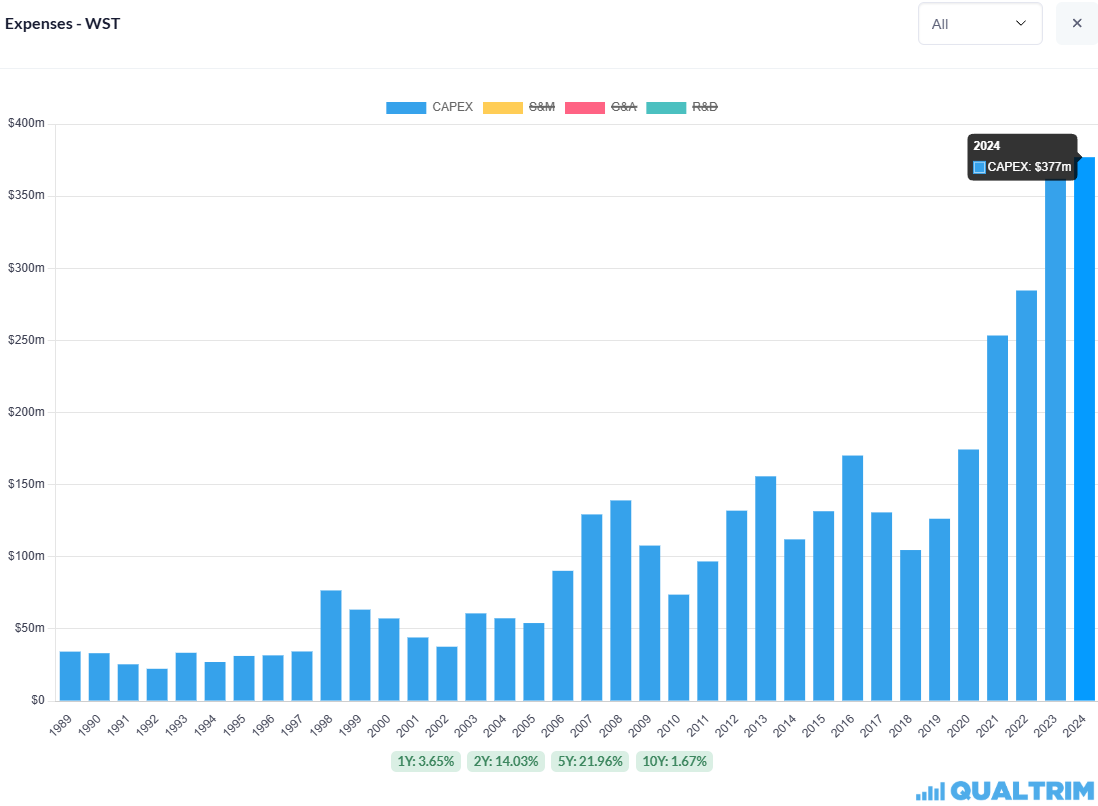

Management’s commentary attributed the dip to transitory issues – chiefly, order “destocking” by customers and foreign exchange impacts – rather than any structural loss of business. In fact, demand for newer products remained healthy: West noted strength in areas like cartridges and syringes for injectable therapies (think GLP-1 and other biologics) picking up in late 2024. The company continued to invest in capacity expansions (capital expenditures rose) to prepare for the next wave of growth, even as short-term volumes lagged.

This cautious optimism started to bear out in the most recent quarter. Q1 2025 results showed net sales of $698.0M, basically flat (+0.4%) year-on-year, but slightly better than many feared given the tough prior-year compare. Encouragingly, on a constant-currency organic basis sales grew ~2.1%, indicating underlying demand is returning. The sales mix also hinted at stabilization: Proprietary segment revenue ticked up +0.6%, while Contract Manufacturing was only down -0.7%. This is a marked improvement from 2024 when proprietary HVP sales were shrinking; by early 2025, those declines have largely bottomed out.

Earnings in Q1 remained under pressure – reported EPS was $1.23, down from $1.55 in Q1 2024 – a 21% drop reflecting still-soft margins. The adjusted EPS was $1.45, backing out certain one-time items, so the core profitability decline was somewhat milder. Management pointed to lingering cost inflation (e.g. wage and material costs) and the fact that some high-margin product lines have yet to fully bounce back. Net income for Q1 was $89.8M, down 22% year-on-year, leaving profit margin around 13% vs 17% a year prior. These numbers aren’t pretty – but the market was already braced for even worse.

Crucially, West raised its full-year 2025 guidance after seeing Q1 trends. The company now projects 2025 net sales of $2.945–2.975B (midpoint ~$2.96B), up from a prior outlook of $2.875–2.905B. Likewise, adjusted EPS guidance was lifted to $6.15–$6.35 (from ~$5.90–$6.20 initially). The guidance hike is modest in absolute terms, but it signals a corner is being turned. It also partially undoes the damage from February, when West’s initial 2025 forecast badly undershot Wall Street’s expectations and sent the stock into a tailspin. Back then, West guided to ~$2.89B revenue and ~$6.10 EPS at the midpoint – a ~5% miss on sales and ~20% miss on EPS vs consensus. The CEO explicitly cited “clients reducing inventory levels” as a key factor in the soft outlook. That news hammered WST shares ~18% in one day (and over 30% from its 2023 highs), as the market recalibrated growth expectations. With Q1’s bump in guidance, West is effectively saying the worst of the destocking pain is likely over.

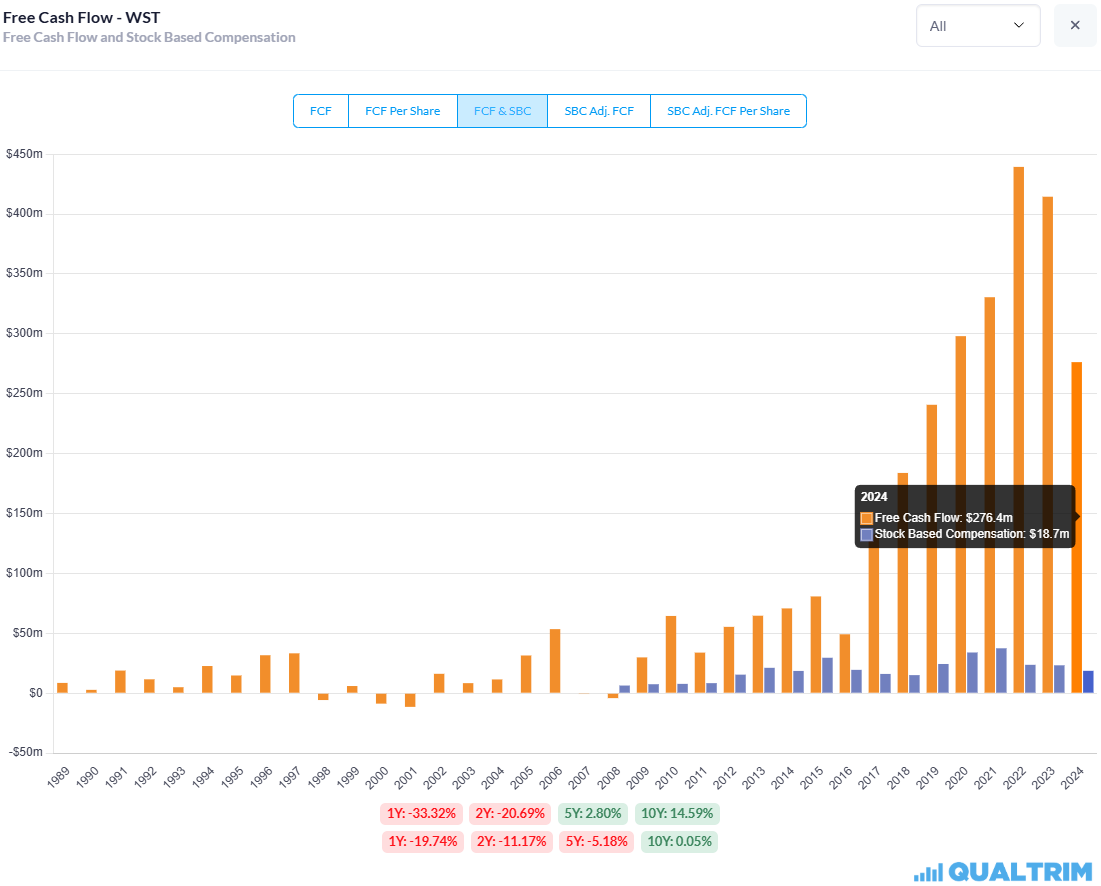

Even at the low point of this cycle, West remained solidly cash-generative. Operating cash flow in 2024 easily funded capital investments and dividends.

West’s balance sheet carries manageable debt (its leverage is modest, with interest coverage very high given its consistent EBITDA). The company returned cash via $133.5M of share buybacks in Q1 2025 alone, taking advantage of the depressed stock price (~$242 average cost per share, a savvy move in hindsight). As a result of buybacks, the share count has shrunk ~2.2% year-on-year – one reason Vanguard and BlackRock’s ownership percentages ticked up despite holding the same number of shares (more on that below). West’s dividend is a token ($0.21/quarter, <0.5% yield) but importantly has never been cut in 53+ years. Management clearly prioritizes maintaining that dividend streak – a nice signal of stability, even if investors mostly prize WST for capital appreciation.

Looking forward, if we normalize past the Covid hangover, West’s growth prospects appear intact. In the latter half of 2023 and into 2024, demand for West’s high-margin offerings (like NovaPure stoppers and injectable device components) began climbing again as pharma customers moved past destocking and resumed new project orders. Meanwhile, entirely new growth avenues are emerging: for example, West’s Crystal Zenith® line (polymer vials and syringes as an alternative to glass) and its partnership on self-administration systems (SmartDose) cater to cutting-edge biologics and gene therapies. These should support mid-single to low double-digit revenue growth over the next several years, with an added kicker if West’s operating margins recover back toward the high-30s percentage (from ~34% in 2024) as volume leverage improves. In short, the long-term margin expansion story remains intact – 2024’s dip looks like an aberration in an otherwise steady upward trajectory.

One might quip that West’s 2024 was “a year of giving pharma clients a breather” – but those clients won’t pause for long. The pipeline of injectable drugs is growing, not shrinking, and every new therapy that requires an injection or specialized containment adds to West’s addressable market. West’s financial history shows consistent growth barring shocks, and the current slowdown appears to be just that: a transitory shock, not a new normal. As inventory dynamics normalize and new capacity comes online, West is poised to resume compounding its revenues and earnings. With the stock still recovering from its recent battering, the valuation (EV/EBITDA and P/E) looks reasonable for a wide-moat business of this caliber.

4/8 Strategic Initiatives & Growth Drivers - Innovation in the Bloodstream

West might sell “shovel” products to the pharma gold miners, but it certainly doesn’t stand still. The company has several strategic initiatives to ensure it remains the supplier of choice as the pharma industry evolves:

Product Innovation: West is constantly developing new and improved containment and delivery solutions. Recent years saw the launch of Westar® Select and NovaPure® high-quality stoppers, which offer reduced particulates and improved purity for sensitive biologics. West also introduced new accuShield™ plungers and other components designed for advanced auto-injectors. In 2024, management highlighted “new products that provide greater packaging flexibility” coming to market. Additionally, West is investing in smart dose delivery systems (like its SmartDose wearable injector that adheres to a patient’s body for slower drug delivery) to cater to next-gen therapies. These innovations not only meet emerging customer needs but also tend to carry higher margins than legacy products, reinforcing West’s profitability moat.

Capacity Expansion: To keep up with demand (and to enable customers’ growth), West has several expansion projects underway. In Dublin, Ireland, West has build out a new plant focused on proprietary products. This will support European and global customers, especially for high-value components. The company is also expanding facilities in Pennsylvania and North Carolina (adding cleanrooms and manufacturing lines) to boost output of its injectable component lines. Even contract manufacturing is growing – West recently expanded capacity at its Ireland contract manufacturing site, adding 100 jobs over five years. By investing ahead of the curve, West aims to avoid being a bottleneck for clients (during the pandemic, certain components were on allocation due to industry-wide shortages). The flipside is temporarily higher CapEx, but West’s balance sheet can handle it, and these investments should earn solid returns given high utilization rates once the pharma cycle picks up.

Geographic Broadening: West is deepening its presence in Asia and other emerging markets where pharma production is rising. The new sales office and warehouse in Seoul, South Korea (opened 2024) is one example. West has also talked about expanding in China (despite geopolitical tensions, China’s biopharma industry is a growth opportunity). West’s strategy is to be closer to customers for both sales and distribution – given the critical, time-sensitive nature of drug manufacturing, local support can be a differentiator. International markets already form over half of West’s revenue and will likely grow further as regions like India and South America develop more vaccine and biologics manufacturing capacity (all of which need West’s components).

Service & Quality Enhancements: Part of West’s moat is its best-in-class quality and technical support. The company continues to beef up its technical support teams, R&D labs, and regulatory expertise to assist customers in drug development and compliance. For instance, West offers analytical lab services to help pharma companies test drug-container compatibility. It has also implemented digital initiatives like West SmartTray™ (an RFID-enabled system to track components). These “extras” may not directly show up as separate revenue streams, but they cement customer loyalty. It’s notable that West often collaborates with customers in the early stages of drug development – essentially locking itself in as the specified supplier by the time the drug hits commercialization. The earlier West is involved, the less likely a competitor can displace it.

ESG and Sustainability: In a traditionally industrial business, West is making efforts on sustainability (reducing waste in manufacturing, increasing recyclability of components, etc.) and social responsibility. While not a direct financial driver, West’s focus on environmental and product safety standards further endears it to big pharma clients who have their own ESG goals. For example, West has introduced formulations that are free of certain chemicals and increased transparency about its supply chain. This is more “hygiene factor” than differentiator, but it reduces risk of falling behind regulatory trends and keeps West aligned with its customers’ values (and by extension, their continued business).

Overall, West’s initiatives reflect a company not content to rest on its laurels (or its 70% market share). It is extending its technological edge, expanding capacity to capture growth, and entrenching itself ever more deeply with customers. West’s idea of complacency is spending tens of millions to make sure no one else gets even a whiff of their market. Just the kind of paranoia we like in an investment. The strategic moves reinforce that West intends to dominate its niche for the next decade as thoroughly as it has for the past one.

5/8 Competitive Landscape - In a League of Its Own?

Despite West’s commanding position, it does have competitors nipping at its heels. The major rivals fall into two categories: specialist packaging firms (like Dätwyler, Aptar) and integrated device/packaging providers (like Gerresheimer, Becton Dickinson in some areas, or Stevanato Group). How does West stack up?

Dätwyler (Switzerland) is perhaps West’s closest analog in elastomer components. It has strong technical expertise and supplies rubber stoppers and seals to pharma as well. However, Dätwyler’s market share is roughly 20–25%, a distant second to West. Many pharma companies use Dätwyler as a secondary source for redundancy, but West is often the primary specified supplier. Moreover, Dätwyler historically focused on standard components; West leaped ahead in high-end coated and sterile products. Dätwyler is trying to catch up (and has its own coated stopper line), but it lacks West’s scale and breadth of portfolio.

AptarGroup (USA) is a broader packaging company (cosmetics, food, etc.), but it has a healthcare division that makes injector devices, pumps, and some elastomeric packaging. Aptar’s ownership of Noble and other drug delivery tech gives it a footprint in auto-injectors and safety devices. Indeed, Aptar is mentioned as a formidable competitor in elastomeric expertise. Still, Aptar’s pharma segment is only a part of its business, whereas West is 100% focused on pharma/healthcare. This focus means West usually wins on deep regulatory knowledge and specialization. Aptar might compete on certain devices or niche offerings, but it doesn’t threaten West’s core vial stopper and seal franchise. If anything, Aptar’s success in devices confirms the growth in that area – which West is also pursuing with SmartDose and related systems.

Becton Dickinson (BD) is a giant in medical devices (and a legacy supplier of glass syringes). BD’s Pharmaceutical Systems unit produces billions of prefillable syringes and glass cartridges – things West doesn’t make (West supplies the rubber plungers for many of BD’s syringes). So BD is more of a partner than a competitor in many cases. However, BD has been eyeing the high-value stoppering and safety device space too. It launched its own coated stopper (via a venture with a competitor) and sells safety syringes and autoinjector devices. BD’s scale and deep customer relationships make it a potential competitive force, but BD’s attention is split among many product lines. West, being specialized, often out-innovates or out-supports BD on the packaging component front. Also, BD often collaborates with West (for instance, a pharma might buy a BD syringe with a West plunger and seal – a combined offering).

Stevanato Group (Italy) is an up-and-comer that went public recently. Stevanato is known for glass vials, syringes, and has been expanding into drug delivery devices and diagnostics. They even manufacture some components like plungers (often in collaboration with companies like Becton Dickinson). Stevanato’s sales (~$1B) are much smaller than West’s, but it’s growing fast. Stevanato’s strength in glass primary packaging complements West’s elastomers – in fact, the two sometimes partner (West provides the stoppers for Stevanato’s vials). That said, Stevanato could eventually try to internalize more elastomer component capabilities, or vice versa, West could expand further into polymer syringes (as with Crystal Zenith). For now, they play in related arenas with some overlap. West’s edge is again its dominance in the “rubber” domain and integrated solutions – Stevanato doesn’t yet have an equivalent to West’s NovaPure or SmartDose.

In sum, no competitor matches West’s comprehensive suite of products, global footprint, and entrenched regulatory status. West’s competitive advantages include:

Scale and Capacity: West’s numerous plants worldwide and high-volume output mean it can meet big orders reliably (a critical factor when a vaccine rollout is on the line). Smaller players can’t always scale as quickly or ensure supply in crises.

Quality Track Record: West has decades without major quality scandals. Pharma companies are conservative; they won’t drop a proven supplier lightly. Meanwhile, any competitor mishap (contamination, recalls) pushes clients more towards West.

Regulatory Embedding: West files Drug Master Files (DMFs) with regulators for its components, smoothing the path for customers to get drug approvals. Switching to a competitor’s component might mean amending filings – a nightmare pharma avoids unless absolutely necessary. Thus, West enjoys a quasi-annuity once specified in a drug’s regulatory filing.

Broad Portfolio & Innovation: Need a basic stopper for a cheap generic? West has it. Need a cutting-edge self-injection device for a $500k gene therapy dose? West has that too. Few rivals span this range. This breadth lets West cross-sell – a customer can solve multiple packaging needs through one vendor.

Customer Intimacy: Over 100 years, West built deep relationships with pharma and biotech firms. It often collaborates on R&D. Competitors that are newer or less specialized struggle to replicate that trust and intimacy with customers (which West calls “increasing levels of customer intimacy” as you move up to its most advanced products).

It’s worth noting that pharmaceutical industry trends tend to bolster West’s moat. Pharma companies are consolidating and also outsourcing more – meaning they want a few reliable, world-class suppliers rather than many fragmented ones. West’s ability to be a one-stop shop for many packaging needs positions it well as the preferred vendor as procurement gets more centralized. Additionally, cost is a relatively minor factor in competition: While West’s customers certainly negotiate hard, at the end of the day packaging cost is minimal relative to a drug’s value. As West candidly puts it, competition in its space is based primarily on design, quality, regulatory compliance, and technical expertise, “although total cost is becoming increasingly important as pharma companies pursue aggressive cost control”. In other words, West can’t price gouge, but it doesn’t need to be the cheapest – it needs to be the best. That’s a favorable competitive dynamic for a high-quality operator like West.

From an investor’s viewpoint, West operates in an oligopoly-like environment in its core niches. We expect it to maintain or even increase its share in the coming years, especially in high-end components, given the focus and reinvestment it’s making. Unless a competitor were to develop a truly disruptive new technology (or unless drug modalities shift massively, e.g. oral biologics replacing injectables someday), West’s castle should remain well-fortified.

6/8 Corporate Governance & Management Alignment - Some Quibbles, Mostly Good

West’s governance practices are largely standard for a mid/large-cap American industrial, with a few points of note. Eric M. Green, CEO since 2015, also serves as Chair of the Board – a dual role that some governance sticklers dislike. However, West does have a designated Lead Independent Director to counterbalance the combined CEO/Chair structure. The board appears to be composed of a diverse, experienced group of independent directors (with backgrounds in pharma, medical devices, finance, etc.), and refreshment has been ongoing. The most recent proxy (2025) shows a board of 9 independent directors plus Mr. Green, with an average tenure that isn’t excessive. The board’s focus on enterprise risk and strategy is highlighted in the proxy, detailing how they oversee management (for instance, the Board reviews the company’s five-year plan and risk portfolio regularly). All that suggests a reasonably engaged board.

From a shareholder alignment perspective, management’s incentives seem well-tuned to performance. Top executives have a mix of short-term cash bonus (annual incentive) tied to metrics like revenue growth, operating income, and ROIC, and long-term equity (PSUs, stock options) tied to multi-year goals and TSR (total shareholder return) vs peers. Importantly, West has share ownership guidelines – the CEO must hold stock worth 6x his base salary, and other executives 2x their salary.

As of the latest filings, Mr. Green far exceeds his requirement: he beneficially owns about 171,121 shares (vs 153,453 a year ago, including vested options/RSUs), which at current market value is nearly ~$35.6 million – roughly 30x his base salary. All directors and executive officers as a group own about 409,759 shares (vs 388,988 a year ago), which is <0.6% of the company but still a meaningful personal stake (worth ~$85M). While it would be nice if insiders owned more of the company, we take comfort that management is at least significantly invested in absolute terms. They feel the stock’s ups and downs in their own net worth, which tends to concentrate the mind.

One potential governance concern is executive compensation growth. In recent years, Mr. Green’s total compensation has been quite generous (in the millions), commensurate with peers but perhaps not commensurate with a year of declining earnings. Shareholders should watch that pay is truly “pay for performance.” The proxy’s compensation discussion indicates the Compensation Committee exercised discretion to moderate payouts when results fell short, which is a good sign. There are no alarming red flags like related-party transactions or over-tenured directors.

West’s management has generally executed well over the past decade, steering the company through complex expansions and a wild pandemic ride. The fact that West scaled production for billions of vaccine components in 2020-21 without major hiccups, then managed a graceful (if not painless) comedown as demand normalized, speaks to operational skill. Communication to investors is typically straightforward, if a bit dry.

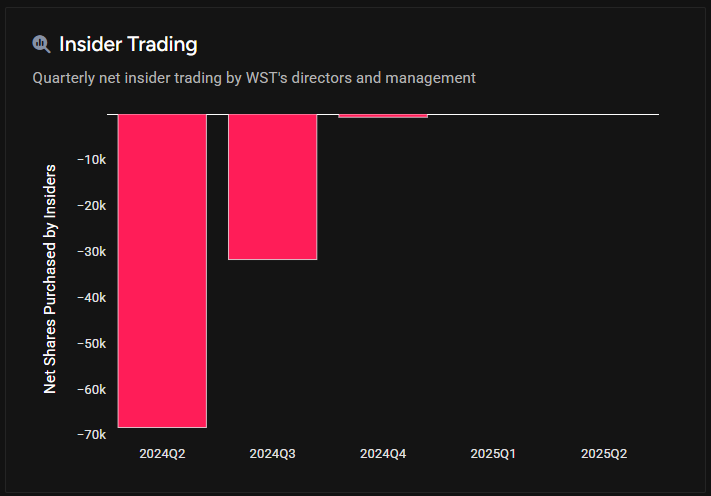

From a shareholder rights perspective, one notable aspect is West’s ownership structure: it’s entirely public float, no controlling shareholders. The largest holders are passives – The Vanguard Group holds ~12.5% and BlackRock ~10.8% – basically unchanged from last year aside from the slight % uptick due to buybacks (they each held ~12.2% and 10.5% a year ago).

There was no significant activist or insider accumulation in the past year; the ownership base is stable with big index funds and quality-focused investors. That implies any major governance changes would likely need broad consensus.

It’s unlikely we’ll see activist agitation here – ironically, an investor like Bill Gates, who favors dominant, high-moat healthcare and life sciences franchises, has already taken a position in West. Not to shake things up, but because it exemplifies the kind of durable, mission-critical business he tends to quietly accumulate and hold for the long term.

Corporate governance can sometimes be an overlooked aspect for a great business. In West’s case, while there are minor areas that could improve (splitting the Chair/CEO role eventually, continuing to refresh the board with diverse expertise), nothing stands out as impairing shareholder value. The company’s bylaws don’t appear onerous, and shareholder votes on say-on-pay and board elections have seen high approval rates. Management’s alignment via equity and the board’s apparent oversight of strategy and risk give us confidence that shareholders’ and management’s interests are reasonably well aligned. This alignment is further evidenced by capital return decisions: West ramped up share repurchases when the stock dipped (suggesting they saw value) and continues to pay dividends without fail, but doesn’t do silly empire-building acquisitions or extravagances. In short, governance is not a significant risk here – if anything, it’s a slight positive that management has skin in the game and is focused on long-term shareholder value.

7/8 Conclusion - Precisely Packaging the Investment Case

West Pharmaceutical Services is the kind of under-the-radar champion that long-term investors cherish: a company with a near-monopolistic grip on a mission-critical niche, secular growth tailwinds, and disciplined management. Yes, the company hit a speed bump as the world worked through a post-Covid inventory glut – and that hiccup bruised the stock badly. But from our analysis, West’s competitive position and growth trajectory remain fundamentally sound. The recent turbulence in financials (and the share price) looks more like short-term noise than a harbinger of decline. In fact, it has arguably strengthened West’s hand: the company used the lull to invest in capacity and gobble up its own shares at a discount, all while weaker rivals stayed quiet.

At ~$208 per share, we believe WST is an attractive buy for investors with patience. The valuation, roughly 32x forward earnings, is not cheap in an absolute sense – but remember that those earnings are temporarily depressed. On a normalized mid-cycle earnings power (once destocking fully passes and new capacity fills), the multiple is more reasonable, and on a EV/EBITDA basis (mid-20s) it’s in line with other high-quality medtech and life science tool companies. We wouldn’t call West a screaming bargain, but for a dominant franchise with decades of growth runway, it’s a justified premium.

Paying a Bentley price for a Rolls-Royce business can still be a good deal if that business reliably compounds for years.

What are the risks? We always consider what could go wrong. Key risks include:

Customer Concentration & Shifts: A significant portion of West’s revenue comes from a few big pharma customers (over 40% of sales from top 10 clients). If a major client switched suppliers or a blockbuster drug using West’s components lost market share, West would feel the pain. Mitigation: West’s breadth of clients and integration into their processes makes abrupt shifts unlikely.

Competition or Innovation Leapfrogs: A competitor could conceivably develop a better material or process that wins new drug platforms. For instance, someone might commercialize a superior elastomer or a new auto-injector that sidelines West. Similarly, if drug delivery technology moves away from West’s sweet spot (imagine many injectables shifting to oral or transdermal forms), demand for West’s wares could soften. We view this as low probability in the near-to-medium term – injectables are here to stay and West itself is innovating at the cutting edge.

Execution & Capacity Risks: As West ramps new plants, execution is key. Delays or cost overruns could hurt margins. Also, should the economic environment worsen, West might find itself with excess capacity for a time. However, West has a good track record of scaling in line with demand (and the conservative nature of pharma provides some visibility into future needs through long-term agreements).

Regulatory or Quality Event: If West were to have a quality control failure leading to a recall or contamination incident for a client, it could tarnish its reputation (and potentially incur liability). This is a critical area to monitor, but West’s history has been stellar on quality, and its culture appears deeply quality-centric.

Macro Factors: Currency exchange rates can impact reported results (West has large euro and other foreign ops). Additionally, inflation in raw materials or labor can pressure margins if not passed on. The strong dollar was a noted headwind in 2024. West does hedge some exposures and can adjust pricing over time, but macro swings can cause short-term volatility.

Balancing these risks against West’s strengths, we believe the risk/reward remains favorable for long-term investors. West has shown that even in a rough year, it stays profitable and financially solid. In all but the most extreme scenarios, the company should continue to grow alongside the pharma industry – an industry that itself has one of the most reliable growth profiles (global drug demand almost invariably rises year after year).

In concluding our investment thesis: West Pharmaceutical is not a flashy story – it won’t cure diseases or launch the next social network. What it will do, in our view, is quietly dominate its indispensable corner of healthcare, year after year, with a mix of precision and prudence. The company’s 100-year history of steady evolution and value creation is testament to that. If one can get comfortable with a medium-term P/E in the 30s (a reflection of high quality rather than hype), West offers the promise of compounding returns bolstered by a wide moat. We have a critical, data-driven eye on West’s progress, but from what we see, the long-term trajectory is up and to the right – securely sealed like a West stopper on a vial.

8/8 Projections: 5-Year Scenario

For our premium subscribers, we’ve developed a detailed 5-year projection model in Excel, which can be accessed separately. The Deep Dive will be accessible for one month. After that, it, along with the Excel template, will be available exclusively to premium subscribers.

Below, we summarize the key outcomes of our Base, Bull, and Bear scenarios:

Bull Case: Biologics Surge & Full Recovery

Keep reading with a 7-day free trial

Subscribe to Swiss Transparent Portfolio to keep reading this post and get 7 days of free access to the full post archives.