96% Earnings Growth, 77% Margins, 5%+ Yield: The SaaS Stock You’ve Probably Missed

The Hidden Compounder Powering My Outperformance

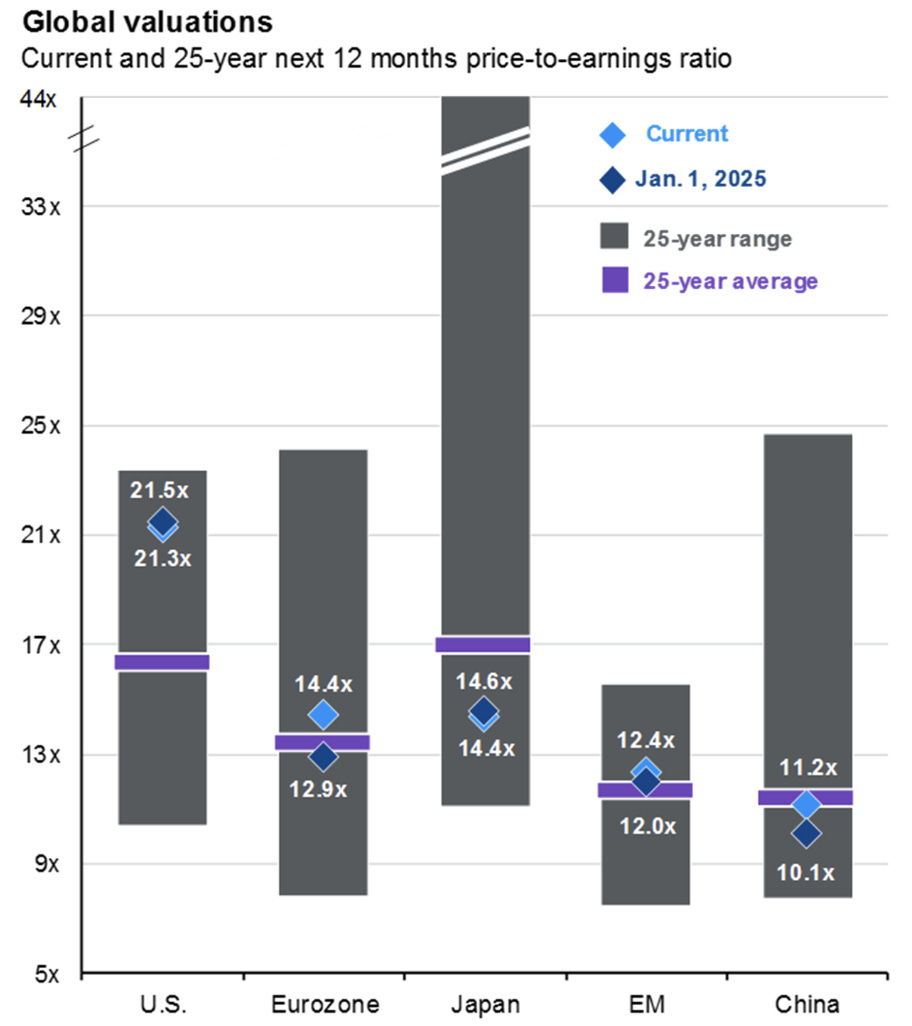

Investing from Switzerland gives me the tax edge. Now the question is: what businesses can best compound from here? To answer that, you need to know where to look: across sectors, regions, company models (global scale or niche?), and above all, balancing growth vs valuation. Why do you think Warren Buffett’s largest international investments lately have been in Japan? Just look at the chart below (from JPMorgan’s latest Guide to the Markets report, May 31, 2025): In a world where U.S. equities are trading at 21.3x earnings, Japan trades at just 14.4x, with companies offering strong balance sheets, global earnings, and a shift toward a more shareholder-friendly environment.

This is exactly the approach I try to follow: find undervalued businesses, with growth, in sectors and regions with structural tailwinds, and run by highly aligned management teams.

Which brings me to one of the biggest contributors to my current outperformance vs the S&P 500:

A position that has helped me maintain a significant lead since inception (37.61% vs 17.95%) is Azeus Systems ($BBW).

Discovered in early 2024 and added around 3Q24, it’s a business with explosive earnings momentum, a massively underpenetrated global market, and a management team compounding shareholder returns the right way. Here’s why I’m long, and why the story is just getting started.

Sentiment: Attractively priced ✅. Azeus Systems ($BBW) keeps delivering: explosive earnings, minimal capex for now, strong FCF, untapped global market, and a founder-led team compounding value the right way. The latest FY2025 results lit a fire under the stock, yet even after the run, valuation still looks attractive relative to growth. Risks: customer concentration, international scaling challenges, rising competition. But this remains one of the best asymmetric setups in my portfolio today.

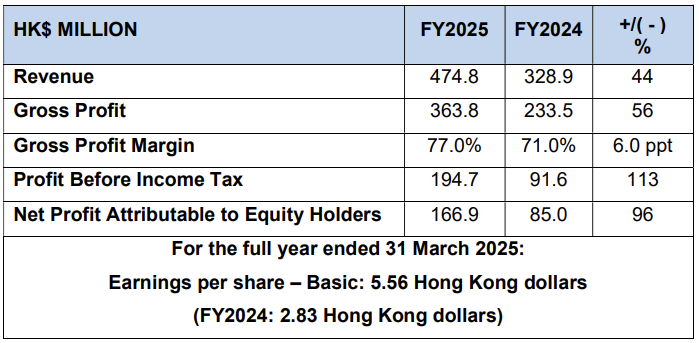

After the company announced record results on May 30, 2025, investors rushed in, pushing Azeus’s share price up 16.6% and 13% on the following two trading sessions. Such a dramatic two-day surge reflects the euphoric response to Azeus’s stellar numbers: revenue up 44%, net profit nearly doubled, and a 100% increase in dividends year-on-year. This post will dive deep into Azeus’s results and fundamentals, blending the excitement of the short-term momentum with a sober analysis of its 3–5 year growth potential. We’ll explore how Azeus’s product-led business is compounding growth, examine its segment performance, profit margins, and cash flows, review the dividend bonanza and capital structure, assess its product pipeline (from the flagship Convene to the new ESG platform), benchmark its valuation against peers, compare the ownership structure now versus the past, and finally consider the forward outlook. By the end, it should be clear why Azeus’s FY2025 is more than a one-off spike, it could be the springboard for a multibagger story.

If you’re enjoying this, a follow and a share go a long way to support my deep dives. I’ll continue sharing deep dives on $BBW and other asymmetric opportunities. I focus on compounding businesses, smart capital allocation, and tax-optimized investing, with a long-term lens. To stay updated, just subscribe below ⬇️.

FY2025 Earnings Breakout and Stock Surge

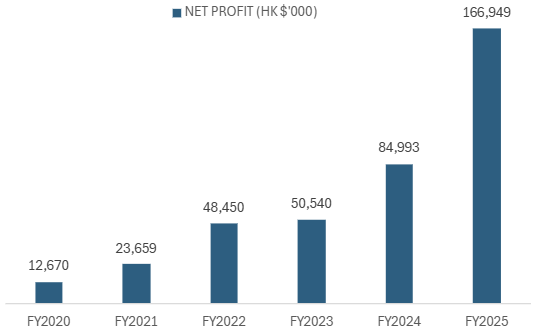

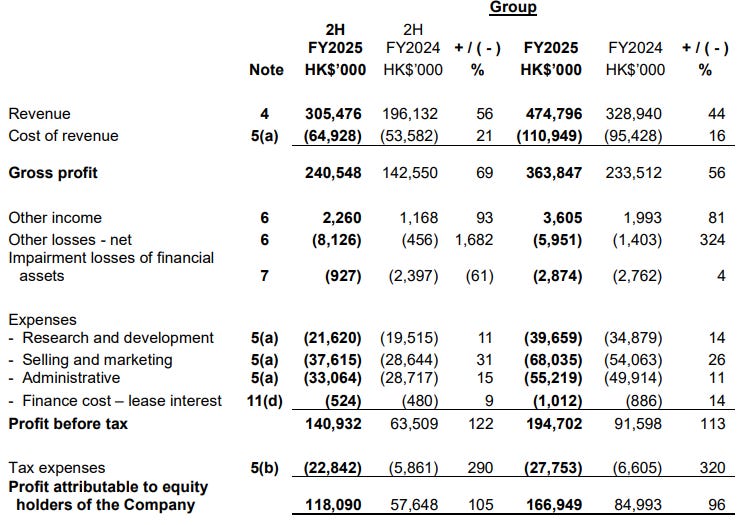

Azeus’s full-year FY2025 (year ended March 31, 2025) results were nothing short of explosive. Revenue jumped 44% to HK$474.8 million while net profit attributable to shareholders soared 96% to HK$166.9 million, both all-time highs.

To put that in perspective, net profit nearly doubled from HK$85.0 million in FY2024, a huge acceleration in growth. The net profit margin leapt to 35% (from 26% the prior year), reflecting much improved profitability. Return on Assets (ROA) surged to ~38% in FY2025, up from ~26% the year before, a clear sign of enhanced capital efficiency.

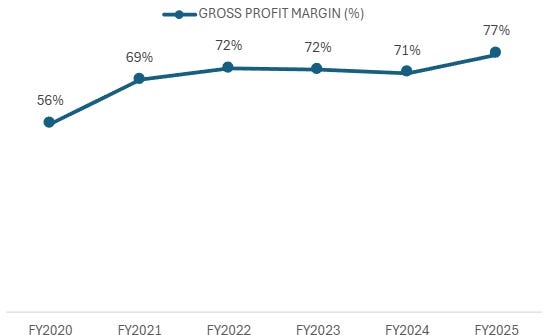

Gross margin expanded from 71% to 77%, while free cash flow more than doubled year-on-year, another clear signal that Azeus is scaling with remarkable operating leverage.

The magnitude of the earnings beat caught the market by surprise, triggering a wave of buying. On June 2 (the first trading day after results), the stock spiked from around S$12.45 to S$14.52 by mid-day, a 16.6% gain, and 30% on the week.

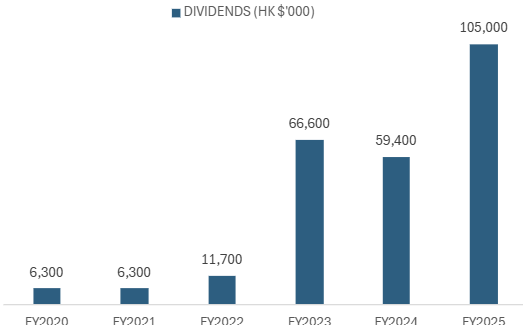

This rally also coincided with news that total dividends for FY2025 doubled to HK$5.50 per share, as Azeus proposed a hefty final dividend of HK$3.90 on top of an interim HK$1.60. Essentially, management is paying out virtually all profits, a 99% payout ratio, to shareholders, rewarding investors with cash and underscoring confidence in the company’s cash generation. It’s rare to see such high growth and high yield together: even after the price jump, the dividend yield stands around ~5% for FY2025, which certainly added fuel to the stock’s momentum.

I would guess that the ~77% insider ownership helps explain this consistent preference for distributing cash rather than pursuing aggressive reinvestment, and this policy likely attracts and retains investors as well, especially in a small-cap name. That said, based on recent management commentary, it seems they are now looking to expand sales and market presence, more on this later.

Narratively, Azeus’s earnings announcement had all the ingredients to excite the market: record revenue and profit, a juicy dividend hike, and optimistic commentary about future growth. Investors responded accordingly, bidding the stock up to new highs. The short-term momentum is clear, but what’s driving these outstanding results? To answer that, we delve into the business segments that propelled Azeus’s breakout year.

Segment Performance: Products Powering Growth

Azeus operates two primary business lines: IT Services and Azeus Products. FY2025 made it abundantly clear that the growth engine is the Products segment. Azeus Products contributed 83% of total revenue in FY2025, dwarfing the 17% from IT Services. Moreover, product revenue grew by 55% year-on-year, vastly outpacing the modest 10% growth in the IT Services line. In absolute terms, product revenue surged to HK$391.8 million (from HK$253.5m the year before).

What drove this impressive growth? The company credits strong demand for its proprietary software products, notably the “Convene” family, and a major ongoing project win:

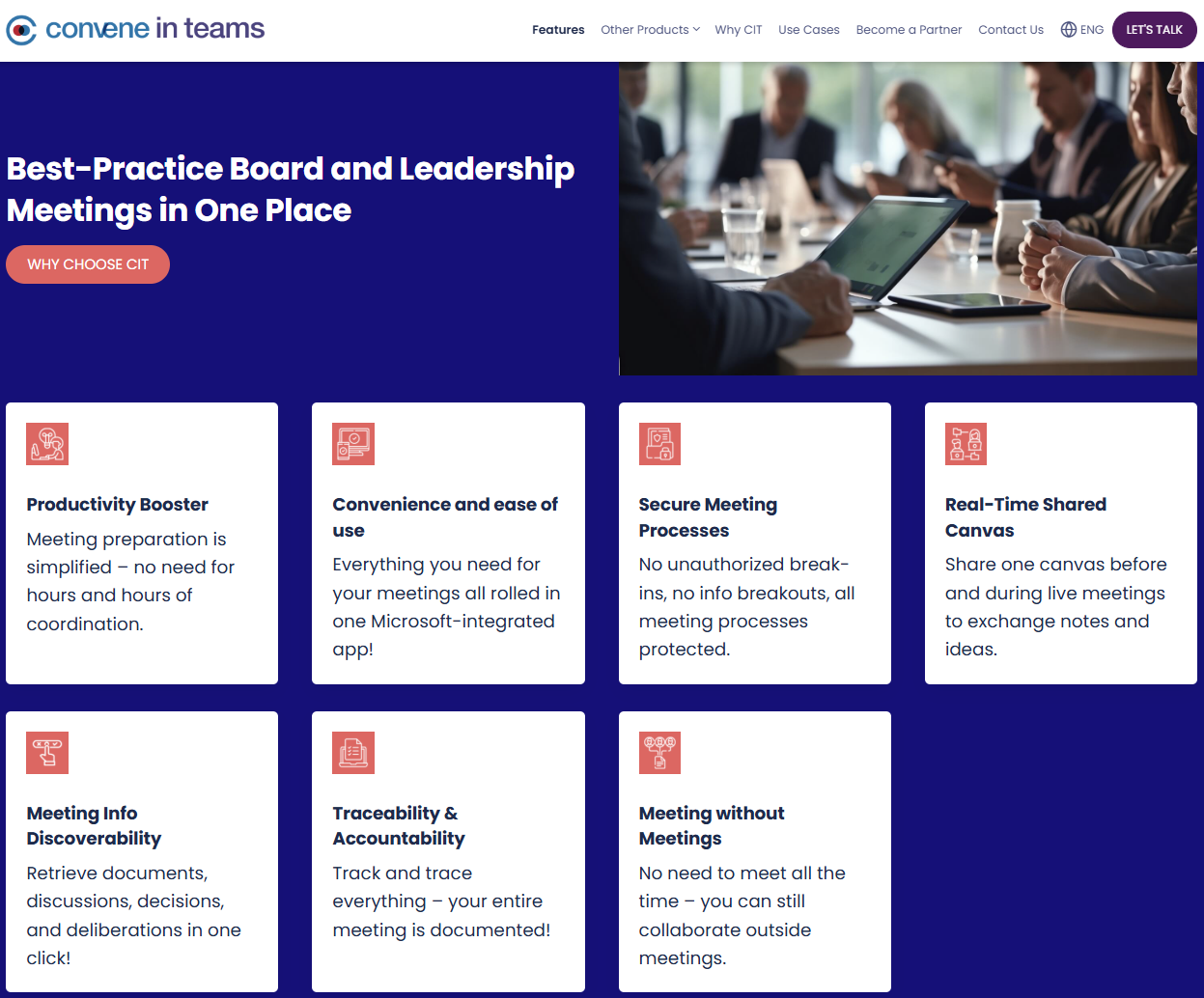

Convene & Convene Records: Azeus’s flagship product “Convene” (a digital paperless meeting solution) and its newer “Convene Records” platform saw robust license sales. The Group reported higher product license revenue across its client base, reflecting broader adoption of these solutions. Convene has been a hit with enterprises and governments seeking secure, efficient board meeting and document management software. One particularly interesting feature is that Convene can be integrated with Microsoft Teams, enhancing its appeal and usability within existing enterprise workflows.

Meanwhile, Convene Records is at the heart of a massive government contract (more on this below):

CERKS Project: The Central Electronic Record Keeping System (CERKS) deployment for the Hong Kong government is a multi-year beautiful mega-contract valued at HK$1.02 billion. This project entered its active deployment phase in FY2024, and in FY2025 it became a significant revenue contributor. Implementation services and licensing fees from CERKS boosted the Products segment income. In fact, revenue from Hong Kong & Asia jumped 61% to HK$301.7 million, primarily due to recognizing CERKS project revenue as various government departments onboarded the system. This “all-of-government” rollout of Convene Records (the software powering CERKS) has been a game-changer for Azeus’s top line.

The smaller IT Services segment, which includes systems implementation projects, enhancements, and maintenance services for clients, grew to HK$83.0 million in FY2025 (up 10% from HK$75.4m). Within IT Services, new project implementation revenue actually rose a robust 28% to HK$30.0m, thanks to more contracts secured during the year. However, this segment remains relatively “flat” (+10%) without the scale of Products. The bulk of IT Services revenue (about 64%) comes from recurring maintenance and support contracts, a stable, but low-growth component that contributed HK$53m. Essentially, Azeus’s legacy services business provides a steady base (and service to long-time customers), but the excitement lies in the Products business which is scaling rapidly.

Geographically, Hong Kong/Asia is Azeus’s largest market (accounting for ~64% of revenue) and the fastest-growing, up 61% year-over-year due to CERKS. Other regions like Middle East, Europe, and the Americas also saw growth, albeit from smaller bases, driven by global sales of Azeus Convene. This indicates that Azeus’s product push is not confined to its home turf; it’s increasingly a global story with clients in over 100 countries. In summary, FY2025’s segment breakdown tells a clear story: Azeus has transformed from an IT services provider into a product-centric software company, and that strategic pivot is yielding high growth.

If you thought, (like I did), that Microsoft could one day easily integrate similar tools into its MS Teams suite, well… maybe. But consider this: take a look at the following example with Diligent. In 2016, Insight Partners acquired Diligent (one of the global leaders in board management software) for a reported $624 million. Clearly, there is strategic value in these niche/specialized, high-trust platforms that even large players like Microsoft haven’t fully replicated. Here’s a short video to get a sense of how Diligent positions itself.

Sky-High Margins and Robust Profitability

One striking aspect of Azeus’s FY2025 results is how profitability leaped even more than revenue. The gross profit margin hit 77%, a significant jump from 71% in FY2024.

This 77% gross margin is exceptionally high (comparable to elite software companies) and underscores the lucrative economics of Azeus’s product business. Software license sales, like those for Convene, have high incremental margins, especially as sales scale up with relatively fixed development costs. Additionally, the CERKS project, while involving services, also delivered high-margin license fees for the deployment of Azeus’s proprietary platform. As a result, gross profit rose 56% to HK$363.8 million, outpacing revenue growth.

Net Profit Trend (FY2020–FY2024): Azeus’s net profit has compounded rapidly in recent years, reflecting improved margins. FY2025 nearly doubled net profit again to HK$166.9m, far exceeding the FY2024 bar.

At the operating level, expenses remained well-controlled despite aggressive growth. Azeus did increase investment in R&D and sales (management noted continued spending on product development and marketing initiatives), but the surge in gross profit far outweighed these costs, which declined year-over-year as a percentage of revenue.

Consequently, profit before tax (PBT) more than doubled, up 113% to HK$194.7 million. The PBT margin expanded to about 41% (from 28% in FY2024), a huge jump indicating strong operating leverage. After taxes, net profit came in at HK$166.9 million, up 96%. For a sense of scale, five years ago Azeus’s annual net profit was under HK$25 million; now it earns that in a good month. The compounding of earnings has been extraordinary, as illustrated by the chart below, and FY2025 took it to another level.

Crucially, these profits are backed by real cash generation. Azeus operates an extremely asset-light business model, with minimal capital expenditure, just HK$3.526 million in FY2025, or less than 1% of revenue, as most investment is funneled through R&D and expensed through the P&L. In effect, free cash flow is nearly equivalent to Net cash provided by operating activities.

While as investors we might wish to see an even more dynamic deployment of this surplus cash, Azeus has consistently favored a disciplined, conservative approach: maintaining a pristine balance sheet and rewarding shareholders through steadily increasing dividends. In FY2025, the company generated HK$197.9 million in operating cash flow, distributed HK$105 million in dividends, and still expanded its net cash position to HK$270.3 million, a 48% year-over-year increase, all while remaining entirely debt-free. The expansion in margins and cash generation in FY2025 also highlights the operating leverage embedded in Azeus’s model: as product revenues scale, a greater portion of each incremental dollar flows directly to the bottom line. This dynamic could persist in coming years if revenue growth continues, positioning Azeus as a compelling long-term earnings compounding story.

Shareholder Rewards: Dividend Windfall and Return History

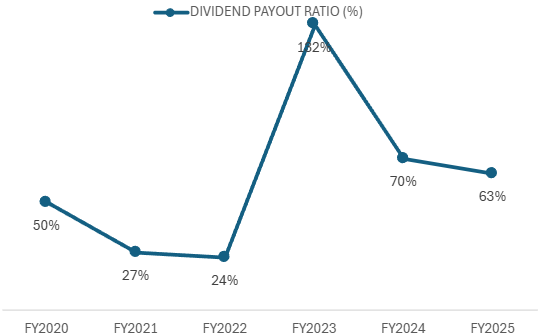

Azeus has coupled its growth with exceptionally shareholder-friendly capital returns. As mentioned, the Board has recommended for FY2025 a total dividend of HK$5.50 per share (HK$1.60 interim + HK$3.90 proposed final), representing a 99% payout ratio on reported net income of HK$166.95 million. It’s worth noting that while only part of this was paid within the fiscal year (HK$105 million), the company’s practice is to communicate payout ratio on a declared basis, including both interim and proposed final dividends against current year earnings.

This is double the HK$2.75 total payout in the prior year (FY2024), effectively mirroring the doubling of earnings. In fact, Azeus has a policy (implicit, if not explicitly stated) of paying out the bulk of its earnings as dividends.

The 99% payout for FY2025 (considering (HK$1.60 interim + HK$3.90 proposed final) is not an anomaly, historically the company has distributed a high percentage of profits, especially as profits surged in recent years.

This trajectory means that anyone who bought Azeus shares a few years ago has seen their dividend yield on cost multiply. Even at the current stock price (~S$16.50, which is about HK$100), the trailing yield is approximately 5.5%, which is outstanding for a tech-oriented growth company. That’s a sizable cash return in absolute terms and indicates management’s confidence that the business can both invest in growth and reward shareholders concurrently.

In terms of total shareholder return, Azeus has been a quiet multi-bagger on the SGX in recent years. The share price appreciation has mirrored the earnings climb. Over the last 12 months alone, Azeus’s stock is up roughly 80% (including the recent post-earnings spike). If we look back 3–5 years, the gains are even more impressive: five years ago the stock traded under S$3; it’s now over S$14. Combined with the regular dividends, long-term holders have reaped substantial returns. One striking datapoint: return on equity (ROE) has climbed from 13% in FY2020 to an impressive 75% in FY2025, a clear sign of how efficiently Azeus is compounding shareholder value.

This performance flies under the radar given Azeus’s small-cap nature, but it underlines a key point, Azeus is transitioning from a niche IT firm to a high-growth, high-return investment shareholder-friendly. So far, the strategy has worked: Azeus funds all necessary R&D and expansion from operating cash flow, and still pays out almost all profits. For investors, it’s the best of both worlds, growth and yield.

Balance Sheet Strength: Net Cash and No Debt

Azeus’s financial position is rock-solid. The company’s balance sheet as of end-FY2025 carries HK$270.3 million in net cash (and equivalent liquid assets). There are no loans, no bonds, and no debt of any kind on the books. This effectively means Azeus’s growth has been financed entirely through internal resources. It also provides a significant safety net; the cash on hand could cover unforeseen downturns or be deployed for strategic investments, all without any financial strain.

To put the cash into perspective, HK$270.3m is about S$47 million. On a per-share basis, it equates to roughly HK$9.0 of cash per share (around S$1.55 per share). In other words, about 10% of Azeus’s current market capitalization is backed by net cash. This cushion adds to the intrinsic value and also enables continued high dividends, Azeus can comfortably pay out dividends even during quarters where cash receipts might lag accounting profits slightly, because it has a war chest on standby.

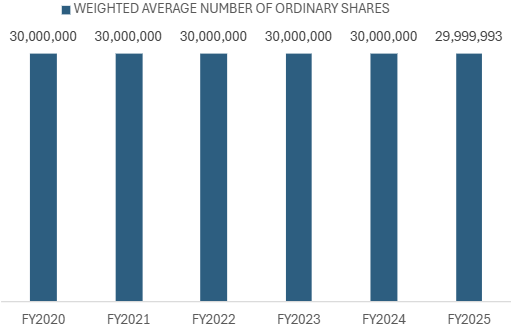

The capital structure is simple and clean: only common equity and accumulated earnings. Share capital has remained stable with no dilution in recent years, Azeus has not issued new shares or raised equity capital since its IPO over a decade ago. In fact, the share count is so stable that earnings per share (EPS) growth aligns directly with net profit growth. FY2025 EPS was HK$5.56, up 96% from HK$2.83 the previous year, exactly mirroring the net profit jump. Investors can likely expect this no-dilution policy to continue, as the company generates ample cash and doesn’t need external financing.

In sum, Azeus’s capital structure is very shareholder-friendly: debt-free, cash-rich, with a tendency to distribute surplus cash. This conservative balance sheet management means Azeus has flexibility for the future, whether to make an acquisition, invest more aggressively in new products, or simply keep returning cash. It also insulates the company from interest rate or refinancing risks that leveraged companies face. In volatile times, that net cash position provides stability and confidence to investors that Azeus can weather storms and seize opportunities.

Product Pipeline and Key Growth Catalysts

While FY2025’s results are impressive, the critical question for a 3–5 year investment thesis is: what will drive Azeus’s growth going forward? Here, Azeus has a number of catalysts on the horizon, anchored by its product pipeline and strategic projects:

CERKS Project (Ongoing through FY2027): The Hong Kong government’s central records system deployment remains a backbone of near-term growth. As of FY2025, Azeus has recognized only part of the HK$1.02 billion contract’s revenue.

The remaining deployment and licensing revenue will be recognized over FY2026 and FY2027 as the project continues on schedule.

This provides a baseline of secured revenue for the next two years. Importantly, management noted that the rollout is progressing well and has received positive feedback. As more government bureaus come online and users are added, Azeus will book additional fees. Even though the ultimate number of users may vary as deployment continues, the scope of CERKS suggests a multi-year tailwind. By FY2027, Azeus will have not only earned the contract value but also established a flagship reference deployment for its Convene Records platform, a case study it could leverage to win similar e-government projects elsewhere.

Azeus Convene – Global Expansion: Convene (the board meeting and collaboration app) is Azeus’s most well-known product internationally. It has been gaining traction with corporates, nonprofit organizations, and public institutions in dozens of countries. In FY2025, revenue from regions outside Hong Kong grew, thanks in part to Convene’s sales. Over the next 3–5 years, Azeus plans to broaden its geographical reach even further. Key markets include Europe, where Azeus already has a presence (the company has offices in London and Madrid), and North America, which remains a large untapped market for the company. Convene’s value proposition - secure, efficient digital meeting management - is increasingly compelling as organizations digitize governance processes. There is significant runway for Azeus to add new clients and roll out product upgrades (such as enhanced video-conferencing integration, workflow features, etc.) to drive subscription/license growth. Continued strategic marketing investments are being made to promote Convene globally, which should support customer acquisition in new regions.

New ESG Reporting Platform: Azeus is developing a brand-new Environmental, Social, and Governance (ESG) reporting platform to capitalize on the rising demand for sustainability and compliance tools. As ESG reporting becomes mandatory in more jurisdictions and companies seek to streamline how they track and report sustainability metrics, this presents a timely opportunity. While details are limited, Azeus’s CEO specifically highlighted continued investment in the ESG platform’s development. We can expect this product to contribute in the coming year or two. If done well, it could be sold to both existing Convene customers (complementing board governance with ESG oversight) and new clients (such as listed companies needing to produce ESG disclosures). Given Azeus’s track record with enterprise software and government contracts, an ESG solution could find ready markets in the Asia-Pacific and beyond. This platform represents a new growth vertical that could add a fresh revenue stream on top of Azeus’s core offerings.

Convene Records - Beyond Hong Kong: Having an entire government adopt Convene Records via CERKS is a strong validation of the product’s capability in large-scale records management. Post-CERKS, Azeus can market Convene Records to other governments or big enterprises facing digital records challenges. Many public sector bodies (in Asia and elsewhere) are modernizing their record-keeping, Azeus now has a proven case study to reference. Over 3–5 years, if Azeus can win even a couple more sizable contracts for records management (perhaps in other countries’ government agencies or multinational firms), it would sustain the product segment growth after CERKS tapers off.

Recurring Revenue Base: As Azeus’s installed base of product customers grows, so does its annuity-like income from maintenance, support, and subscription renewals. Already in FY2025, recurring maintenance revenue was HK$53m (mostly from IT Services clients). For the product segment, many clients likely pay annual fees or SaaS subscriptions for Convene. Although Azeus doesn’t break out recurring product revenue explicitly, we can infer that a portion of the HK$391.8m product revenue is recurring (for example, cloud-hosted Convene subscriptions or yearly license renewals for clients). Over time, as the user base expands, this sticky revenue should grow, providing more predictable cash flow. This also gives Azeus the ability to upsell new modules (like ESG or additional Convene features) to an existing client base.

In summary, Azeus’s growth catalysts for the next few years revolve around maximizing current wins (CERKS), scaling core products (Convene and Records) in new markets, and launching new offerings (ESG platform). The combination of ongoing contract revenue and new product initiatives creates a path for Azeus to continue compounding its business. It’s feasible that Azeus could sustain a double-digit annual growth rate in revenue and profit over the next 3–5 years if these catalysts play out. Of course, execution will be key, the software space is competitive, and Azeus will need to maintain its innovation edge and customer service reputation to keep growing. But given its recent track record, the company appears well positioned to seize these opportunities.

Ownership Structure: Then and Now

Azeus’s shareholding structure is unique and worth understanding, as it has implications for stock liquidity and management alignment. The company was founded by Mr. Lee Wan Lik, who serves as Executive Chairman, and he (along with his family) has retained a very large ownership stake. In fact, historically the Lee family controlled an outright majority of the company.

According to Azeus’s Annual Report 2021, the founder and his spouse (Ms. Lam Pui Wan) together had deemed interests in 51% of Azeus’s shares through a holding vehicle (Mu Xia Ltd.), in addition to about 31% held directly (26.8% by Mr. Lee, 4.7% by Ms. Lam). This meant that as of 2021, they effectively controlled ~77% of the company’s equity. The public float at that time was only ~17.6%, which is quite low and just above the SGX’s free float requirement.

Fast forward to today, and the ownership is still very much insider-dominated, though there have been some changes. Ms. Lam Pui Wan sadly passed away (her shares are presumably now held by her estate or transferred), but Mr. Lee remains at the helm. He is reported to directly hold ~27% of the company now.

The Mu Xia Ltd. vehicle (90% owned by Ms. Lam’s estate, 10% by Mr. Lee) likely still holds the 51% block, meaning the founder’s family estate effectively still controls a majority of shares. Insiders and related parties in aggregate own well over 80% of Azeus, by all indications. Even the next largest shareholders are small by comparison:

The implications of this structure are twofold:

Strong Alignment and Stability: The founder’s huge ownership stake means management’s interests are closely aligned with shareholders. Mr. Lee’s wealth is largely tied to Azeus’s long-term success, so he has every incentive to continue growing the business prudently and maintaining dividend payouts. The company has been run in a financially conservative manner, which likely reflects this owner-operator mindset. This also provides strategic stability - there’s little risk of a hostile takeover or radical strategy shift with the founding family in firm control.

Limited Liquidity: The downside is that the free float is small, which can lead to low trading liquidity and higher stock volatility. With perhaps only ~20% of shares truly available in the market, large investors might find it hard to accumulate or exit positions without moving the price significantly. This could partly explain why Azeus’s valuation stayed modest for so long, it wasn’t on the radar of bigger institutional investors due to liquidity constraints. However, liquidity has been gradually improving as the company’s market cap grows (it’s now around S$490+ million). The big volume spike on the post-results day suggests that interest is picking up, and sometimes sustained strong performance can draw in more trading activity regardless of float.

It’s also worth noting that no equity fund-raising or significant sell-down by insiders has occurred in recent memory. The Lee family appears content holding their stake, reaping dividends, and letting the share price appreciate. If anything, one could watch if the founding shareholder eventually trims a bit to improve float, but given their long-term approach, such a move would likely be measured (if at all). For now, the structure means shareholders can invest alongside a founder-owner who has skin in the game, which is generally a positive in fundamental investing.

In comparing the past vs. present structure, essentially the control remains with insiders as before, so not much has changed except the value of those holdings has risen dramatically with the stock’s climb. The public float percentage may have inched up marginally (due to any estate distribution or minor selling), but Azeus is still a tightly held company. This backdrop is important to keep in mind when evaluating the stock, it may not behave like a widely-owned blue chip, but the flip side is that insider commitment is very high.

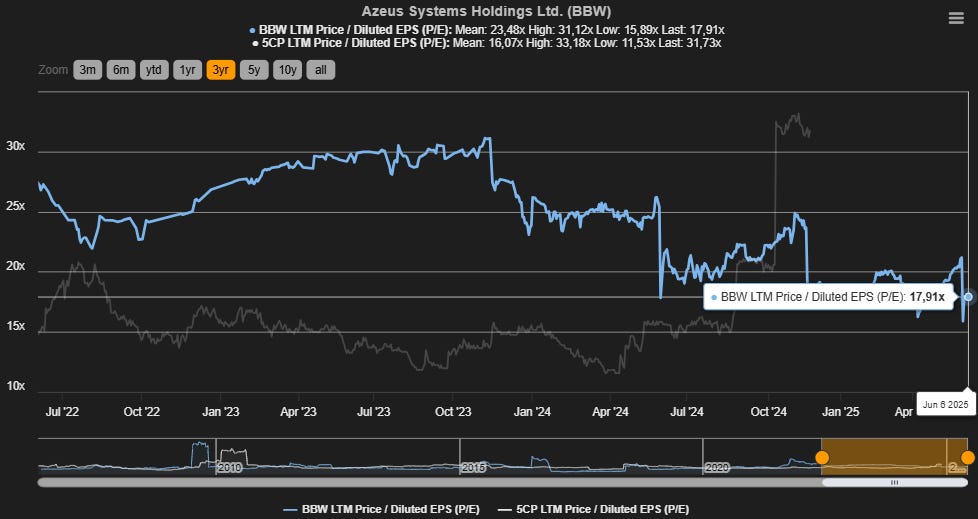

Valuation Upside: Still Compelling vs. Peers

After the recent rally, Azeus’s valuation has re-rated higher, yet it still appears moderately priced relative to its growth and peers in the tech sector. Let’s break down a few valuation metrics:

Price-to-Earnings (P/E): Based on FY2025 actual earnings (EPS of HK$5.56, equivalent to ~S$0.96), the stock’s trailing P/E at S$16.50 is about 17 times. A 17x trailing multiple for a company that just grew earnings ~96% is arguably low. Even if one assumes growth will normalize to a more modest pace, Azeus’s forward P/E is likely lower. For instance, if net profit grows say 20% in FY2026 (a conservative assumption given CERKS revenue will increase), forward P/E would drop to ~13-14x. Compare this to industry peers: Silverlake Axis, another Singapore software company (focused on banking software), who was acquired last year at around 31x earnings. Global software companies with high growth typically command P/Es well above 20x. Azeus, with its mix of high growth, high margins, and high dividend, looks undervalued on a pure earnings multiple basis.

But let’s go one level deeper, beyond the multiples. Based on FY2025 results, Azeus’s non-CERKS product revenue, primarily from Convene and Convene Records, is estimated around HK$230m–270m. With market benchmarks suggesting an average pricing of ~HK$100k–150k per client per year (USD ~$10k–20k), this implies Azeus today serves roughly 1,500 to 2,500 paying clients globally. Now compare that to the broader market: the global “Board Portal” segment is a ~$2.5B–$3.5B market today, expected to surpass $4B by 2028, with an estimated 100k–200k paying enterprise clients already on solutions like this, and a long-tail potential of 700k–900k global organizations who could adopt. In other words, Azeus is barely at ~1–2% penetration of the current paying market, and far below total TAM.

For context: Diligent, the market leader, reportedly serves ~25k clients and is believed to generate >$600m+ annual revenue, proving that this space can scale fast and profitably once penetration deepens. Azeus, with its proven product, expanding global footprint, and much leaner cost base, still has a long runway to catch up. If they simply double or triple their client base over the next 3–5 years, which is entirely feasible given their TAM and momentum, product revenue and EPS could scale materially. And this growth would come with 77% gross margins, zero debt, and strong recurring cash flow.

Dividend Yield: As discussed, the trailing yield is about 5.5%, which is exceptionally high for a company with this growth profile. Most tech peers have yields near zero (as they reinvest or don’t pay dividends). Even mature software firms seldom yield above 3–4%. Azeus’s high yield is a function of its generous payout policy and is unlikely to go unnoticed by investors seeking income. If the stock price stays around current levels, and if Azeus continues to pay out ~90-100% of earnings, investors could be looking at a 5-6% yield forward. This yield provides a solid margin of safety, you’re being paid handsomely to wait for the growth to materialize.

Taken together, Azeus exhibits a “GARP” (Growth At a Reasonable Price) profile: strong growth and quality metrics for valuation multiples that are more akin to a slow-growth company. The undervaluation could be due to its small-cap status and historically low liquidity, which might have kept it off the radar of large investors. But as performance continues to shine, one can expect more attention and possibly some valuation catch-up to peers. Even a re-rating to 20x earnings (which would still be below software sector norms) would imply a significant upside from the current 17x, on top of whatever earnings growth Azeus delivers.

In scenario terms, if Azeus compounds its earnings ~20% annually for the next three years and even gets a modest multiple expansion, the stock could potentially double from here. Of course, valuation is just one lens, and we must consider risks (execution, competition, etc.). But the current pricing suggests potential upside remains if Azeus stays on its growth trajectory.

Outlook: Sustaining the Growth Trajectory

Looking ahead, Azeus faces bright prospects tempered by the usual execution challenges. The momentum from FY2025 provides a strong foundation: the company enters FY2026 with record-high order books, a marquee project mid-stream, and new products in the pipeline. Management’s commentary struck an optimistic tone, emphasizing plans to expand into new markets and innovate continuously. The ongoing CERKS deployment means a substantial portion of revenue for the next two years is already in hand, reducing downside risk. Meanwhile, the push into ESG software and possibly other adjacent solutions (like e-Government services, workflow software, etc.) could open new growth avenues.

In the short-term (next 12 months), investors can watch for a few key developments:

Continued Earnings Momentum: Will Azeus follow up its FY2025 leap with another strong year? Even a moderation to, say, 15-20% growth in FY2026 would be impressive on the higher base. The first half of FY2026 results (due later this year) will be a telling indicator, last year’s 1H saw 79% profit growth, so the comparables are tough, but any growth will demonstrate resilience.

Contribution of the ESG Platform: If Azeus rolls out its ESG reporting product in FY2026, how is the market reception? Early client wins or pilot projects could signal the platform’s potential.

New Contract Wins: Beyond CERKS, any notable contract in government or large enterprise (for either Convene or Convene Records) would be a catalyst. Azeus’s track record with public sector IT projects could lead to surprises on this front (for example, perhaps another government in Asia modernizing its systems).

Margin Trends: With margins at 77% gross and ~35% net, maintaining these levels will be crucial. We will look to see if Azeus can sustain high margins even as it invests in marketing and R&D. The gross margin might fluctuate depending on revenue mix (services vs. license), but staying in the 70s% would confirm the business’s fundamentally high profitability.

Dividend Policy: Given the big jump in FY2025’s dividend, will Azeus keep the absolute dividend flat if earnings don’t jump as much next year, or will it maintain the near-100% payout (which could mean a slight drop in dividend if earnings were flat)? The company’s pattern so far is to size dividends to profits. Any signal of a more measured payout (for instance, keeping some cash for acquisitions) would be noteworthy, though presently there’s no indication of that.

In the medium-term (3–5 years), Azeus’s trajectory could be very rewarding if it continues executing:

We may see Azeus evolve into a globally recognized niche software player, especially in the board management and public sector digitalization space. Convene could become a standard tool for boards in many countries (like how some competitors in the West, e.g., Diligent Corporation, have achieved). If so, Azeus would derive more revenue internationally, diversifying beyond Hong Kong.

The revenue mix is likely to tilt even more toward products, possibly 90%+ by FY2027, given the faster growth of that segment. Services will remain, but mainly as a support function for big projects.

Profit growth might outpace revenue growth in most years, thanks to the high incremental margins. It wouldn’t be surprising if Azeus’s net profit margin stabilizes in the mid-30s% or even approaches 40% if product licensing dominates the mix.

Cash accumulation vs. utilization will be an interesting story. If Azeus continues to pay out ~100% of earnings, the cash level will hover around current levels plus any small buffer. However, should the company decide to retain more cash for a strategic move (e.g., an acquisition of a complementary software company or technology), that would signal a new phase. M&A could be a possibility, Azeus might seek to acquire small tech firms to broaden its product offerings (perhaps in cybersecurity or AI capabilities to enhance Convene). With its clean balance sheet, it certainly has capacity if an opportunity arises.

One cannot ignore possible risks: the software industry is competitive, and while Azeus currently has a strong niche, larger competitors could target its domain. The Convene product competes with other board portal software, continuous innovation is needed to stay ahead. The CERKS project, although on track, is complex; any major hiccup or cost overrun could impact financials (though so far execution has been smooth). Also, foreign exchange fluctuations (HKD is pegged to USD, SGD stable, but multi-currency operations might have some impact) and macroeconomic slowdowns in key markets could influence the pace of new sales.

Nonetheless, Azeus’s fundamental strengths, high recurring revenue, strong client relationships (especially with governments, which tend to stick with proven vendors), and an owner-led management, give it resilience. The company has been around for over 30 years and navigated various tech cycles, suggesting prudent management of both growth and risk.

Conclusion: Azeus Systems’s FY2025 was a defining year that showcased the scalability of its product business model. The immediate aftermath, a euphoric stock surge and dividend windfall, is gratifying for shareholders, but the real story lies in what comes next. With a robust pipeline of projects and products, a war chest of cash, and an entrenched leadership, Azeus is positioned to keep compounding its success. In an era where investors often have to choose between growth and dividends, Azeus offers both. If the company can execute on its vision, expanding Convene’s global footprint, turning its ESG platform into the next hit, and leveraging its CERKS success into more big wins, the coming 3–5 years could see Azeus morph into a much larger enterprise software player, all while continuing to reward its shareholders handsomely. For investors looking for a blend of momentum and long-term growth, Azeus Systems presents a rare and compelling thesis.

If you enjoyed this, a follow and a share go a long way to support my deep dives. I’ll continue sharing deep dives on $BBW and other asymmetric opportunities. I focus on compounding businesses, smart capital allocation, and tax-optimized investing, with a long-term lens. To stay updated, just subscribe below ⬇️.

Final Recommendation & Excel Model for Paid Subs

Keep reading with a 7-day free trial

Subscribe to Swiss Transparent Portfolio to keep reading this post and get 7 days of free access to the full post archives.