The Bear Case II: $GOOGL

The Robotaxi Wars

Alphabet’s “Other Bets” hit $1.65B in 2024. Is Waymo quietly earning its share of that pie? The moonshot no one believed in, is now ahead.

Waymo just hit 10 million paid robotaxi rides, is running 250,000 rides per week across four cities, and plans to more than double its fleet to 3,500 vehicles by 2026. All of this while expanding service in San Francisco, Los Angeles, Austin, and Phoenix, and letting the public in with no waitlist.

Meanwhile, Amazon’s Zoox is still testing. Tesla's big June 23 launch? A cautious dozen cars in Austin, each with a safety driver, and viral clips of them crossing double-yellow lines.

So why is this all still hidden under Alphabet’s “Other Bets” bucket, with investors barely blinking at $GOOGL's robotaxi potential?

Alphabet’s Waymo is quietly achieving what many thought impossible: operating a driverless taxi service at scale. Ironically, the “bear case” for Google might just be that its self-driving success is underappreciated, yet.

🚘Waymo’s Gain Ground in California📍

Waymo’s expanded service area in Los Angeles now spans diverse neighborhoods, reflecting the company’s steady push into major urban markets.

Waymo, Alphabet’s autonomous driving arm, has been steadily expanding its robotaxi service areas in key cities. As of June 2025, the company added about 80 square miles of coverage in San Francisco and Los Angeles (light blue), bringing its total service area in California to roughly 250 square miles.

This expansion includes new parts of the SF Peninsula (down through suburbs like Millbrae and Burlingame) and a broad swath of Los Angeles from beachside Playa del Rey to hip neighborhoods like Echo Park and Silver Lake.

Crucially, Waymo’s ride-hailing service is no longer an exclusive club, waitlists have been dropped, meaning anyone can download the Waymo One app and catch a driverless ride in SF or LA (just as they’ve been doing in Phoenix for years).

These aren’t just small pilot programs either. Waymo recently hit 10 million paid rides completed, and it’s now averaging about 250,000 rides per week across its four cities (San Francisco, Los Angeles, Austin, and Phoenix). For context, that weekly volume rivals some traditional taxi fleets, and it’s growing. To meet demand, Waymo is doubling its fleet size, currently ~1,500 Jaguar I-Pace electric SUVs, by adding 2,000 more vehicles by 2026. If all goes to plan, Waymo will have 3,500 autonomous taxis humming around U.S. streets in the next year or two. The company’s cautious approach (gradual expansion, lots of testing) appears to be paying off in reliability and user adoption.

There are still limitations to note. Waymo is intentionally avoiding the hardest challenges for now: it’s not yet servicing freeway routes or major airports in SF or LA (despite doing autonomous airport runs in Phoenix). These are strategic gaps, highways and airport pick-ups are key use cases if Waymo wants to fully outshine incumbents like Uber and Lyft in all scenarios. The good news is that Waymo is actively testing those capabilities (employees have been riding Waymo vehicles on CA highways in trials) and negotiating airport access. It’s a reminder that even as Waymo leads in robotaxis, it’s still playing a long game on the hardest technical hurdles.

Interestingly, Waymo’s go-to-market strategies are evolving too. In California, Waymo operates via its own Waymo One app, essentially competing directly with Uber/Lyft on their home turf. But in newer markets like Austin (and soon Atlanta), Waymo has struck a partnership to appear inside the Uber app, letting Uber riders hail a Waymo car seamlessly.

This multi-channel strategy shows Waymo isn’t just being pragmatic, it’s being deliberate. By testing both direct-to-consumer (via the Waymo One app) and platform partnerships (like Uber), Waymo is gathering data, optimizing deployment, and refining user experience at scale. The irony? Uber, once a would-be rival, is now tapping into Waymo’s tech to stay relevant in a game Google never stopped playing.

🚕 The Robotaxi Wars

Waymo has been ahead for some time, until now. It’s not alone in the self-driving race. Tech giants and automakers are all vying to define the future of ride-hailing. Here’s how Waymo’s competitive position stacks up against Amazon’s Zoox, Tesla, and Uber.

Amazon Zoox:

Amazon’s robotaxi effort Zoox is arguably Waymo’s closest rival in ambition. Zoox has developed a fully custom robotaxi vehicle, a squat, bidirectional electric shuttle with no steering wheel (often likened to a “toaster on wheels”).

After years of quiet R&D, Zoox is now shifting into gear: in June 2025 it opened a 220,000 sq. ft. factory in California dedicated to robotaxi production. That facility can eventually crank out 10,000 autonomous vehicles per year at full tilt.

Zoox is currently testing in San Francisco (with a few dozen vehicles mapping the streets) and running an early rider program in Las Vegas, with plans to launch its first commercial rides in Las Vegas by the end of 2025. Shortly after, Zoox aims to expand service to San Francisco and other cities. The Zoox vs. Waymo matchup will be fascinating: Waymo has years of real-world experience and thousands of trips under its belt, whereas Zoox has Amazon’s deep pockets and a purpose-built vehicle that could offer a different rider experience. For now, Waymo holds the lead in deployments, but Amazon clearly sees an opportunity to challenge Waymo’s head start.

Tesla:

Elon Musk’s Tesla is tackling the robotaxi race from a fundamentally different angle. Rather than designing a purpose-built autonomous vehicle or relying on lidar, Tesla is doubling down on a pure vision-based approach, betting that its millions of existing EVs (Model Ys, Model 3s, etc.) can be upgraded via software into a self-driving fleet.

The long-promised robotaxi service is finally launching in June 2025, with a pilot in Austin, Texas. But the debut is telling: only a dozen or so vehicles will roll out initially, each with a human “safety monitor” in the passenger seat, far from Musk’s original vision of “no one in the car.” This cautious rollout underscores just how complex full autonomy remains.

And the challenges are real. A now-viral clip circulating online shows a Tesla robotaxi veering across two solid yellow lines, acting unpredictably on a quiet street, highlighting the safety concerns regulators and skeptics have long raised:

Despite the rocky start, it would be a mistake to count Tesla out. Their edge lies in scale: no other company has millions of vehicles already on the road with the potential to receive autonomous capabilities via software updates. Tesla also has a dedicated robotaxi vehicle, the upcoming two-seat “Cybercab”, in the pipeline, designed from the ground up for autonomy.

Still, as of mid-2025, Tesla is clearly playing catch-up. It lacks the depth of ride-hail operational data that Waymo has quietly amassed, and its Full Self-Driving (FSD) system continues to raise regulatory concerns. While Waymo has faced oversight as well, the spotlight remains far more intense on Tesla. The next 12–18 months will be critical, Tesla will almost certainly improve rapidly, but whether it can close the execution gap with Waymo’s fully driverless operations remains an open question.

Uber:

Unlike Amazon and Tesla, Uber isn’t developing its own self-driving cars anymore (after some well-documented setbacks). Instead, Uber is focusing on its strength, a massive ride-hailing network, and partnering with companies like Waymo to supply the driverless vehicles. In practical terms, that means Uber will happily dispatch a Waymo robotaxi to pick you up if one is available, as is starting to happen in Phoenix, and soon in Austin and Atlanta. Uber’s calculus is that it can remain the go-to marketplace for rides, whether human-driven or autonomous, without having to build the tech itself. The competitive dynamic between Waymo and Uber is thus a bit complex: in one sense they compete for the same riders in cities like San Francisco (Waymo’s own app vs. Uber’s app), but in another sense Uber is also a customer/partner, integrating Waymo vehicles to enrich its service. For Alphabet, this partnership is a validation, even the world’s largest ride-hail company finds Waymo’s technology too promising to ignore. In the long run, if robotaxis truly take off, Uber will have to negotiate access to Waymo’s fleets (or those of Zoox, Tesla, etc.), potentially giving the tech owners significant leverage. For now, Waymo’s operational lead (250,000 driverless rides a week and counting) is something Uber can’t match on its own. Uber brings the users; Waymo brings the robots. How revenue gets shared in that scenario could determine whether Waymo becomes a gold mine for Alphabet or just an infrastructure supplier.

🚗 The Robotaxi Equation: Price/Safety

This dynamic sets the stage for a fierce and multi-dimensional battle, where price, safety, and platform control will define the winners:

Waymo leads on scale, reliability, and brand trust. It’s delivering over 250,000 paid rides per week across major cities, and safety data shows a 95% drop in collision rates per ride. But its ~$20–25 fares may limit mainstream appeal unless the price gap with Uber narrows. To tackle that, Waymo is actively reducing vehicle costs, its next-gen autonomous platform uses a more efficient sensor suite with fewer cameras and lidar units to lower production costs without sacrificing safety. In parallel, Waymo and Toyota have teamed up to scale a fleet of autonomous Toyota Sienna minivans, combining Toyota’s manufacturing muscle with Waymo’s full-stack self-driving system. It’s a clear sign Waymo isn’t just expanding geographically, it’s strategically optimizing for scale.

Tesla is going aggressively low with a $4.20 flat fare in its Austin launch. That could supercharge adoption, but early incidents and a history of fatalities tied to Autopilot raise concerns. The pricing is bold. The safety record? Still under the microscope.

Zoox remains in the early stages, with no public pricing announced yet. Backed by Amazon and boasting a custom-built, futuristic vehicle, Zoox is potentialy aiming for a premium/different experience position. But early challenges have already surfaced, the NHTSA (National Highway Traffic Safety Administration) investigated Zoox over rear-end collisions linked to abrupt braking. While the probe was closed in April 2025 after software updates were implemented, it’s a reminder that even the most advanced autonomous platforms face real-world hiccups on the road to scale.

Uber, once a pioneer in the field, is now just the middle layer, offering robotaxi rides through Waymo in its app. It takes a cut, but owns neither the vehicles nor the tech, and increasingly risks being disintermediated as players like Waymo and Zoox go direct-to-consumer. What looks like a smart partnership today may eventually box Uber out of its own game.

This isn’t just a race to build the best robotaxi, it’s a race to make it work economically, safely, and at scale. Success won’t hinge on engineering alone, but on getting the unit economics right, earning public trust, and owning the rider relationship.

That said, this won’t necessarily be a winner-takes-all market. Multiple models may coexist, each excelling in different segments. But over time, only those that balance cost-efficiency, safety, and platform control will earn the right to dominate.

💎 A Hidden Gem in Alphabet’s Valuation?

If price, safety, and platform control are the battlegrounds of the robotaxi war, then Waymo is already winning quietly on two of the three. But you wouldn’t know it from looking at Alphabet’s ($GOOGL) stock price.

Despite running one of the world’s only commercial, fully autonomous ride-hailing networks, and clocking over 250,000 paid rides per week, Waymo is still buried inside Alphabet’s “Other Bets” line, a category many investors treat as glorified science experiments. Wall Street continues to value Alphabet almost entirely on the back of Search. That’s likely a mistake.

At its current trajectory, Waymo is on pace to double its fleet, expand into more cities (Atlanta is next), and eventually capture high-frequency routes like airport trips. Even a single-digit market share in the global ride-hailing space, which is easily a $300B+ TAM, could turn Waymo into a multibillion-dollar revenue contributor for Alphabet. And unlike Uber or Lyft, Waymo owns the tech stack: software, data, sensor suite, and fleet deployment strategy.

In other words, Alphabet is quietly building an Uber alternative, one that doesn’t need gig workers or surge pricing to work.

Of course, some skepticism is warranted. Robotaxis have burned capital for years. Regulatory approval varies by state. And yes, Alphabet’s rollout is cautious by design, not blitzscaling à la Musk. Meanwhile, competitors like Amazon (via Zoox) and Tesla continue their push, each with very different philosophies. Zoox with its custom-built shuttles. Tesla with its fleet-first software vision. But so far, Waymo is the only one delivering scale, safety, and public access at once, and today.

If Waymo were a private company showing this kind of traction, millions of rides, improving safety metrics, multi-city expansion, partnerships with Uber and Toyota, and a clear path to lower manufacturing costs, it would likely command a generous standalone valuation. But within Alphabet, it barely moves the needle. That’s what makes it one of the most interesting and underappreciated assets hiding in plain sight.

The ironic “bear case” for Alphabet is that the market isn’t bullish enough. Every week, Waymo inches further ahead, quietly reducing collisions, expanding coverage, refining tech, and yet it’s still treated as an other bet rather than a business.

If you enjoyed this, a follow and a share go a long way in supporting these deep dives. I’ll keep covering high-quality businesses, asymmetric opportunities, special situations, and tax-optimized investing, often through a long-term lens where it makes sense. If that sounds like your playbook too, you know what to do 😉 ⬇️

If that’s how you invest too, don’t stop here, dig into the archive. If you share my approach to selecting compounders in high-quality jurisdictions with favorable megatrends, my past deep dives are must-reads 👇

HIMS +66% since deep dive (13.1).

IESC +27% since deep dive (9.2).

PSIX +107% since deep dive (5.3).

SPGI +6% since deep dive (14.3).

DUOL +6% since deep dive (1.5).

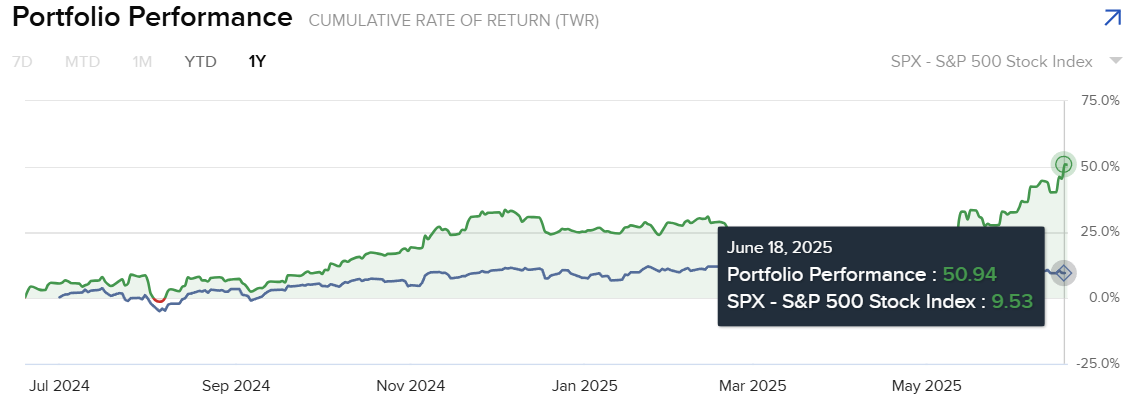

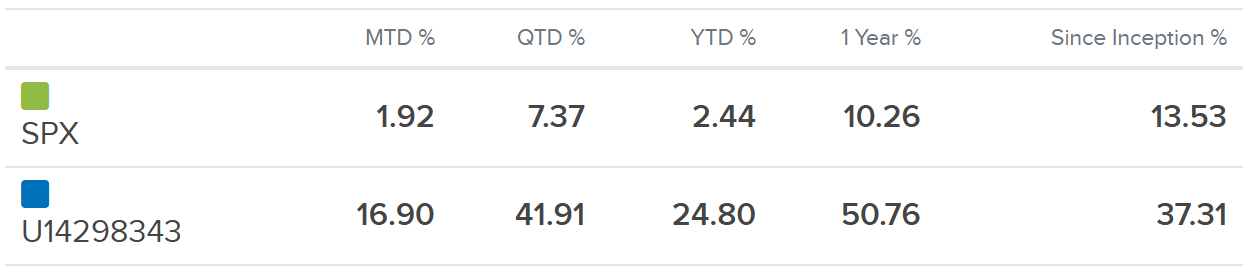

These ideas haven’t just looked good on paper, they’ve delivered. Over the past year, my portfolio is up +50%, handily outperforming the S&P 500’s +9.5%, as shown in the chart below. That’s a +40 percentage point edge driven by focused, thesis-backed positions in companies with strong management, sector tailwinds, and attractive valuations. It’s the compounding effect of being early in high-quality setups:

🚀 Coming soon on the Substack:

👉 In upcoming posts, I’ll cover:

A full deep dive on one of the Top 5 Swiss companies highlighted in this article (free and going live tomorrow).

How to optimize taxes when investing from Switzerland, a huge advantage vs US & EU (free).

Continued deep dives on asymmetric opportunities I’m tracking, including my recent Azeus deep dive (free).

The “move to Switzerland” playbook for investors and entrepreneurs (paid).

My personal Swiss allocation strategy, which has returned 50%+ in a year and 30%+ CAGR over the past 5 years (paid).