Power Solutions International Inc. ($PSIX)

Unlocking the Power of AI

1. Summary

1.1. Investment Idea

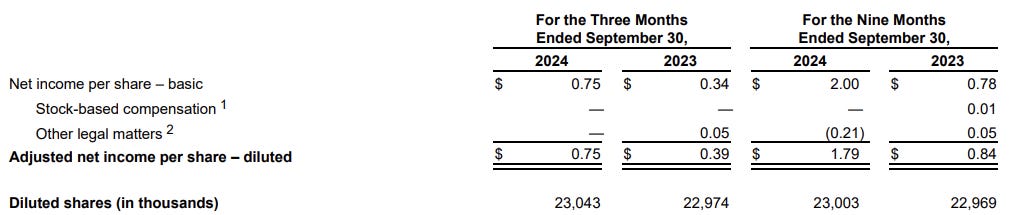

With earnings expected next week, a P/E ratio below 12, NTM P/E under 10, earnings growth exceeding 100% YoY, margin expansion of over 700 bps and legacy businesses declining in favor of a higher-margin power generation market make PSIX an interesting and compelling case. Add to that an opportunistic and masterful strategic shift toward AI and data center demand, with strong tailwinds in the coming years, and the recent Mr. Market sell-off, and a deep dive into PSIX is definitely worth a read.

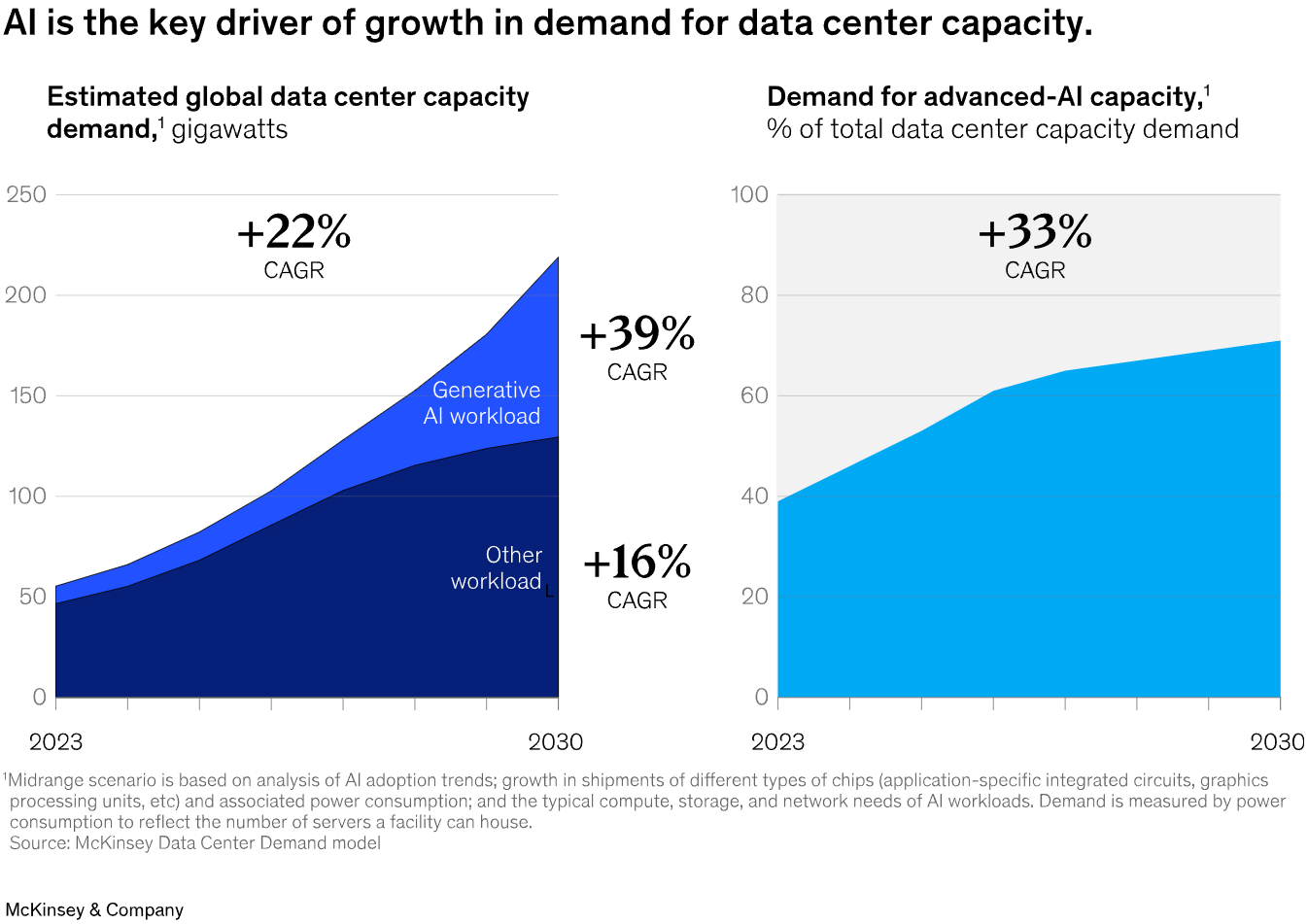

The AI revolution isn’t just about cutting-edge algorithms and breakthrough machine learning models, it’s about the infrastructure powering it all. As Amazon, Microsoft, Google, and Meta prepare to pour over $300 billion into AI infrastructure in 2025 alone, plus the Government’s Stargate project +500 billion in the next 4 years, the demand for data centers, electrical systems, and specialized industrial solutions is reaching unprecedented levels. While the headlines focus on AI giants, the real opportunity may lie in the companies building and supporting this infrastructure. Enter Power Solutions International Inc. ($PSIX), a lesser-known but strategically positioned player in the power systems infrastructure space. As AI data centers scale exponentially, PSIX stands to benefit from the massive capital expenditures driving the next wave of technological transformation, and investors might be overlooking this hidden gem.

Power Solutions International Inc (PSIX) designs, engineers, and manufactures emission-compliant engines and power systems. They specialize in alternative fuel engines and power systems, catering to power generation, industrial, and transportation end markets. Their fuel-agnostic approach, allowing engines to run on natural gas, propane, gasoline, diesel, and biofuels, aligns with global sustainability trends. This makes PSIX an attractive investment for those looking to capitalize on the clean energy transition.

However, PSIX's recent shift toward the rapidly expanding data center market has significantly boosted its earnings. This is evident in the company's Q3 2024 performance, with a nearly 9% year-over-year revenue growth and improved gross margins, resulting in 122% Net Income growth YoY, driven by strong demand for its power systems in this strategic, high-profit sector, as its CEO Dino Xykis expressed on the last quarterly results:

Mr Xykis: “Currently the Company is actively pursuing several initiatives to enhance and expand manufacturing capacity to meet the increasing demand from data center markets. Pivoting the focus to these markets is driving current net sales growth and profitability.”

Outlook for 2024: The Company expects its net sales in 2024 to increase by approximately 3% versus 2023 levels, a result of expectations for strong growth in the power systems end market paired with lower sales in the industrial end market and a forecasted reduction in the transportation end markets. Notwithstanding this outlook, which is being driven in part by expectations for continuous improvement in supply chain dynamics, including timelier availability of parts and a continuation of favorable economic conditions within the United States and across the Company’s various markets, the Company cautions that significant uncertainty remains as a result of supply chain challenges, inflationary costs, commodity volatility, and the impact on the global economy of the war in Ukraine and Israel, among other factors.

1.2. Why It Is Compelling

Attractive valuation compared with its peers, around 30% less NTM PE.

Pivoting focus to high growth markets: Expanding manufacturing capacity to meet increasing customer demand in higher growth, high margin markets, like data center demand.

The transportation and industrial segments are declining in favor of the higher-margin power generation market. While this shift may initially be perceived negatively, it can create a compelling opportunity.

Optimizing capital structure: Financial flexibility and lower interest costs achieved through debt refinancing through a new Uncommitted Revolving Credit Agreement with Standard Chartered Bank and New Shareholder Loan Agreement with Weichai America.

Achieving operational excellence: Streamlining operating expenses and prioritizing certain R&D investments in support of long-term growth objectives.

Integrated manufacturing with strong R&D.

Leading market position in custom gen set enclosures.

Profitable business with recent cash flow generation.

Asset-light manufacturing model with capital efficiency and scalability.

Strategic focus on rapidly expanding data center sector provides significant opportunity for future growth and continued profitability.

Collaborative value creation and customercentric approach with strong field support capabilities.

Recent Uplisting to The Nasdaq Stock Market.

1.3. Risks

Competition: Larger players like Cummins and Generac pose a threat, potentially eroding PSIX's market share.

Dependence on cyclical industries like construction and infrastructure, which can be vulnerable to economic slowdowns.

Potential labor shortages or increased costs in skilled trades, which could impact project timelines and profitability.

Sensitivity to macroeconomic conditions, including tariffs, interest rate fluctuations, government policy shifts, and supply chain disruptions. Fluctuations in fuel prices and regulatory changes could impact operations, particularly given their reliance on alternative fuels.

Weichai’s majority ownership, with more than 50% of the shares, may influence key strategic decisions, including board appointments, executive leadership changes, and operational directions.

2. Business Model

2.1. History of the Company

Power Solutions International, Inc. (PSIX) was founded in February 1985 by Gary S. Winemaster, Kenneth J. Winemaster, and William Winemaster. Over the years, PSIX has expanded its product offerings to include alternative-fueled power systems and large custom-engineered integrated electrical power generation systems. This diversification has enabled the company to serve a broad range of applications, such as standby and prime power generation, industrial equipment, and on-road vehicles.

Headquartered in Wood Dale, Illinois, PSIX continues to innovate in the power solutions industry, maintaining a significant presence in both domestic and international markets. Their longevity, over 40 years, is a testament to their adaptability, much like a seasoned marathon runner pacing themselves for the long haul.

As of January 2025, the founders of Power Solutions International, Inc. (PSIX) hold the following ownership stakes:

Gary Winemaster: Approximately 2,946,962 shares, representing 12.81% of the company's outstanding shares.

Kenneth Winemaster: Approximately 2,211,274 shares, representing 9.61% of the company's outstanding shares.

These figures indicate that the Winemaster brothers collectively own approximately 22.42% of PSIX's outstanding shares.

2.2. Key Concepts Regarding Its Business

PSIX provides turnkey solutions, meaning they handle everything from design to manufacturing, ensuring a seamless experience for customers. Their fuel-agnostic strategy allows engines to run on multiple fuels, aligning with diverse customer needs and regulatory environments.

2.3. Revenue Analysis by Segments

PSIX operates in three end markets:

Power Systems: Includes stationary and mobile power generation, with growth driven by data center demand.

Industrial: Covers forklifts, agricultural equipment, and more, showing mixed performance with declines in some areas.

Transportation: Medium-duty trucks and buses, facing challenges due to regulatory changes and customer evolution.

The three business segments of Power Solutions International, Inc. (PSIX)—Power Systems, Industrial, and Transportation—demonstrate different trends over the analyzed quarters, with Power Systems showing the most notable growth and benefiting from higher profit margins.

2.4. Capital Allocation

PSIX invests in R&D to innovate and meet customer needs, with recent focus on data center applications. Their capital allocation strategy includes seeking financing solutions, as seen in plans to extend debt maturities, which is crucial given their financial position.

2.5. Financial Health

The Company is focused on leading the business through a growth phase, which includes strengthening the balance sheet while strategically prioritizing products that carry strong demand and higher gross margins. Currently the Company is actively pursuing several initiatives to enhance and expand manufacturing capacity to meet the increasing demand from data center markets.

Pivoting the focus to these markets is driving current net sales growth and profitability. In addition to prioritizing gross profit, the Company is committed to efficiently managing expenses, including streamlining operating expenses and prioritizing certain R&D investments in support of long-term growth objectives. The Company is committed to focusing on growth opportunities and investment while also optimizing its cost structure to enhance growth and profitability, ultimately delivering sustained value to our shareholders.

3. Market Share

3.1. Company’s Dominance in Its Sector

While PSIX maintains a presence across all three segments, its market share is relatively modest compared to the vast global markets. The company's strategic emphasis on the Power Systems segment, coupled with global trends favoring renewable energy and infrastructure development, positions it for potential growth in this higher-margin area.

Power Systems Segment:

PSIX's Power Systems segment focuses on power generation solutions. While specific revenue figures for this segment are not detailed in the provided sources, we can infer its significance from the company's overall performance. The global engines market, encompassing various applications including power generation, is projected to grow from approximately $377.83 billion in 2024 to $477.89 billion by 2029, at a Compound Annual Growth Rate (CAGR) of 4.8%.

This estimate does not account for the potential growth driven by AI advancements, particularly the surging demand for data centers.

Industrial Segment:

The Industrial segment caters to applications such as material handling, construction, and agriculture. The global industrial engines market size was valued at approximately $41.26 billion in 2024 and is expected to reach $58.21 billion by 2033, exhibiting a CAGR of 3.9% during the forecast period.

Transportation Segment:

The Transportation segment includes engines for on-road vehicles such as trucks and buses. This segment has faced challenges, with sales declining due to evolving customer products and new regulatory requirements affecting engine offerings. The global engines market for transportation is substantial, contributing significantly to the overall engines market valued at $377.83 billion in 2024.

3.2. Market Trends and TAM

The U.S. infrastructure market, valued at over $2 trillion, offers significant growth potential. AI infrastructure, renewable energy and telecom sectors are particularly robust, driven by technological advancements and policy initiatives. The increasing digitization of industries further expands PSIX’s addressable market.

The TAM for alternative fuel engines is growing, with the gas engines market projected to reach $8.08 billion by 2032 (Gas Engine Market Size, Share, Trends | Global Report 2032). Trends include increased adoption of natural gas and stricter emission norms, benefiting PSIX's offerings.

3.3. Macro Trends

Increasing demand for data and telecom services, fueled by the rise of remote work, e-commerce, automation, IoT devices and ultimately AI surge.

Federal infrastructure spending programs aimed at modernizing aging systems.

Shift toward renewable energy sources, with solar, wind energy projects and battery energy storage gaining momentum.

Sustainability: Global push for net-zero emissions drives demand for PSIX's products.

Technological Advancements: Innovations in engine efficiency and fuel flexibility enhance market opportunities.

Regulatory Environment: Stricter emission standards, like EPA and CARB certifications, align with PSIX's focus.

3.4. Competitors

Competitors include Cummins, Generac Power Systems, IES Holdings and others, each with varying strengths in diesel, alternative fuels and power solutions. PSIX's niche in alternative fuels provides a competitive edge.

3.5. Market Share of Its Competitors

Cummins dominates with a larger market share, and over the past several decades, Cummins Inc. (CMI) has delivered a remarkable return of approximately 3,548.32% to its investors.

However, over the last five years, the entire power generation and energy solutions industry, including $PSIX and its competitors, has experienced remarkable growth too, as shown in the chart.

Driven by strong market tailwinds such as surging data center demand, renewable energy expansion, and infrastructure modernization, major players—Cummins (+146.88%), Generac (+21.82%), IES Holdings (+617.88%), and Caterpillar (+181.51%)—have delivered notable returns.

This strong performance highlights the resilience and opportunity within the power generation sector, positioning $PSIX as a key beneficiary of AI-driven data center growth and industrial energy needs. Furthermore, $PSIX's valuation remains attractive, trading at a lower forward P/E compared to its peers, while achieving significantly higher growth rates in the power generation sector.

3.6. Growth Potential

PSIX has significant growth potential, particularly in data centers and renewable energy applications, fueled by strategic partnerships and favorable market trends. Notably, the company is expanding its workforce at its Darien facility, where it manufactures power generation solutions to meet the surging demand from massive data centers.

4. Management Quality

4.1. Experience

Dino Xykis (CEO/previous CTO): Over 30 years in engineering, with roles at Cummins and Generac, appointed permanent CEO in April 2023 (Power Solutions International Announces the Permanent Appointment of Dino Xykis).

Kenneth Li (CFO): Extensive financial leadership, previously at ND Paper and Caterpillar, appointed in August 2022 (Board of Directors and Executive Officers).

Mr. Xykis:

Dino Xykis was appointed as the Chief Executive Officer on April 24, 2023. Prior to that, Mr. Xykis served as the Interim Chief Executive Officer from June 1, 2022 to April 24, 2023.

He has more than 30 years of professional experience in multi-disciplined engineering areas including senior management and executive positions, was appointed as the Company’s Chief Technical Officer on March 15, 2021. Since that time, Mr. Xykis has been responsible for the oversight of the Company’s advanced product development, engineering design and analysis, on-highway engineering, applied engineering, emissions and certification, Waterford, Michigan engineering operations, program management and product strategic planning. Since joining the Company in 2010 and until his appointment as Chief Technical Officer in March 2021, Mr. Xykis served as Vice President of Engineering for the Company. Prior to joining PSI, his previous professional experience in multi-disciplined engineering areas including senior management and executive positions includes service at various companies including Cummins Inc., and Generac Power Systems, both current competitors of PSIX. Mr. Xykis also served as Adjunct Professor of Mechanical Engineering and Mechanics at the Milwaukee School of Engineering and previously served on the audit and compensation committees of the Board of Directors of Image Sensing Systems, a publicly traded company on NASDAQ, from 1996 to 2001. Mr. Xykis also served on the advisory board of CEGE, College of Science and Engineering, University of Minnesota for eight years.

Mr. Xykis holds a Bachelor’s degree in Structural Engineering, a Master’s degree in Vibration/Dynamics, and a PhD. in Structural/Applied Mechanics from the University of Minnesota, Minneapolis.

Kenneth Li:

Has served as Chief Financial Officer since August 29, 2022.

Mr. Li is an accomplished executive who has more than 20 years of professional experience in the areas of finance, accounting, financial planning & analysis, internal controls and strategy, among others. Most recently, Mr. Li served as chief financial officer for ND Paper, a leading pulp, packaging and paper company, from 2020 to August 2022, where he was a member of the executive leadership management team with primary responsibility for finance, accounting, tax, auditing, treasury, risk management, internal audit, and strategic planning, among other areas, and served as a strategic advisor to the CEO. Prior to this role, Mr. Li was with Caterpillar Inc., from 2008 through 2020, where he served in various financial leadership positions, the most recent of which was chief financial officer of the global mining machine product group from 2013 to 2020. Prior to Caterpillar, Mr. Li was with Ford Motor Company, where he held finance leadership roles of increasing responsibility, from 2003 to 2008.

Mr. Li holds an MBA with high distinction and an M.S. in Accounting, both from the University of Michigan. He also holds an M.S. in Mechanical Engineering from the University of Oklahoma and a B.S. in Mechanical Engineering from Shanghai JiaoTong University. Mr. Li is also a CPA.

Recent Good Decisions:

Data Center Focus: Strategic shift to data centers, driving Q3 2024 growth (Power Solutions International, Inc. (PSIX) Stock Price, Quote & News).

Debt Reduction: Efforts to manage debt, with decreases noted in Q1 2024 (Power Solutions International Announces First Quarter 2024 Financial Results).

4.2. Management Shares Ownership

The ownership structure of Power Solutions International ($PSIX), as depicted in the provided table, indicates that the company has a significant controlling shareholder. Weichai holds a 51.2% stake in the company, making it the majority owner. Other notable shareholders include Gary S. Winemaster (14.5%), Neil Gagnon (10.8%), and Kenneth J. Winemaster (9.6%), with no other individual or group holding a substantial portion of the outstanding shares.

Weichai America Corp., headquartered in Rolling Meadows, Illinois, is a wholly-owned subsidiary of China's Weichai Power Co., Ltd., one of the world's largest diesel engine manufacturers. Established to expand Weichai's presence in North America, Weichai America focuses on delivering clean power solutions, including the design and manufacturing of diesel and natural gas engines for off-road applications. The company also engages in strategic partnerships to enhance its technological capabilities and market reach. Weichai Power Co., Ltd. is, in turn, a subsidiary of Weichai Group, a diversified conglomerate with interests spanning powertrains, vehicles, construction machinery, and more. Weichai Group operates under the umbrella of Shandong Heavy Industry Group, a major state-owned enterprise in China.

The most prominent risk associated with Weichai’s majority ownership is the potential for control over corporate governance and decision-making. With more than 50% of the shares, Weichai has the ability to influence key strategic decisions, including board appointments, executive leadership changes, and operational directions. This level of control could pose risks to minority shareholders if Weichai prioritizes its own interests over broader shareholder value. Additionally, regulatory and geopolitical risks could arise, especially given the scrutiny that foreign ownership—particularly by Chinese entities—often faces in industries related to energy and manufacturing.

However, it is important to note that Chinese entities do not have a historical track record of penalizing minority shareholders, reducing the likelihood of aggressive corporate actions that could harm smaller investors. Additionally, the two founders, Kenneth and Gary Winemaster, still hold a significant portion of shares, with a vast majority of their net worth tied to the company. This alignment of financial interests with the rest of the shareholders suggests that the leadership will remain incentivized to drive shareholder value rather than pursuing actions that disproportionately benefit the majority owner.

The low insider selling activity in Power Solutions International ($PSIX), despite the stock price having multiplied several times, is notable and suggests strong confidence in the company’s long-term prospects. The image shows that Gary S. Winemaster reduced his holdings slightly (-2.3%, or 68,000 shares), and Gagnon Securities, LLC made a more significant reduction (-32.3%, or 274,300 shares). However, both Weichai Power (majority owner) and Kenneth J. Winemaster have maintained their positions, with no recorded selling activity.

This low level of insider selling is significant because, typically, after a substantial stock price increase, insiders often take profits. The fact that the Winemaster family and Weichai Power continue to hold onto their shares indicates that they believe in the company's continued growth potential or that they see further upside ahead. Additionally, the entry of Portolan Capital Management, LLC as a new buyer suggests institutional confidence in the stock at current levels.

Overall, the limited insider selling despite a strong rally in share price suggests that key stakeholders align their interests with long-term growth rather than short-term profits, reinforcing stability and positive sentiment for the company's future trajectory.

4.3. Executive’s Compensation

The table below summarizes the compensation paid for the services rendered to the Company, in all capacities, by its named executive officers for the years ended December 31, 2023 and 2022.

Mr. Xykis's 2023 compensation of $216,542 in Stock Appreciation Rights (SARs) is relatively modest compared to industry peers, who often receive significantly larger stock-based compensation packages, leading to substantial dilution.

4.4. Shareholder Treatment

The total shares outstanding chart for Power Solutions International ($PSIX) shows a notable increase over time, particularly around 2018-2019, where the share count jumped significantly from approximately 10 million to over 20 million shares. This suggests a major equity issuance, likely due to capital raises or strategic agreements. A key event during this period was Weichai Power taking control of the company. In March 2019, Weichai increased its ownership stake, becoming the majority shareholder, which now stands at over 51%.

However, after this sharp increase, the share count has remained relatively stable, with only minor fluctuations from 2019 to 2024. This indicates that $PSIX has not been aggressively diluting shareholders in recent years, in contrast to many companies that continually issue shares for stock-based compensation or funding.

From a shareholder perspective, this stability is a positive sign, as it reflects management’s discipline in preserving shareholder value while ensuring financial sustainability. While past dilution may have been necessary for the company’s growth and strategic positioning, the recent commitment to maintaining a steady share count suggests a more shareholder-friendly approach going forward.

Buyback activity is not relevant, as investment are focused on increasing the capacity to feed the current demand.

5. Competitive Advantages

Keep reading with a 7-day free trial

Subscribe to Swiss Transparent Portfolio to keep reading this post and get 7 days of free access to the full post archives.