A 100x stock: Hims & Hers ($HIMS)

Following COSTCO’s recipe in HealthCare

1. Summary

1.1 Investment idea

In the ever-evolving healthcare landscape, Hims & Hers Health, Inc. ($HIMS) has emerged as a disruptive force by embracing a model that echoes the principles of Costco’s retail success. By focusing on delivering high-quality healthcare products and services at an affordable price point, Hims is redefining accessibility and value in the healthcare space. This strategy, rooted in customer-centricity and efficiency, positions the company as a long-term winner in a fragmented, costly and complex industry.

Like Costco, which thrives on a membership-based approach and economies of scale, Hims leverages its subscription model to drive predictable recurring revenue, reduce costs for consumers, and create a robust flywheel of growth. By owning the customer experience end-to-end—from telehealth consultations to prescription delivery—Hims maximizes operational efficiencies while building trust and loyalty among its users.

Furthermore, Hims capitalizes on the growing demand for digital healthcare, offering convenience and discretion for patients addressing sensitive issues such as mental health, sexual health, capillary, dermatology and beauty. This model not only attracts a wide customer base but also generates significant value through scale, much like Costco's ability to maintain lower prices by consolidating demand.

As this thesis unfolds, we will explore how Him’s strategic alignment with Costco's principles of cost leadership, operational efficiency, and customer loyalty sets it apart in the healthcare sector. We will also examine the company’s ability to sustain long-term growth through innovation, organic expansion, and a commitment to providing accessible healthcare solutions for millions of individuals.

With Hims, we see not just a healthcare provider, but a brand poised to become a household name by delivering quality care at an unmatched value—a formula that has worked wonders in other industries and has the potential to revolutionize healthcare.

1.2 Why it is compelling

Moat’s: low-cost provider and data-driven personalization in a complex healthcare system. Hims is a DTC pharmacy platform.

Revenue growth: 65% YoY and 100% over last 5 years.

Expanding TAM in telehealth and weight loss markets GLP-1s, growing Q324 4% over the total 44% growth respect Q323.

High quality execution so far by the management, with the co-founder acting as CEO.

1.3 Risks

Regulatory scrutiny, GLP-1 being removed from the FDA’s shortage list.

Intense competition, Amazon initiating pharmacy capabilities.

Stock based compensation can dilute shareholder value.

1.4 How it works

“How it Works” page on their site does a great job of explaining the business model quickly:

2. Business model

2.1 History of the company

Hims & Hers, co-founded in 2017 by Andrew Dudum, emerged as a disruptive force in the telehealth and wellness sector. The name Hims & Hers reflects the company’s mission to provide inclusive, personalized, accessible, affordable, and stigma-free healthcare solutions for both men (Hims) and women (Hers), utilizing a subscription-based direct-to-consumer (DTC) model to revolutionize patient care. Initially focused on de-stigmatizing sensitive health issues for men (e.g., hair loss and erectile dysfunction treatments), the company quickly recognized broader market opportunities. By expanding into women’s health and mental wellness, Hims & Hers established itself as a comprehensive telehealth platform catering to Millennials and Gen Z.

Hims & Hers connects customers with licensed healthcare providers through online consultations for diagnosing and treating various health conditions. After an online consultation, medications are prescribed and shipped directly to the customer’s door in discreet packaging. The platform allows users to access care from the comfort of their homes, removing barriers like long wait times or in-person visits in medical consults or pharmacies.

Key milestones include:

2017: Company founded and initial focus on men’s health.

2020: IPO via SPAC merger, marking its public market debut.

2023-2024: Rapid growth driven by GLP-1 weight loss treatments and cosmetics.

As mentioned, Hims & Hers went public through a merger with Oaktree Acquisition Corp., a Special Purpose Acquisition Company (SPAC), which was completed in January 2021. By February 2021, investor enthusiasm surrounding newly listed SPACs was still high, plus market optimism around telehealth, driving interest in Hims as a newly public company.

2.2 Key Concepts regarding its business

Hims & Hers operates a digital-first, vertically integrated telehealth model. Key components include:

· Affordable Telemedicine: Enables customers to consult licensed healthcare providers online.

Personalized Treatments: Products range from dermatology (acne, anti-aging) to sexual health and mental health (anxiety and depression medications).

Subscription Model: Revenue is primarily generated through subscription plans for recurring treatments.

Compounded GLP-1 Treatments: Recently entered the booming market for weight loss drugs, such as GLP-1-based products.

Branding and Accessibility: Aimed at younger demographics (Millennials and Gen Z), the platform emphasizes simplicity, transparency, and destigmatization of health concerns.

2.3 Revenue analysis by segments

The company derives revenue primarily from two sources:

Subscriptions (90% of revenue): Monthly and online recurring revenue from ongoing prescriptions, with a 85% long-term retention.

Non-Subscription Products (10% of revenue): Includes one-time purchases and over-the-counter health and wellness products.

Additionally, the subscriber base is segmented into personalized and non-personalized categories, with the personalized segment showing an impressive 175% year-over-year growth. This one, is one of the moats of the company, same as Spotify uses custom lists and an excellent user experience.

2.4 Capital allocation

Hims has strategically reinvested cash flow into:

Marketing campaigns aimed at growing brand awareness. Crucial for its growth.

Enhancing its product portfolio, particularly in high-margin categories like weight loss. Master movement.

Avoiding excessive leverage, maintaining a strong balance sheet. Excellent execution.

2.5 Financial health

Profitability: Achieved profitability in Q4 2023, and since then it is expanding its margins.

Revenue Growth: 65% year-over-year growth (2022-2023).

Cash Flow: Positive free cash flow (≈$80 million in Q3 2024).

Debt Management: Controlled leverage with Debt/EBITDA between 2 and 3x and more than 20x cash.

3. Market share

3.1 Company dominance in its sector

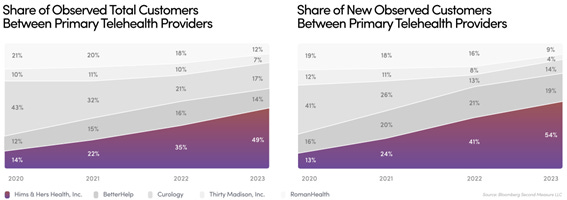

Hims & Hers has carved a niche in the telehealth industry through its DTC approach, focusing on convenience, branding, and affordability. It commands approximately 49% of the U.S. telehealth market share between the primary telehealth providers.

3.2 Market trends and TAM

Telehealth TAM: One of the most conservative studies projected to reach $450 billion by 2030, growing at a CAGR of 24%.

Weight Loss Drug Market: Expected to hit $100 billion by 2030, driven by innovations like GLP-1 treatments, according to Goldman Sachs and other top researchers, with an annual growth rate CAGR above 30%.

Mental Health Market: Increased awareness is fuelling rapid growth, with Millennials and Gen Z leading demand for affordable, digital solutions. Studies suggest a CAGR between 2-5%.

3.3 Macro trends

Post-COVID Telehealth Boom: Accelerated adoption of virtual healthcare.

Health-Conscious Consumers: Younger demographics prioritize convenience and transparency.

Image culture: acceleration in cosmetics and beauty products, skincare, fashion, etc.

Focus on Preventative Care: Shift from reactive to proactive health solutions.

3.4 Competitors

Major direct competitors include:

Teladoc Health ($TDOC): Teladoc focuses more on enterprise partnerships and insurance integrations, while Hims prioritizes a direct-to-consumer subscription-based model.

Roman ($RO): Private company, offers similar DTC telehealth services. Ro has a more clinical, less lifestyle-focused brand identity compared to Him’s modern and approachable branding.

Amazon Clinic ($AMZN): A new entrant leveraging Amazon’s massive distribution network, which enables prescription delivery with competitive pricing and fast fulfillment. However, Amazon Pharmacy lacks the telehealth consultation and holistic health offerings that Hims provides.

CVS ($VCS) & Walgreens ($WBA): CVS and Walgreens capitalize on their extensive physical presence and vertically integrated models, focusing on insured patients and managing chronic conditions. In contrast, Hims adopts a digital-first, direct-to-consumer (DTC) approach, emphasizing transparent pricing and niche healthcare services.

3.5 Market share of its competitors

The U.S. pharmacy market is largely dominated by CVS and Walgreens, forming a duopoly with significant distribution advantages. Both companies are making strides in digitization, but they may struggle to connect with digitally-native customers in the same way Hims & Hers does.

According to Statista, CVS and Walgreens lead in prescription drug market share. While their overlap with Hims is currently minimal, their paths are converging. Hims operates outside the traditional PBM/insurance framework but competes for the same consumer attention. As Hims expands its offerings, competition between the two models is likely to intensify.

Looking ahead a decade, it’s not far-fetched to imagine Hims managing hundreds of proprietary facilities nationwide, potentially serving 100 million Americans. This could significantly challenge CVS and Walgreens, particularly if Hims undercuts insured out-of-pocket costs with lower pricing.

As digital convenience becomes an increasing consumer expectation and healthcare prices continue to rise, the macro environment grows increasingly volatile. While CVS and Walgreens have their differences—and a fascinating history of rivalry—their physical presence could become both their vulnerability and their advantage.

In a future value-based healthcare system, physical patient interactions will gain importance, as ongoing monitoring ensures treatments are effective. CVS and Walgreens are well-positioned to capitalize on this opportunity through their physical footprint, which could become a critical asset as the industry shifts toward outcome-driven care.

For now, however, the traditional system’s limitations often leave patients underserved, a gap that Hims is uniquely positioned to address with its digital-first, customer-centric approach.

3.6 Growth potential

Hims’ growth drivers:

Potential expansion into high-margin weight loss drugs.

Highly favorable macroeconomic and market tailwinds, as seen in previous chapters.

Increasing customer lifetime value (LTV) through bundling services.

International expansion potential in Europe and Canada.

4. Management quality

4.1 Experience

The management team displayed in the image is composed by experienced leaders with diverse expertise across major industries:

The team combines expertise from top-tier companies in technology, healthcare, retail, and design, demonstrating a well-rounded approach to scaling and innovation in digital healthcare.

Andrew Dudum, co-founder of Hims & Hers, has served as the Chief Executive Officer and a board director since September 2016. Before founding Hims, Dudum co-founded Atomic Labs, a startup studio and investment fund, where he played a pivotal role in launching a range of innovative companies, including Bungalow, Homebound, TalkIQ, and Terminal, as General Partner. A true serial entrepreneur, Dudum continues to thrive as an active angel investor and trusted advisor to numerous startups, including Cherubic Ventures, an early-stage venture capital firm with operations in both China and the U.S. His accomplishments earned him recognition on Fortune’s 40 Under 40 list in 2020.

4.2 Mangement shares ownership

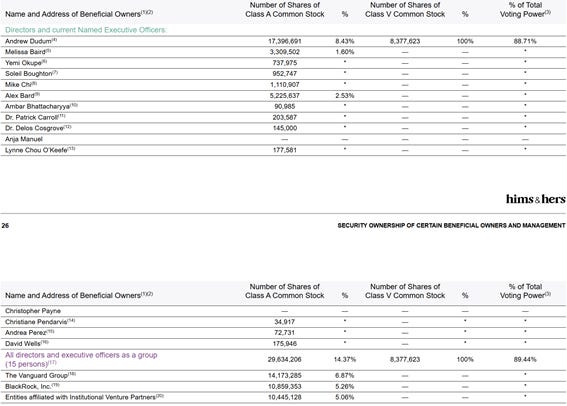

According to the DEF 14A filing from 2Q23 and the 2Q24 report, CEO and co-founder Andrew Dudum held 9.43% of Hims & Hers outstanding shares in 2023, which decreased to 8.43% in 2024.

As of December 2024, he holds approximately 10.5 million shares, representing about 5% of the total outstanding shares, equating to approximately $262 million in stock value at the current share price of $25. This is a stark contrast to his 2023 base salary of $612,000 and his substantial stock-based compensation (SBC) package of $11 million in stock awards in 2023.

The salary plus the SBC package represents the 4.4% of his total stake in the company by December 2024, indicating a strong alignment with shareholder interests.

Including Dudum’s stake, all directors and executive officers held 14,37% of the company by 2Q24. However, it is important to note that excessive reliance on stock-based compensation (SBC) can dilute shareholder value if not managed carefully. Additionally, since then, Mr Dudum has been gradually reducing his stake in the company, taking advantage of recent peak stock prices at the range of $30.

4.3 Executive’s compensation

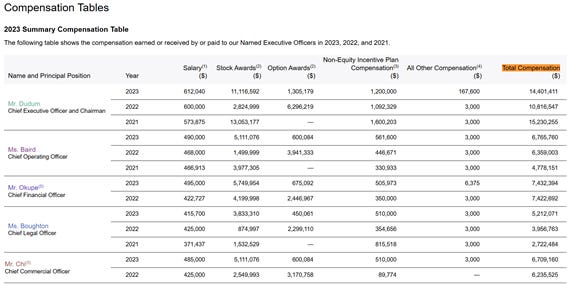

If we compare the salary of the CEO with his stake on the company:

2023 salary: $612,000.

2023 SBC: more than $11 million.

2023 Total compensation: $14.4 million.

Ownership value: estimated today at $262 million, showcasing strong alignment with shareholder interests and representing more than 18x his total compensation in 2023.

4.4 Shareholder treatment

The gradual increase in shares, 11% YoY, is partly attributable to SBC, which aligns management and employee incentives with shareholder interests. However, this approach can lead to dilution, impacting existing shareholders if not carefully managed.

On the other hand, in 2024, Hims & Hers executed share repurchase programs totaling $80 million, acquiring approximately 5.77 million shares of its Class A common stock, which reflect the company's confidence in its financial health and commitment to enhancing shareholder value.

4.5 Recent good decisions

Strategic entry into the GLP-1 weight loss market.

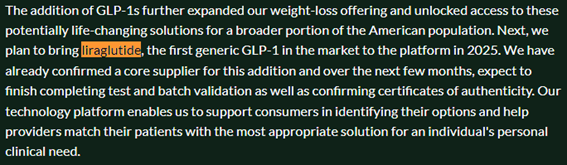

If GLP-1 drugs like semaglutide are removed from the FDA’s shortage list, Hims may face increased competition, pricing pressures, and potential regulatory challenges. However, it could mitigate these risks by introducing liraglutide (Saxenda/Victoza) as an alternative for weight loss and diabetes management, leveraging its proven effectiveness and availability. By emphasizing affordability, convenience, and personalized care, Hims can differentiate itself in a competitive market, reduce reliance on semaglutide, and expand its customer base, maintaining its growth trajectory despite market shifts.

Andrew Dudum, 3Q24:

Investments in compounding capabilities through a 503(a) facility.

Andrew Dudum, 2Q24:

503(a) facilities allow for the preparation of compounded medications tailored to individual patients’ needs, such as GLP-1 weight loss treatments, which are a growing market for Hims.

Recently added Dr. Shepherd to the team to be the Chief Medical Officer of Hers.

Her expertise & the expansion to other areas like Menopause & Hormonal therapy could be the extra mphh needed to get the female audience larger than mens.

5. Competitive advantages

5.1 Advantages vs competitors

DTC Branding: Strong connection with Millennials and Gen Z.

Subscription Model: High customer retention and recurring revenue.

MedMatch: a service that leverages the collective knowledge of thousands of providers, and millions of data points, to assist Hims providers with offering treatments/prescriptions with the greatest chance of success to patients.

Low-Cost Operations: Minimal overhead compared to traditional healthcare providers.

As Jassy (CEO of Amazon) mentions, the pharmacy business is extraordinarily complex, and Hims’s vertically integrated model adds another layer of sophistication. At this stage, the combination of its digital front-end and automated back-end creates a highly defensible operation.

Andrew Jassy, 4Q2023:

Keep reading with a 7-day free trial

Subscribe to Swiss Transparent Portfolio to keep reading this post and get 7 days of free access to the full post archives.