PSIX Record Q2

Undervalued Gem or Priced for Perfection?

Few things capture investors’ attention like a company smashing its own records, and Power Solutions International (NASDAQ: PSIX) just did exactly that. The engine and power systems maker delivered a blowout Q2 2025, fueling a massive rally in its stock price (+11% after hours).

Since our deep dive on March 5, the stock has delivered a +3x return on our initial investment. In our PSIX Earnings Preview, we reiterated our conviction with a “Hold” rating, citing the company’s strong growth potential.

Now the burning question is whether PSIX remains a bargain with tailwinds at its back or if the market has already priced in the good news. Let’s break down the key highlights and what they mean for its valuation going forward.

Q2 2025: By the Numbers (Record-Breaking Highlights)

PSIX’s second quarter 2025 results weren’t just good, they were record-setting and well above last year’s levels. Key highlights include:

Record Net Sales: $191.9 million for Q2, up a staggering 74% year-over-year, driven by booming demand in its power systems segment.

Soaring Profits: Net income of $51.2 million, a 138% jump from a year ago, with diluted EPS of $2.22 (up 136% YoY). This surge was boosted by a one-time tax benefit (~$29.2M from releasing deferred tax allowances) that resolved prior “going concern” issues. Even without that one-off gain, underlying earnings improved significantly, reflecting strong operational performance.

Gross Profit Up, Margins Mixed: Gross profit climbed 54% to $54.1 million, although gross margin dipped to 28.2% (from ~31.8% a year ago) due to a higher mix of lower-margin products and some temporary production inefficiencies. In other words, PSIX sold a lot more, but at slightly lower margin, a trade-off that still boosted overall profit.

Healthier Balance Sheet: The company paid down $15 million in debt and fully repaid a prior shareholder loan. It also secured a new $135 million revolving credit facility extending to July 2027, enhancing financial flexibility. Cash on hand was nearly $49.5 million as of quarter’s end, giving PSIX a solid liquidity cushion.

Notably, this blockbuster quarter builds on momentum from earlier in the year, Q1 2025 saw sales up 42% and EPS more than double. In short, PSIX has strung together consecutive strong quarters, signaling that its turnaround is in full swing.

Big news at Swiss Portfolio

Enjoying these earnings reviews?

💥 Full access is just $39.99/year, more value and transparency than most $300+ memberships out there.

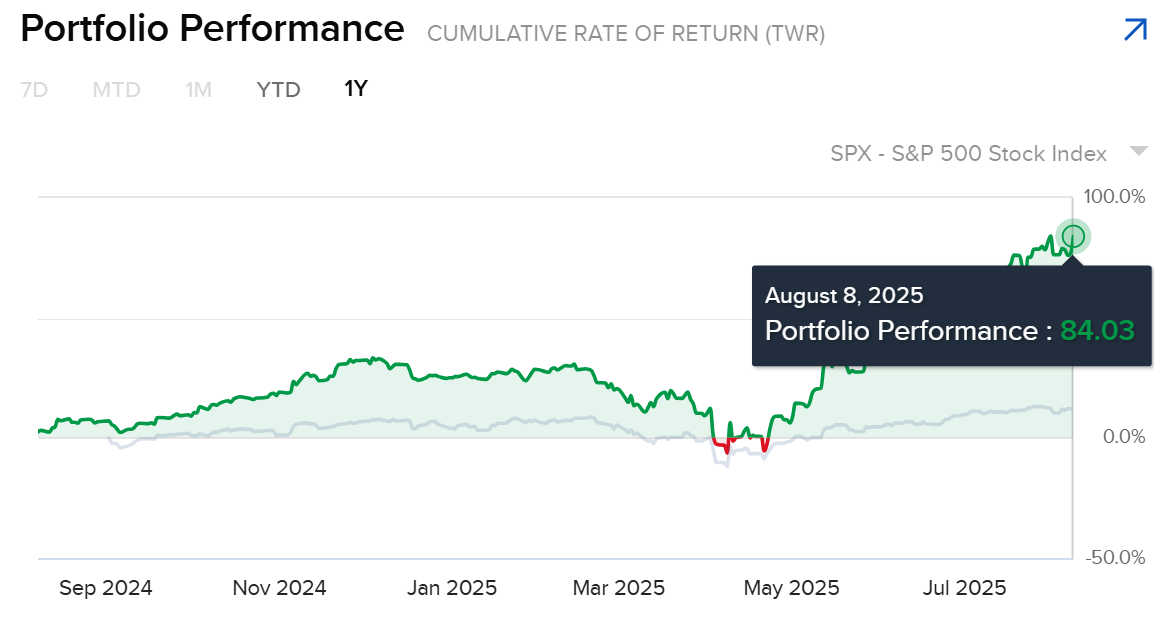

Over the past 12 months, our portfolio has returned close to 7x the S&P 500, and we publish every move with full transparency. In a world where most of finance hides behind paywalls and vague claims, we do things Swiss-transparently.

That’s not by chance. It’s the result of deep research, disciplined capital allocation, and a focus on durable, capital-light compounders, with strong management, sector tailwinds, and attractive valuations, often well before they’re widely recognized.

Become a member and you’ll gain full access to:

✅ Full access to Swiss Portfolio positions + monthly allocation updates.

✅ At least 1 high-conviction deep dive every month.

✅ Downloadable financial models to follow and stress-test each thesis.

✅ Live idea tracking once they spike, plus an S&P tracking template.

✅ Exclusive Swiss-based insights on investing, residence, and tax optimization.

🧠 The $39.99 subscription pays for itself a few times over, sometimes in just one deep dive. This isn’t about hype. It’s about transparency, consistency, and long-term compounding.

If you share our philosophy of identifying scalable compounders in high-quality jurisdictions backed by durable megatrends, we strongly encourage you to explore how past ideas have performed (current date 8.8 before market open) :👇

HIMS +97% since deep dive (13.1)

IESC +46% since deep dive (9.2)

PSIX +182% since deep dive (5.3)

SPGI +15% since deep dive (14.3)

WST +15% since deep dive (22.5)

SGX: BBW -3% since deep dive (9.6)

SWX: SQN +27% since deep dive (26.6)

What’s Fueling the Growth? (Data Centers, Oil & Gas, and More)

The power systems segment is the engine behind PSIX’s record results. In Q2, power systems sales surged by $83.8 million, especially thanks to soaring demand from data center customers and oil & gas projects. This isn’t a one-quarter wonder either, it’s part of a broader trend. The rise of AI-driven data centers and the need for reliable backup power have opened a lucrative new market for PSIX’s emissions-certified generators and integrated power solutions. These products carry higher margins and leverage PSIX’s engineering expertise, giving the company a foothold in a booming space. As the expansion of cloud and AI infrastructure drives 15% annual growth in data center capacity globally, PSIX is positioned to ride this wave.

As Dino Xykis, Chief Executive Officer, commented:

“We are very pleased with our second quarter results, which marks the strongest sales and profit performance in our Company’s history. Achieving 74% year-over-year sales growth and 138% increase in net income reflects strong demand for our power systems solutions, the disciplined execution of our strategy, the commitment and dedication of our employees, and favorable tax benefits”.

Beyond data centers, the company’s diversification into renewable energy components and custom power units also provides secular tailwinds. And while industrial and transportation equipment sales have been relatively flat or soft (with some weakness in material handling noted in Q1), the overall outlook remains positive: management “anticipates continued growth in 2025, driven by power systems market expansion, especially in data centers”. Importantly, PSIX’s recent inclusion in the Russell 2000 and Russell 3000 indexes underscores its progress and is likely bringing new investor attention.

Financially, PSIX is far more robust than it was a couple of years ago. Debt is down, interest expense is falling, and cash flow is strong. By repaying debt and extending its credit line, the company has reduced risk and gained flexibility to invest in growth. This strengthened balance sheet, combined with tailwinds from high-growth end markets, forms the crux of the bull case that PSIX can sustain its earnings trajectory.

Valuation Check: Still Undervalued or Now Fully Priced?

With such explosive growth, PSIX’s stock has been on a tear, roughly a 700% gain in the past 12 months. A year ago, this was a sub-$11 stock; recently it touched all-time highs around $100. After a rally of that magnitude, it’s fair to ask: Has PSIX become expensive, or does it remain a hidden gem?

Here’s where things get beautifully interesting.

Want to see the updated model, valuation ranges, and our Final Verdict? 👇

Keep reading with a 7-day free trial

Subscribe to Swiss Transparent Portfolio to keep reading this post and get 7 days of free access to the full post archives.