The Single Biggest Investment Opportunity of this decade

Oracle just kicked off the AI earnings season. What happens next?

Oracle, long written off as a legacy snoozer, just posted 11% revenue growth and 50%+ cloud infrastructure growth. That’s not normal. That’s an inflection point. And when a company its size starts throwing around phrases like “skyrocketing demand” and “70%+ growth next year”, you’d be wise to pay attention.

But this isn’t about Oracle alone. It’s the clearest signal yet that we’re entering a full-blown AI infrastructure supercycle, where cloud, chips, power, and pipes all converge into one secular megatrend.

Earnings season is coming. If Oracle’s results are the overture, the symphony is about to get loud.

Here’s what to expect, and how to position before the next wave hits.👇

Oracle’s Blowout FY2025 Finish

Let’s first take a look at Oracle’s earnings release from June 11. The company wrapped up fiscal 2025 on a high note, posting surprisingly strong growth for a firm often seen as a legacy tech incumbent. In Q4 (ended May 31, 2025), total revenue rose 11% year-over-year to $15.9 billion, an acceleration driven largely by its cloud businesses.

Cloud revenue (SaaS + IaaS) jumped 27% to $6.7 billion in the quarter, with infrastructure-as-a-service (OCI) growing a stunning 52% to $3 billion. This helped push full-year revenue up 8% (to $57.4 billion) despite Oracle’s massive size. The bottom line looked solid as well, Q4 delivered $1.70 in non-GAAP EPS, comfortably outpacing consensus, indicating Oracle is not only growing but doing so profitably.

The real eye-opener was management’s bullish outlook. CEO Safra Catz proclaimed FY2025 was

“a very good year, but we believe FY2026 will be even better”,

forecasting Oracle’s cloud growth to accelerate from 24% last year to over 40% in FY2026, with OCI (infrastructure) revenue growth jumping from 50% to over 70% next year. A key reason is its swelling order pipeline, remaining performance obligations (backlog for future revenue) reached $138 billion, up 41%. In other words, demand is so strong that Oracle is booking record future business, foreshadowing much faster growth ahead as those contracts get fulfilled. Oracle’s Chairman Larry Ellison noted that consumption of Oracle’s cloud services is “skyrocketing” and demand is “soaring” heading into FY2026. This kind of language, paired with hard numbers, suggests Oracle has hit an inflection point, transforming from a slow-and-steady software giant into a serious hyper-growth cloud contender.

The Cloud Wars Just Got Interesting

Oracle’s resurgence doesn’t happen in a vacuum, it sends ripples across the entire tech landscape. First and foremost, it underscores that enterprise cloud demand remains robust. In fact, global spending on cloud infrastructure services jumped 23% year-over-year to $94 billion in Q1 2025, the fastest growth in six quarters. Oracle’s piece of that pie is still modest (about 3% market share), but the company’s ability to grow 50%+ in cloud infrastructure signals that the cloud market still has plenty of juice left. For the “Big Three” cloud providers, Amazon AWS, Microsoft Azure, and Google Cloud, Oracle’s success is both a validation and a warning. It validates that enterprises are still rapidly migrating workloads to the cloud, including mission-critical systems (databases, ERPs) that Oracle specializes in. At the same time, Oracle’s momentum hints at customers embracing a more multi-cloud approach, rather than relying on a single vendor. In fact, Oracle saw its database revenue from AWS, Google, and Azure environments soar 115% sequentially in Q4, as companies deployed Oracle’s tech across those platforms. This suggests the days of one cloud to rule them all are fading, even rivals are collaborating. For instance, Oracle and Microsoft now partner so customers can run Oracle databases natively on Azure datacenters (with 23 such “multi-cloud” datacenters live and 47 more being built). Same story between OpenAI and Google, where OpenAI has signed up for Google Cloud service to meet its growing needs for computing capacity. The takeaway: cloud giants are realizing that cooperation, not just competition, is what customers want, even if the headlines shift day by day.

What might we expect when these cloud titans report their own earnings? Likely more of the same robust growth, with an AI-powered kicker. In Q1 2025, Google Cloud grew revenue 28% to $12.3 billion, still the fastest-growing major cloud player. Microsoft doesn’t break out Azure dollars, but it disclosed Azure and related cloud services grew 33% year-on-year last quarter, an uptick that Microsoft attributed to strong demand for AI services. AWS, the largest provider, is growing a bit more slowly (17% YoY last quarter) but at immense scale (~$117 billion annual run-rate). Notably, all three have highlighted surging interest in AI workloads (training models, hosting generative AI services) as a new growth driver. Azure’s 33% jump came as it rolled out OpenAI services; AWS is investing heavily in its Bedrock AI platform and custom AI chips (Trainium, Inferentia), CEO Andy Jassy recently touted that AWS’s latest chips

“make it easier… to train models and run inference more cost-effectively”.

Google, meanwhile, is racing to add GPU capacity after demand briefly outstripped its data center supply. In short, cloud earnings this year won’t just be about generic compute and storage, they’ll be an AI arms race. We should watch for guidance on cloud capex and order backlogs: so far, all signs point to aggressive spending. Microsoft said it plans to invest ~$80 billion in data centers for fiscal 2025, and Amazon indicated its 2025 capital spending will top the estimated $75 billion it spent in 2024. These staggering sums (echoed by Oracle’s own build-out of 47 new cloud data centers) tell us the major players are betting big that demand will justify the investment.

Even companies adjacent to the public cloud have reasons to cheer Oracle’s news. Enterprise software firms like Salesforce, SAP, or ServiceNow may find that if Oracle’s customers are increasing IT spend, others likely are too, a healthy sign for software budgets broadly. And consider the digital advertising giants: while Oracle’s results don’t directly reflect consumer ad spending, they do reflect a resilient economy on the enterprise side. If businesses are maintaining strong tech investment, it often correlates with confidence that can trickle into advertising and marketing spend (good news for Alphabet’s and Meta’s ad revenues). Moreover, both Google and Meta have their own cloud-like infrastructure needs for search, social media, and AI, and they are spending lavishly to keep up. Meta in particular has entered the fray as an infrastructure heavyweight. CEO Mark Zuckerberg has declared 2025

“a defining year for AI”

and plans to spend as much as $65 billion this year to expand Meta’s AI supercomputing capabilities. Meta is building a new 2-gigawatt data center (the scale of a small power plant) and aims to have 1.3 million Nvidia GPUs in operation by year-end, making it one of the world’s largest AI compute clusters. This arms race in AI blurs the line between traditional cloud providers and tech giants like Meta. Ultimately, whether it’s AWS, Azure, Google, or even Meta’s internal AI farm, all are racing to build more cloud capacity. Oracle’s confidence simply confirms that the winners in tech will be those who invest boldly in infrastructure and AI to meet the surging demand.

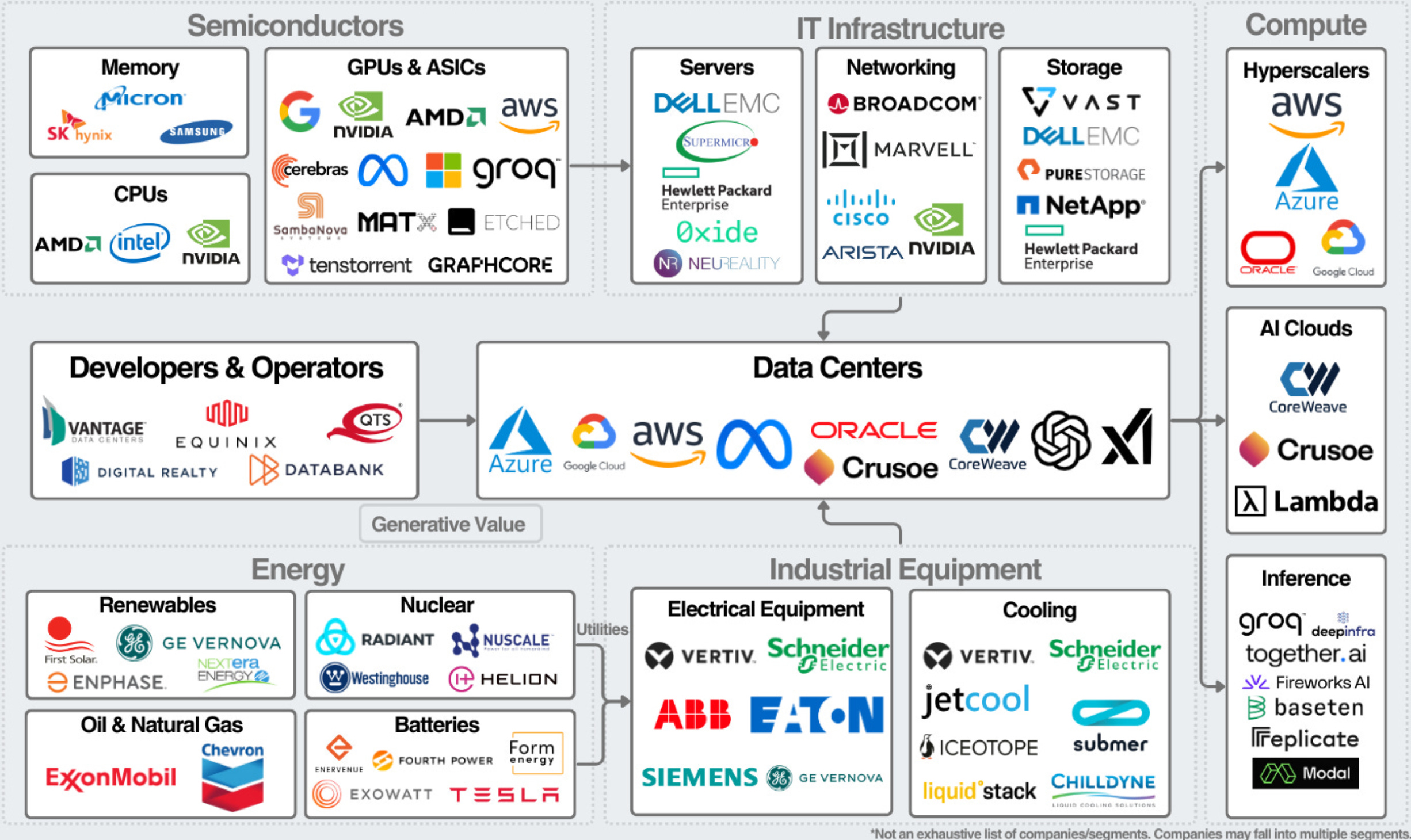

The AI Gold Rush for Chipmakers and Suppliers

If cloud providers are the new gold mines, then semiconductor firms are selling the shovels, and business is booming. Oracle’s planned 70% surge in cloud capacity next year implies enormous orders for the chips and hardware that power these data centers. We’ve already seen this play out dramatically: Nvidia, the dominant supplier of GPUs for AI, reported a record $60.9 billion in revenue for its fiscal 2024 (up 126% year-on-year), fueled by seemingly insatiable demand from cloud and AI customers. Nvidia’s data center revenue quadrupled last year, and with Oracle and others scrambling to add GPU clusters, Nvidia’s forward guidance has been stratospheric. Every big cloud and social media firm (Oracle included) is buying Nvidia’s latest H100 and A100 processors by the tens of thousands, resulting in shortages and long lead times. It’s no wonder Nvidia’s CEO remarked that

“accelerated computing and generative AI have hit the tipping point”,

with demand surging across industries.

Advanced Micro Devices (AMD), while a step behind Nvidia in AI chips, is now coming on strong. AMD’s data center segment (which sells EPYC server CPUs and Instinct AI accelerators) nearly doubled in revenue last year to $12.6 billion. In Q4 2024, AMD shipped a record $3.9 billion of data center products (+69% YoY) as it ramped up its new MI300 AI accelerators alongside its well-entrenched EPYC CPUs. CEO Lisa Su projects

“continued growth”

ahead as more cloud providers test out AMD’s MI300 chips as a lower-cost alternative to Nvidia. If Oracle’s bullish forecast holds, even a secondary supplier like AMD should see plenty of new orders for both its CPUs (many cloud companies, Oracle included, use AMD EPYC processors in their servers) and GPUs. Marvell Technology, which specializes in the high-speed networking and custom silicon that tie these supercomputers together, is another quiet winner. Marvell’s latest quarter saw data center revenues soar 78% year-on-year, now making up 75% of its business. Its CEO highlighted record demand for network interconnect chips (like 400G/800G Ethernet and optical DSPs) used to wire up AI clusters. In fact, Marvell’s custom AI silicon programs (chips developed in partnership with hyperscale cloud operators) have moved into volume production and the company is guiding for 60%+ total revenue growth next quarter. That kind of outlook from a chip supplier is a strong tell: it means their customers (the cloud and telecom giants) have placed orders hand over fist, expecting significant near-term expansion.

It doesn’t end with the chip designers. Arm Holdings ($ARM), whose energy-efficient CPU architecture powers many data center chips, is enjoying a renaissance as the industry races to optimize performance-per-watt. Arm’s leadership recently said they expect to capture 50% of the data center CPU market by the end of 2025, up from roughly 15% in 2024, thanks to the AI boom driving adoption of Arm-based servers. This isn’t wishful thinking: Amazon’s AWS already uses Arm-based Graviton processors for more than half of its new server capacity, and both Microsoft and Google have internally designed Arm server chips in the works. Oracle too offers Arm-based instances (using Ampere’s Altra chips) on its cloud, again highlighting how power efficiency and cost advantages are shifting industry standards. A massive build-out of data centers also spells good news for the likes of TSMC and ASML, the one-two punch behind global chip manufacturing. TSMC (Taiwan Semiconductor) is the contract producer for Nvidia, AMD, Apple and others at the cutting-edge; it saw a 30% jump in revenue in 2024 (to $90 billion) largely on “robust AI-related demand” for advanced 5nm/3nm silicon. TSMC’s management expects 2025 to be another “healthy growth year,” citing an accelerating structural need for high-performance, energy-efficient computing as

“everything becomes more intelligent and connected”.

This aligns perfectly with Oracle’s narrative that we’re in the early innings of a multi-year tech investment cycle. Meanwhile, ASML, which monopolizes the extreme ultraviolet lithography machines needed to fabricate the most advanced chips, continues to operate at full capacity. ASML’s order backlog sits around €36 billion (nearly a year’s worth of sales), and the company is forecasting growth to ~€30–35 billion in revenue for 2025. ASML’s CEO explicitly noted that the rise of AI is a “key driver” for the semiconductor industry’s growth outlook, even if not all market segments benefit equally. In short, from fabless chip designers to equipment makers, the entire semiconductor supply chain is being lifted by the AI/cloud tide. Upcoming earnings from these companies should reflect record backlogs, upbeat guidance, and perhaps continued constraints in meeting demand, high-class problems to have.

The Other Winners of the AI Boom

One often overlooked angle of this tech expansion is the physical infrastructure and industrial economy supporting it. Behind every shiny new data center loaded with advanced chips lies a mountain of concrete, steel, power equipment, and skilled labor, and this is creating opportunities for a different set of companies.

Take IES Holdings ($IESC), for example. IES is a specialty contractor that designs and installs electrical and technology systems in buildings, with a booming niche in data centers. As hyperscalers like Oracle, Amazon, and Meta race to erect or expand server farms, firms like IES are in high demand to wire up these facilities and ensure they run flawlessly. In fact, IES’s communications segment (which includes data center work) saw 41% year-over-year revenue growth in the latest quarter, and its backlog hit a record $1.8 billion, much of it tied to data center and infrastructure projects. The company even invested in a new $50 million manufacturing facility in Birmingham to produce custom-engineered power systems for hyperscale data centers. Industry analysts project data center construction spending will reach $250 billion globally by 2026, which provides a strong multi-year tailwind for IES and peers. In short, the more Oracle and friends build, the more revenue flows to these specialty infrastructure players play.

Similarly, Power Solutions International ($PSIX) stands to benefit from the data center boom, albeit in a different way. PSI makes large, emission-certified engines and generators that run on natural gas and other fuels, essentially providing backup and prime power systems for industrial sites. Data centers, which can’t afford a second of downtime, rely on robust backup power generators to kick in during outages or peak load times. PSI has identified this trend: the company guided for increased sales in 2025 driven by demand for power systems supporting data centers. Its product lineup includes big gensets and custom enclosures specifically for mission-critical facilities like server farms. So as Oracle and others build those 2 GW mega-data centers, companies like Power Solutions are likely to be supplying the hefty backup generators and microgrid components to keep them running 24/7. Indeed, this segment helps offset softness in some of PSI’s other markets (like general industrial or transport), making the data center trend a key growth driver for the firm. We should watch for PSI’s upcoming earnings to see if orders from tech infrastructure projects are accelerating, an indicator that the digital build-out is spilling over into old-school manufacturing.

Beyond these two, there’s a wider ecosystem of “digital infrastructure” beneficiaries. Real estate investment trusts like Equinix and Digital Realty trust are leasing record amounts of colocation space to cloud providers. Electrical equipment makers (Schneider Electric, Eaton) are seeing strong demand for switchgear and cooling systems for new server halls. Even construction machinery could get a lift, someone has to grade the land and construct these massive facilities. The key point for investors is that the tech boom is not confined to Silicon Valley darlings; it extends to steel in the ground. Oracle’s ambitious expansion plans (and similar moves by its peers) effectively guarantee a steady stream of work for these enabling industries in the coming years. When a company like Oracle says it’s building nearly 50 new data centers in the next 12 months, that translates into billions of dollars of construction contracts, electrical components, generators, fiber optics, and more. The guidance trends we’re hearing, e.g. Oracle expecting RPO (orders) to double again next year, or Meta boosting capex to unprecedented levels, give real businesses the confidence to hire, invest, and expand to meet this demand. It’s a virtuous cycle: robust tech investment begets robust industrial activity.

The Calm Before the Earnings Storm

Stepping back, Oracle’s strong quarter and even stronger outlook may be just the opening act of a broader tech earnings supercycle driven by cloud and AI. When a traditionally mature company accelerates growth and speaks of “skyrocketing” demand, it suggests something fundamental is shifting. In this case, that something is the dawn of AI-as-a-service at scale, enterprises are not just migrating to the cloud for storage or CRM, they’re racing to deploy AI capabilities, and they need infrastructure yesterday. Oracle’s results tell us that even second-tier players are catching a massive tailwind. This bodes well for upcoming reports from the household names: we can reasonably expect upbeat commentary and guidance from the likes of Microsoft, Amazon, Google, Nvidia, etc., especially on anything AI-related. Investors should pay close attention to guidance in particular, management teams now have enough visibility (thanks to huge backlogs and bookings) to confidently predict growth through 2025 and beyond, and many are doing exactly that.

Oracle’s stock has already been on a tear this year as the market catches on to its cloud pivot. But if their forecast of 40%+ cloud growth in FY2026 materializes, there could be significant upside left as the market reprices Oracle from a low-growth legacy multiple to a high-growth cloud multiple. The same repricing story could apply to other players: for instance, some industrial “sidekicks” (like IESC or PSIX) are still valued as cyclicals, but their alignment with secular tech trends might merit a second look. At the same time, richly valued leaders (say a Nvidia trading at high multiples) will need to keep delivering hyper-growth to justify those prices, so far, they’ve done so in spectacular fashion. The current environment is a reminder that in tech, fortune favors the bold. Oracle was bold in reinventing itself for the cloud era, and now it’s reaping the rewards. Others are equally bold in pouring capital into AI. The suspense for investors is: who will emerge as the biggest winner of this coming wave?

As we look to the coming earnings season and year ahead, the stage is set for some blockbuster reports. There’s a palpable sense of momentum across the sector, something we haven’t felt at this scale since perhaps the early cloud computing boom or the mobile revolution. Institutional investors seem to agree: according to Bank of America, net buying of tech stocks by institutional clients just hit the highest level in their data history going back to 2008. That’s not retail hype, that’s serious capital repositioning ahead of what many expect to be a historic AI-led earnings cycle.

Yet, we should also remain vigilant. Rapid growth can attract competition (Oracle itself proves that newer entrants can claw into markets thought impenetrable), and macroeconomic wildcards could always test the resilience of these optimistic forecasts. For now, however, the message is clear: the AI-enabled cloud boom is in full swing, and Oracle’s surprise leap forward is just one chapter of a much larger story unfolding across tech. This could be the “single biggest investment opportunity” in tech infrastructure of this decade, but as always, we’ll be tracking the data and results quarter by quarter to see how the thesis plays out. One thing’s for sure: with growth numbers like we’re seeing, it’s going to be an exciting ride for those of us watching (and investing in) these transformative trends.

Something Big is coming to Swiss Portfolio

To tilt the odds in your favor, you need to know where to look: across sectors, across borders, exceptional businesses, led by exceptional management teams, and across long-term themes with structural tailwinds. The key is pairing great businesses with the right markets, and ensuring management has both skin in the game and a track record of disciplined capital allocation.

If you share my approach to selecting compounders in high-quality jurisdictions with favorable megatrends, I strongly recommend double-checking my past deep dives: 👇

HIMS +92% since deep dive (13.1)

IESC +29% since deep dive (9.2)

PSIX +108% since deep dive (5.3)

SPGI +8% since deep dive (14.3)

DUOL +3% since deep dive (1.5)

WST +5% since deep dive (22.5)

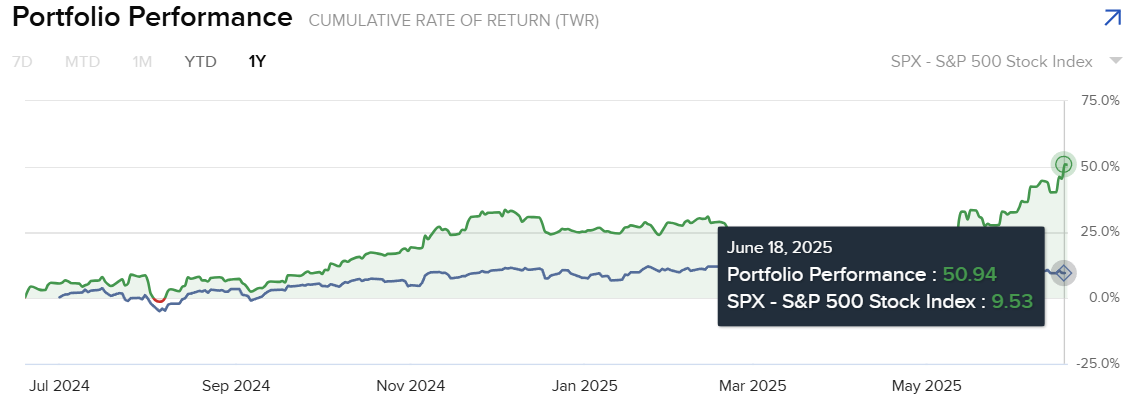

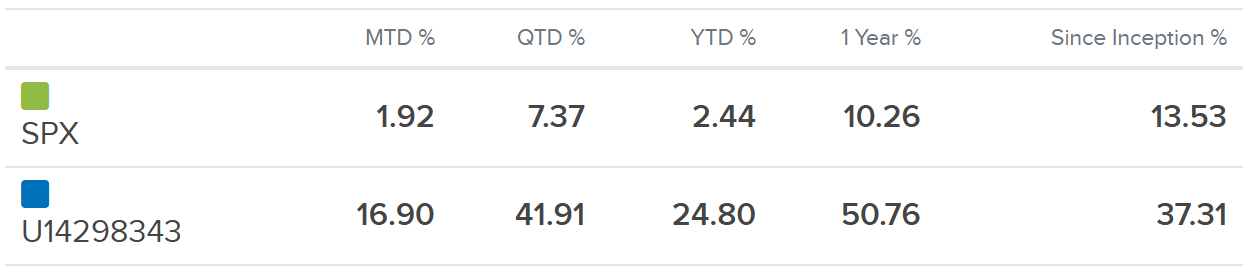

These ideas haven’t just looked good on paper, they’ve delivered. Over the past year, my portfolio is up +50%, handily outperforming the S&P 500’s +9.5%, as shown in the chart below. That’s a +40 percentage point edge driven by focused, thesis-backed positions in companies with strong management, sector tailwinds, and attractive valuations. It’s the compounding effect of being early in high-quality setups:

🚀 Coming soon on the Substack:

👉 In upcoming posts, I’ll cover:

A full deep dive on an under-the-radar company benefiting from the AI megatrend (free).

How to optimize taxes when investing from Switzerland, a huge advantage vs US & EU (free).

Continued deep dives on asymmetric opportunities I’m tracking, including my recent Azeus deep dive (free).

The “move to Switzerland” playbook for investors and entrepreneurs (paid).

My personal Swiss allocation strategy, which has returned 50%+ in a year and 30%+ CAGR over the past 5 years (paid).

If you find the kind of knowledge packed into these deep dives valuable, not just theory, but returns that beat the market by over 40 percentage points, I’d genuinely appreciate a subscribe, like, or comment. This isn’t fluff. It’s a conviction-driven approach to finding real compounders with asymmetric upside. I’ll keep sharing deep dives and commentary on high-quality businesses, special situations, and tax-optimized investing. If that’s your playbook too, you know what to do 😉 ⬇️.

Disclaimer

These opinions are solely those of the individual author. The content of this material is provided for educational purposes only and does not constitute investment advice. No discussions herein should be interpreted as an offer to sell or a solicitation to buy any securities of any company. All information is subjective, and readers are encouraged to conduct their own due diligence.

Swiss Transparent Portfolio makes no representations, warranties, or guarantees, whether express or implied, regarding the accuracy, reliability, completeness, or reasonableness of the information provided in this material. Any assumptions, opinions, or estimates expressed reflect the author’s judgments as of the date of publication and are subject to change without notice. Any projections included are based on various market condition assumptions, and no assurances can be made that the projected outcomes will be realized.

Swiss Transparent Portfolio disclaims any liability for direct, consequential, or other losses resulting from reliance on the content of this material. Swiss Transparent Portfolio does not serve as your financial, legal, accounting, tax, or other adviser, nor does it act in a fiduciary capacity.

⚡ If you enjoyed the post, please feel free to share with friends, drop a like and leave me a comment. I will thank you for that.

You can also reach me at:

X: @SwissTportfolio