Swissquote (SWX: SQN): Fintech Growth with Swiss Precision

Record-Breaking 2024 Financial Performance 🚀

To tilt the odds in your favor, you need to know where to look: across sectors, across borders, exceptional businesses, led by exceptional management teams, and across long-term themes with structural tailwinds. The key is pairing great businesses with the right markets, and ensuring management has both skin in the game and a track record of disciplined capital allocation.

In my ongoing search for these rare compounders, Swissquote (SWX: SQN) stands out. It checks several of the boxes: a founder-led fintech scaling internationally, riding the secular shift toward self-directed investing, and compounding profits with remarkable efficiency. It’s also one of the top ideas I flagged in my recent piece, “20+ Swiss Stocks to Buy and Sleep Well”.

If you share my approach to selecting compounders in high-quality jurisdictions with favorable megatrends, I strongly recommend double-checking my past deep dives: 👇

HIMS +60% since deep dive (13.1).

IESC +23% since deep dive (9.2).

PSIX +99% since deep dive (5.3).

SPGI +7% since deep dive (14.3).

DUOL +0% since deep dive (1.5).

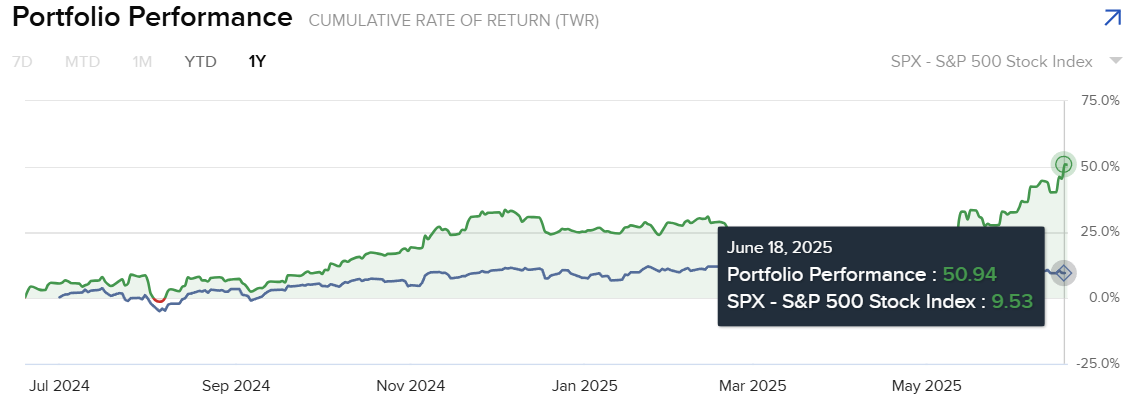

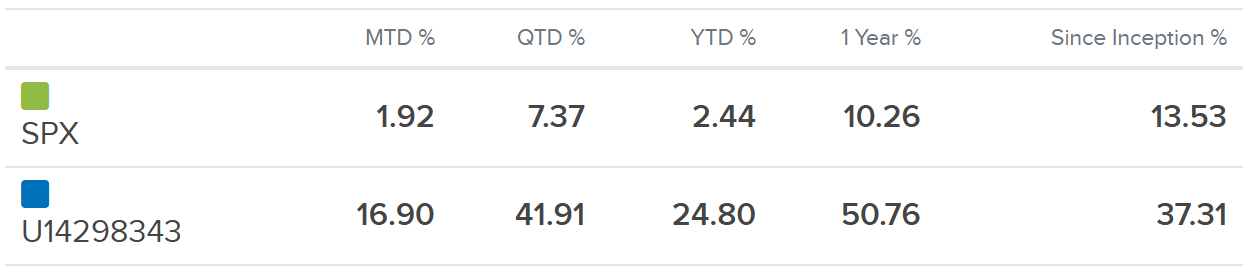

These ideas haven’t just looked good on paper, they’ve delivered. Over the past year, my portfolio is up +50%, handily outperforming the S&P 500’s +9.5%, as shown in the chart below. That’s a +40 percentage point edge driven by focused, thesis-backed positions in companies with strong management, sector tailwinds, and attractive valuations. It’s the compounding effect of being early in high-quality setups:

🚀 Coming soon on the Substack:

👉 In upcoming posts, I’ll cover:

A full deep dive on one of the Top 5 Swiss companies highlighted in this article (free). Done✅

How to optimize taxes when investing from Switzerland, a huge advantage vs US & EU (free).

Continued deep dives on asymmetric opportunities I’m tracking, including my recent Azeus deep dive (free).

The “move to Switzerland” playbook for investors and entrepreneurs (paid).

My personal Swiss allocation strategy, which has returned 50%+ in a year and 30%+ CAGR over the past 5 years (paid).

If you find the kind of knowledge packed into these deep dives valuable, not just theory, but returns that beat the market by over 40 percentage points, I’d genuinely appreciate a subscribe, like, or comment. This isn’t fluff. It’s a conviction-driven approach to finding real compounders with asymmetric upside. I’ll keep sharing deep dives on high-quality businesses, special situations, and tax-optimized investing. If that’s your playbook too, you know what to do 😉 ⬇️.

Now, let’s talk about Swissquote, and why the story is just getting started.

👉 What you’ll find in this deep dive on Swissquote ($SQN):

A founder-led fintech bank compounding profits at 25%+, with a fortress balance sheet and 52% margins.

A record-breaking 2024: Revenues +24%, Net Income +35%, Dividend up 40%, and crypto income up 4.5x.

Diversified income streams: interest, equities, crypto, FX, custody. Built to thrive in any market.

Not just Swiss. Global: Expanding across EU, Middle East, and Africa with profitable mobile banking JV (Yuh).

Product innovation engine: AI tools, fractional shares, savings plans, and the only bank-run crypto exchange in Switzerland.

Owner-operators at the helm: Founders still hold ~22%, compounding shareholder value for 25+ years.

Valuation? Fairly priced (~20-22x P/E) for a high-ROE, capital-light compounder still underfollowed by global investors.

Risks? Manageable: Rate sensitivity, fintech competition, but Swissquote keeps executing.

Long-term outlook: Clear 2028 profit target (+45%), zero net debt, and a playbook that keeps beating expectations.

If you’re hunting for real compounders, backed by smart capital allocation and Swiss discipline, this is one of Europe’s best-kept secrets.

Swissquote Group (SWX: SQN) is no overnight fintech. Founded in 1996 by engineers Marc Bürki and Paolo Buzzi, it started as a humble project to publish real-time stock quotes online, hence the name.

From the picture alone, you'd guess it right, right? They have to be Swiss bankers:

From a two-man operation in a Gland warehouse, it has grown into Switzerland’s leading digital bank, blending Swiss reliability with fintech agility. Over nearly three decades, Bürki and Buzzi have transformed Swissquote into a publicly listed, highly profitable, and tech-forward financial institution (in the Swiss Stock Exchange (SIX) since May 29, 2000). Today, it stands at a strategic inflection point: after a record-breaking 2024, the stock has rallied over +50% in the past year, yet still trades at a modest ~22x earnings, a reasonable multiple for a founder-led compounder growing EPS at 30%+.

While investors have taken a breather following management’s conservative 2025 guidance (Swiss are conservative by nature), the stock’s recent ~13% pullback could be more of an opportunity than a warning.

Sentiment: Fairly priced ⚖️ Swissquote isn’t cheap, but it’s not expensive for what you’re getting either. At ~22x trailing earnings and ~21x forward P/E, the stock trades at a premium to traditional banks but fairly relative to its fintech peers, especially when you factor in its profitability, diversification, and growth profile. This is a capital-light, founder-led business compounding EPS at 30%+ over last 5 years with a 52% operating margin and a fortress balance sheet. You’re paying a reasonable multiple for quality, scalability, and alignment, in a Swiss conservative market. And here’s the kicker: European equities still trade at just ~14x forward earnings, slightly above its average and well below their 25-year range. The market continues to underprice European tech excellence.

Record-Breaking 2024 Financial Performance 🚀

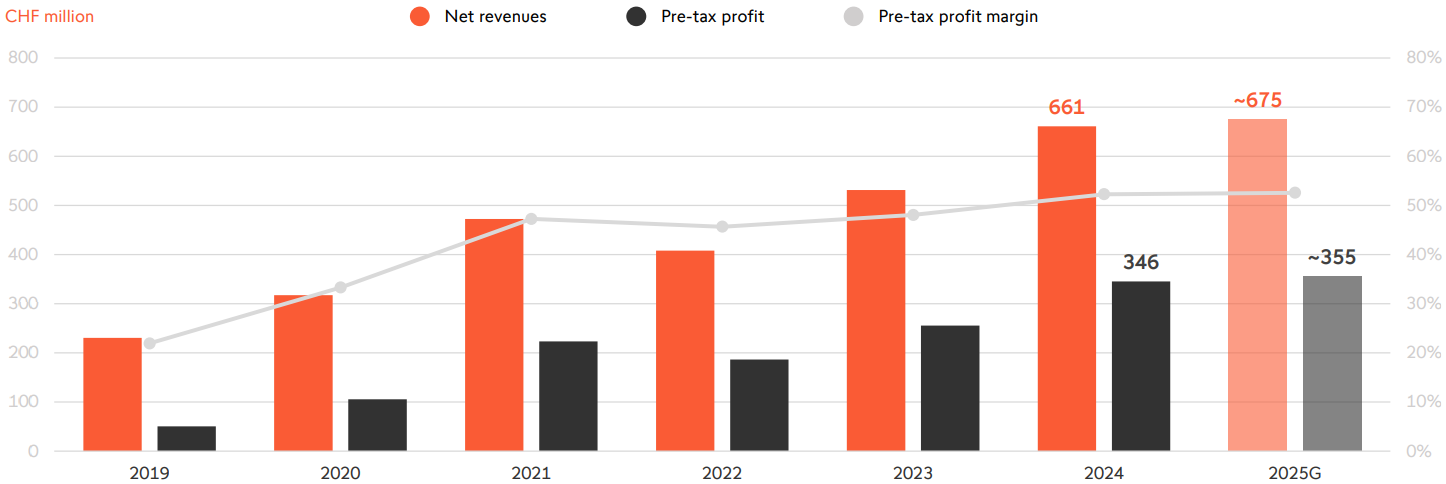

Swissquote delivered its best year ever in 2024, setting new records on multiple fronts. Despite a mixed market backdrop (rising rates early on, then waning volatility), the company’s top and bottom lines surged to all-time highs. Revenue jumped 25% to CHF 661 million, while operating profit climbed 35% to CHF 345.6 million.

Net profit followed suit, rising to CHF 294.2 million (+35% YoY).

Impressively, Swissquote’s operating profit margin hit 52.0%, its highest ever, reflecting disciplined cost control even as revenues expanded. In short, 2024 was a banner year, affirming the resilience of Swissquote’s model.

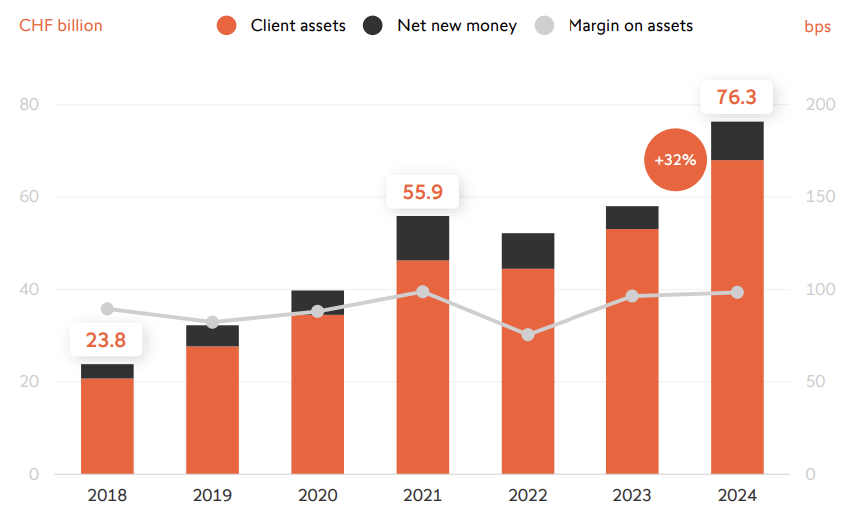

Such growth was fueled by strong client activity and asset inflows. The number of client accounts swelled by 75,000+ in 2024 (up 13.2% YoY) to reach 650,089. Client assets leapt 31.5% to CHF 76.3 billion, a remarkable jump aided by CHF 8.3 billion of net new money (versus CHF 5.0 billion in 2023) and favorable market performance.

Notably, all regions saw positive inflows, with Swissquote attracting CHF 5.1 billion in Switzerland and CHF 2.2 billion in the EU organically. This robust asset growth underscores Swissquote’s appeal to self-directed investors, even in choppy markets.

These asset inflows are the raw material Swissquote earns fees on, whether via interest, trading commissions, or custody.

Crucially, revenue growth +24% was broad-based. Swissquote’s fee and commission income (from trading, excluding crypto) climbed ~25% to CHF 178.2 million in 2024, driven by high client trading activity (particularly in foreign equities). Crypto-related income skyrocketed +353% to CHF 85.5 million, contributing 13% of total revenues as crypto markets rebounded late in the year. Even net interest income, which had exploded in 2023 due to rate hikes, managed to grow a further 5% in 2024, benefiting from a 33% jump in client cash deposits and a favorable USD/EUR mix on deposits. The only soft spot was eForex (online FX trading), which dipped 6% to CHF 94.7 million amid low FX volatility.

Overall, Swissquote’s diversified revenue streams cushioned any single segment weakness. As CEO Marc Bürki summed up:

“even in a challenging market, we achieved record income and profitability, a testament to the resilience of our business model”.

Swissquote’s operating expenses rose 16.5% (mainly from strategic hiring and higher performance-based pay), but grew much slower than revenues (+24%). In fact, the company’s cost/income efficiency improved, enabling the fat profit margin noted above. It’s clear management is investing for growth without sacrificing profitability.

For shareholders, Swissquote’s board has proposed a CHF 6.00 dividend per share for 2024, up sharply from CHF 4.30 the prior year, representing ~30% payout of net profit. The company’s capital ratio remains a solid 23.5% even after accounting for this payout. In short, 2024’s results showcased Swissquote’s ability to thrive in varying market conditions, leveraging both rising interest income and client trading activity for long-term gains.

Growth Drivers: Tech, Crypto & More 💡

Swissquote’s stellar 2024 was no accident, it’s the payoff of forward-looking investments in technology and product innovation. A prime example is the company’s bet on crypto. Years ago, Swissquote became the first (and still only) bank in Switzerland to operate a full-fledged crypto exchange. In 2024, that crypto exchange really proved its worth: heightened crypto volatility (especially after the U.S. elections) drove a surge in trading, and Swissquote’s exchange, backed by Swiss banking security, captured the volume. The result was a massive boost in crypto revenues (up 4.5x). It’s an almost ironic twist: a staid Swiss bank embracing crypto, yet it gave Swissquote a clear edge when crypto markets rebounded. As Marc Bürki noted,

“being the only bank-run crypto exchange meant we could effectively serve clients during the late-2024 crypto frenzy. Swissquote’s early move into digital assets back in 2017 now looks prescient”,

validating its tech-pioneering ethos.

Another innovation highlight was artificial intelligence tools. In 2024 Swissquote introduced an AI-powered sentiment analysis feature on its trading platform. This tool uses advanced language models (akin to GPT transformers) to sift through news and social media, gauging market sentiment on stocks. It condenses huge volumes of news into simple positive/negative/neutral signals, helping investors cut through noise. In true Swiss fashion, the AI is deployed responsibly, it analyzes public data only (no client data?) and is monitored for fairness. While it won’t guarantee winning trades (no AI crystal ball here), it arms Swissquote’s clients with insightful data in an easy format, aligning with the company’s mission to “democratise finance” through technology.

This kind of practical innovation, think less hype, more useful tool, bolsters Swissquote’s appeal to tech-savvy investors. (And yes, even Swiss bankers are dabbling in ChatGPT-like tech, just without the sci-fi fanfare).

Swissquote introduced fractional share trading in 2024, making high-priced stocks like Amazon accessible to investors with smaller budgets. It’s a welcome move that lowers the entry barrier to global investing. Alongside this, the launch of the Swissquote Savings Plan, (a robo-like tool for automated, recurring investments), signals a push beyond pure trading into broader wealth management for the “mass affluent” segment. These additions help increase stickiness by encouraging clients to build long-term positions rather than simply trade in and out.

In terms of market reach, Swissquote currently offers access to around 60 global exchanges, respectable for a European fintech, but still limited compared to the 150+ markets available on Interactive Brokers, which remains the gold standard for global investors. That said, Swissquote brings something most traditional brokers don’t: a native, regulated crypto exchange operated fully within the bank, offering secure and direct access to major cryptocurrencies. While it’s still building out its international footprint, Swissquote is carving a distinct position by blending traditional finance with forward-looking features, and it’s steadily narrowing the gap.

On the strategic expansion front, Swissquote didn’t sit still either. It made a targeted acquisition in early 2024, buying Optimatrade in South Africa (now rebranded Swissquote South Africa) to gain a foothold on the African continent. This follows its 2022 acquisition of Keytrade Bank Luxembourg, which was successfully merged into Swissquote Europe to broaden its EU presence. These moves show Swissquote executing on a global expansion strategy, extending beyond its Swiss home base to tap new client pools. The Optimatrade deal, while modest (CHF ~4.3 m purchase), brought in CHF 1.3 billion of client assets and an introducing broker network in a new market. Meanwhile, Yuh, Swissquote’s mobile banking joint venture with PostFinance, was another success story in 2024: the app’s user accounts jumped 48% to 285,000 and client assets doubled to CHF 2.8 billion.

Notably, Yuh reached profitability ahead of plan during 2024. This is significant, Yuh is aimed at young, mobile-first customers in Switzerland, a demographic key to Swissquote’s future. Now profitable, Yuh is no longer a drag on earnings but a contributor, validating the JV approach. All these innovations and expansions, crypto, AI tools, fractional shares, savings plans, new markets, illustrate Swissquote’s “pioneering DNA” that management frequently touts. Crucially, they were achieved without bloating costs: Swissquote still kept marketing and IT spend efficient (even upping marketing by 18% to ride the growth momentum).

In the words of Chairman Markus Dennler,

“Swissquote stands out through a unique combo of Swiss reliability, cutting-edge tech, and a culture of innovation”,

which in practice means constantly adding new services while keeping that trusted Swiss bank aura.

Subtly, Swissquote is transforming from a pure online broker into a full-service digital bank. Marc Bürki emphasizes a “one-stop-shop” vision, offering not just trading, but payments, lending, robo-advice, etc., all with a tech edge. The 2024 initiatives reflect this: they’re laying groundwork for Swissquote to capture more of a client’s financial life (saving, investing, spending) within its ecosystem.

Market Position and Revenue Diversification 🌐

Swissquote today occupies a unique market position at the intersection of banking and brokerage. It’s often dubbed “the Swiss Robinhood” for its online trading focus, but unlike Robinhood, Swissquote charges commissions, is a multi-asset access and also runs a bank, yielding far more diversified revenue. In fact, Swissquote’s revenue mix is more akin to a mini-Charles Schwab or Interactive Brokers, straddling interest income, trading commissions, and asset-based fees. This balance became very evident in 2024: when trading revenues dipped in early 2023, interest income (thanks to higher rates) carried the load; when interest margins tightened in late 2024, trading and crypto revved up, a natural hedge. Management deliberately cultivated this diversification.

Swissquote’s “multi-asset, multi-stream” model means it can earn from client cash balances, stock trades, FX, CFDs, crypto, and more. As a result, the company is less vulnerable to any one market’s downturn. In 2024, for example, non-transaction revenues (interest, custody, etc.) exceeded transaction-based revenues for the first time, a sign that Swissquote has reached a new level of balance in its business.

Geographically, Swissquote remains rooted in Switzerland (where it’s the top online bank), but is expanding across Europe and even into Asia/Middle East. Swiss clients still contributed ~80%+ of operating income in 2024, but European clients are growing fast (EU operating income +35% in 2024) and now make up ~7% of revenue. The company opened a new Madrid office and integrated Keytrade Luxembourg, signaling intent to become a truly pan-European fintech. Its brand stands for Swiss quality and security, a strong selling point abroad, especially after some high-profile fintech failures (e.g. Wirecard, FTX, BlockFI, etc.).

Swissquote can credibly claim to offer the safety of a Swiss bank with the innovation mindset of Silicon Valley, a rare combination that appeals to investors seeking both trust and tech. Competitively, it faces online brokers across various markets (e.g. DEGIRO, Interactive Brokers, TD Ameritrade, Schwab, Robinhood), but few provide the same breadth of services under one roof: from regulated crypto trading to full-suite Swiss banking. This integrated model has enabled Swissquote to build a highly diversified and resilient revenue base.

Net Interest Income (~33% of 2024 revenue): Swissquote smartly capitalized on higher rates by sweeping client cash into short-term investments. In 2024, interest income was CHF 224 m (up from CHF 213 m), comprising a stable one-third of revenues. Unlike pure brokers, Swissquote operates as a bank, so it can earn a spread on deposits (while still offering competitive rates to clients). This provides a steady income baseline even if trading slows. One risk: as interest rates normalize downward (as they started to in late 2024), this tailwind could fade. However, Swissquote managed to grow interest income slightly even in a “declining rate environment” by increasing deposit volumes and optimizing currency, showcasing management’s treasury skills.

Trading Fees & Commissions (~40% incl. crypto): Traditional trading fees (stocks, funds, etc.) were CHF 178 m in 2024, about 27% of revenue, while crypto trading fees added another CHF 85.5 m (~13%). Combined, commission-type income made up ~40% of revenue. This is transactional and tied to client activity, which can fluctuate with market conditions. 2024 saw a resurgence in equity trading interest (foreign equities were especially popular), benefiting Swissquote’s commissions. Meanwhile, the crypto fee explosion shows Swissquote can ride new waves when they come. Few competitors in Europe offer direct crypto trading within a banking platform, Swissquote’s willingness to venture here gave it a unique market share in crypto trading when the boom returned. This part of the business is higher risk/reward (volatile volumes, regulatory uncertainty in crypto), but Swissquote has so far managed it prudently (only listing major cryptos, stringent risk controls).

eForex and Other Trading (~20%): Leveraged forex trading contributed ~CHF 95 m in 2024 (14% of revenue). This segment has been subdued by ultra-low FX volatility (2024 was a snoozer in FX markets). Yet, Swissquote’s eForex still generates healthy income via spreads on client trades. It’s basically market-making revenue: Swissquote adds a small markup on forex quotes. When volatility returns, this segment could uptick. “Other trading” (like market-making in other assets, or trading gains) made up the remainder (~12%). Notably, Swissquote takes very limited principal risk, it largely uses an agency model (no big prop trading bets). That aligns with its conservative Swiss banking DNA and keeps earnings quality high (less earnings from one-off trading windfalls, more from stable client-driven flows).

Overall, Swissquote’s revenue diversity is a strength few fintech peers can match. US brokerage giants like Schwab or Interactive Brokers also boast multi-stream income (Schwab gets ~50% of revenue from net interest, IBKR similarly from interest + financing). In Europe, competitors are narrower: e.g. flatexDEGIRO (DE) relies mostly on brokerage fees (and struggled when trades slowed in 2022), Saxo Bank and IG Group make a lot from FX/CFD trading but less from interest. Swissquote sits in an enviable middle ground, diversified like a bank, nimble like a fintech. Its Swiss banking license and regulatory status give it a trust advantage over unregulated platforms, while its tech offerings beat those of lumbering traditional banks. As one measure of market positioning, Swissquote’s client asset base (CHF 76 bn) now rivals mid-sized private banks, yet its average account size (~CHF 117k) implies a mass-affluent clientele, not just ultra-high-net-worth. This bodes well for stability, a broad base of ~650k clients means no single whale can rock the ship. The firm’s long-term strategy to be “the first bank for digital-first mass affluent investors” is clearly on track.

Swissquote’s total client assets have grown dramatically, from CHF 40 billion in 2020 to CHF 76 billion in 2024. Even during the 2022 market dip (when assets fell), Swissquote rebounded strongly. This asset growth, fueled by net new money inflows each year, underpins future revenue potential (more assets to earn interest and fees on). The 2024 jump reflects both strong inflows and positive market performance.

Despite Swissquote’s successes, inefficiencies are few but worth watching. One might question the cost of continually adding new features, e.g. AI tools, new platforms, could complexity hurt margins? So far, Swissquote’s lean ~52% cost/income ratio says otherwise. The company smartly centralizes costs and doesn’t allocate redundant expenses to each segment. It’s a mindset of efficiency, Swissquote’s management seems equally averse to bloat: even marketing spend (a discretionary cost) is carefully tuned to market conditions. Furthermore, Swissquote avoids the payment-for-order-flow (PFOF) model that some US brokers use to monetize trades, a practice often criticized as conflict-prone. Instead, Swissquote earns more transparently via commissions and spreads, which keeps it on the right side of European regulations and likely results in better execution for clients (sparing them the hidden “PFOF tax”). This client-centric ethos likely contributed to Swissquote achieving a high customer satisfaction (Net Promoter Score NPS of 39 in 2024, a record). Happy customers stick around and bring more assets, a virtuous cycle that reinforces Swissquote’s long-term positioning.

Management Quality & Ownership 🧠💼

One of Swissquote’s greatest assets is the quality and alignment of its leadership. The company is a rare owner-operated success story in banking, CEO Marc Bürki and CTO Paolo Buzzi co-founded Swissquote nearly three decades ago and continue to helm its evolution today. Under their steady leadership, Swissquote grew from a two-man startup (providing online stock quotes out of a warehouse in 1996) into Switzerland’s undisputed leader in online trading, all while navigating multiple market crises. This kind of long-term execution track record is exceedingly rare in finance. Bürki and Buzzi steered Swissquote through the dot-com bust (when the stock collapsed from CHF 250 at the IPO to CHF 11 in the early 2000s) and the 2008 financial crisis, emerging each time with a stronger, more innovative company. They are engineers by training, not traditional bankers, and it shows in Swissquote’s DNA. Buzzi famously quips,

“I’m an engineer that became a banker by accident”

emphasizing the company’s tech-first culture. In his words,

“We are a tech company with a banking license”

a striking statement that highlights Swissquote’s ethos of innovation. Indeed, Swissquote has led its peers in adopting new technologies (from being the first Swiss bank with an iPhone app in 2008 to being Europe’s first bank to offer crypto trading in 2017, years before larger banks dared to). This pioneering spirit comes straight from the top: Bürki and Buzzi’s focus on software development, creativity, and customer empowerment is woven into Swissquote’s strategy.

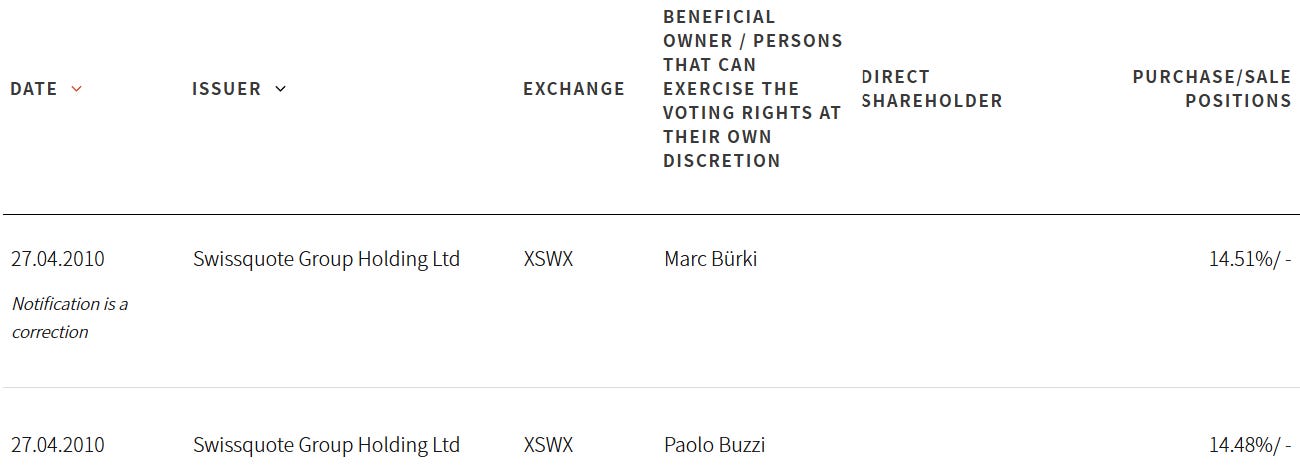

Crucially, management’s interests are deeply aligned with shareholders. Marc Bürki (CEO) is Swissquote’s largest shareholder at ~11.5% ownership, and Paolo Buzzi holds around 10.4%.

Together they own ~22% of the company, a stake worth roughly CHF 1.4 billion, and have deliberately remained major shareholders even as Swissquote’s market cap swelled above CHF 6 billion. This long-term ownership mindset means management thinks like owners, prioritizing sustainable growth and shareholder value over short-term gambits. Notably, the founders have gradually reduced their stakes from higher levels in the early days to ~22% today (see the image below), but those sales have been orderly and often to strategic partners (for instance, the Swiss post office’s banking arm, PostFinance, acquired a 5% stake in Swissquote as part of a strategic collaboration).

Even after 25 years, Bürki and Buzzi clearly believe in Swissquote’s future, they remain fully engaged, with no signs of complacency despite their substantial personal stakes in the company. In 2024, the total fair value of stock options granted to Executive Management was just CHF 777,000, a modest figure that underscores how little dilution is needed when leadership already thinks like owners.

The rest of the Board and Executive team together hold 128,579 shares, signaling some alignment, though most of the weight is clearly with the founders.

On the other hand, Swissquote doesn’t play the dilution game either. Shares outstanding have remained flat at around ~15 million for over a decade, and stock-based compensation is minimal.

Valuation and Peer Comparisons 📈

Swissquote’s stellar performance hasn’t gone unnoticed by the market. The stock nearly doubled in 2024, ending the year at CHF 348 (up ~70% from CHF 204 at 2023’s end). Over a five-year span, SQN has been a multi-bagger, climbing from ~CHF 86 at end-2020 to CHF ~430 now.

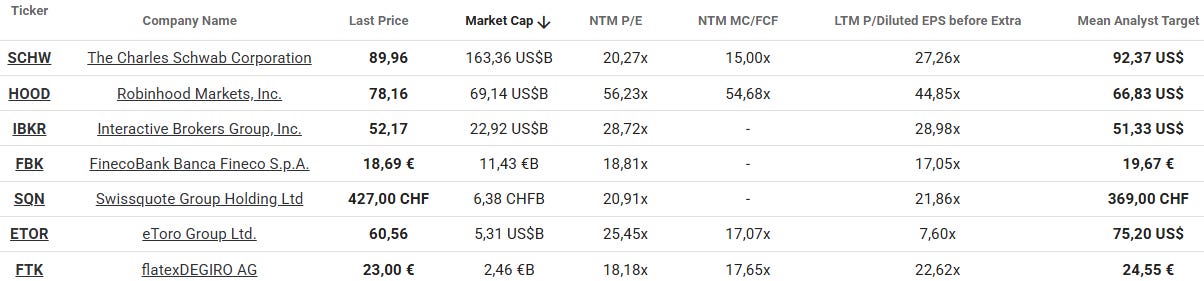

With a +433% return over last 5 years, it has outpaced global peers like IBKR (+398%), Schwab (+145%), and Robinhood (+121%), firmly leading the digital broker pack.

This share price surge reflects investors’ recognition of Swissquote’s earnings growth and improved prospects. Indeed, as management pointed out, better earnings visibility and a stronger equity base have led to a “progressive re-rating” of the stock. Swissquote trades at valuation multiples that price in its growth: currently about 21x NTM earnings.

For context, that is a premium to many European banks (sector average P/E ~10-12x), but more in line with fintech peers. For example, Interactive Brokers trades ~29x NTM earnings and flatexDEGIRO around 18x. As shown in the chart, Swissquote’s ~21x forward P/E sits comfortably between conservative brokers like FTK and premium-growth names like IBKR or Robinhood (which trades at a rich 56x). Charles Schwab, trades around 20x forward earnings after its recent turbulence, FinecoBank in Italy (another online investing bank) trades ~19x, quite comparable to Swissquote given similar hybrid models. One notable metric: Swissquote’s price-to-book is ~6.2x, which is high vs peers (who average 1-3x depending on model). This reflects Swissquote’s high return on equity and light balance sheet (few physical assets). It does mean the stock isn’t “cheap” on book value, but for a capital-light fintech, P/B is less meaningful (a lot of Swissquote’s value comes from intangible assets like its platform and customer base).

Analysts have tempered 2025 estimates a bit (management issued a cautious outlook, noting 2024 benefited from unusually favorable conditions). Indeed, when Swissquote gave initial 2025 guidance, the stock dipped ~7% as some exuberant expectations were reined.

This perhaps healthy skepticism has kept Swissquote’s valuation from overheating.

Swissquote’s risk profile is arguably lower than many fintechs: it’s profitable, well-capitalized, and prudently run. That justifies some premium. Additionally, Swissquote’s dividend yield (CHF 6 on a CHF 430 stock is ~1.4%) isn’t high, but the payout has room to grow given the 30% payout ratio. Management is retaining earnings to fund growth, a strategy shareholders will appreciate, because Swissquote has clear avenues to deploy capital at high returns (e.g. geographic expansion, tech development).

Let’s also consider share price performance vs fundamentals. Over 2020–2024, Swissquote’s EPS rose from CHF 6.12 to CHF 19.70, a ~3.2x increase, while the stock price rose ~4x. The slight multiple expansion shows increased market confidence. Swissquote’s shareholder base evolution underpins this confidence: Founders Marc Bürki (CEO) and Paolo Buzzi still own ~22% combined, providing strong insider alignment, but they have gradually sold down from higher levels years ago, improving the free float. Free float is ~73% now and includes institutional investors like UBS Fund Management (5.1% stake). Notably, PostFinance (the Swiss postal bank) owns 5.0% as a strategic partner (tied to the Yuh JV). This stable of shareholders (founders + Swiss institutions) gives a supportive base, while the broad free float ensures liquidity. Over recent years, insider ownership has stabilized around ~22%, high enough for commitment, but low enough to avoid entrenchment. There have been no alarming insider sales lately; the tiny decreases in founder percentages from 2022 to 2024 were marginal. In fact, the CEO has publicly set bold targets (aiming for CHF 500 m operating profit by 2028), indicating he’s focused on growing the pie, not cashing out. It’s refreshing to see a fintech where management thinks in 5-year plans, not quarterly trading hype.

In summary, Swissquote’s valuation is demanding but not irrational. The company trades at roughly a market multiple for a growth stock of its caliber. Investors are effectively betting that Swissquote will continue to compound earnings at a double-digit pace, leveraging its tech and market position. If it can execute (grow assets, expand internationally, monetize new services) as it has, today’s multiple will look quite fair in hindsight. However, any stumble, e.g. a sudden drop in trading volumes or margins, could compress the multiple. This was seen in early 2022 when the stock fell on weaker activity, taking the P/E down. Thus, Swissquote must keep proving itself to justify its fintech valuation. Given management’s track record so far, there’s reason to be optimistic.

Long-Term Outlook and Risks 🔮

Looking ahead, Swissquote’s management is targeting CHF 500 million operating profit by 2028, roughly a 41% increase from 2025 estimate, the implied CAGR over that period is approximately 13%. Achieving this will require mid-teens annual profit growth. Key drivers will be continued client growth, deeper monetization of existing clients, and international expansion. On client growth: Swissquote added ~75k accounts in 2024; it may need a similar or higher annual pace (which could come from new markets like Spain or Germany, and from Yuh’s ongoing growth). However, to accomplish this strategy they forecast 50k added accounts on yearly basis with a 55% pre-tax profit margin assumed.

There is significant runway: even at 650k accounts, Swissquote has only ~5% of Switzerland’s population and a tiny fraction in EU markets. If Swissquote replicates its Swiss success abroad (even modestly), account numbers could swell. Each new client often brings an initial deposit and then grows their assets over time. Swissquote’s high customer satisfaction and expanding product suite suggest it can retain and deepen relationships, increasing assets per client. The average client asset of ~CHF 117k is already quite high, but includes some wealthy individuals; as Swissquote attracts more mass-market customers via Yuh and similar, average may dip even as total assets climb. The company’s challenge will be converting those entry-level clients (with small balances) into full-service users of Swissquote as they accumulate wealth.

A potential headwind is the interest rate cycle. 2023-24 gave a huge boost to net interest income as global rates surged from zero. But Switzerland has now reentered the zero-rate era: SARON is flat at 0%, and swap markets forecast it staying near that level through at least 2026. According to the SNB’s projections, even the 10-year swap rate barely reaches 0.7% by mid-2027. This means Swissquote’s interest margins could compress further. Indeed, Q1 2025 guidance was already cautious on this front, and the stock briefly dipped. That said, Swissquote isn’t defenseless. Even in a low-rate world, volumes matter: more client assets = more fee income (custody, FX conversion, etc.). And with 0% rates, trading often heats up, offering a natural offset through higher transaction revenue. Swissquote has weathered interest cycles before, and its diversified model is designed to keep compounding even as rates retreat.

Still, it’s something to watch closely on the upcoming H1 2025 call, scheduled for August 14th.

Regulatory changes are another risk to watch. Being a bank and broker, Swissquote faces a lot of oversight, from FINMA in Switzerland to EU regulators through its subsidiaries. Any clampdown on crypto trading, for example, could impact that revenue stream (though Swissquote’s fully regulated approach makes it less exposed than unregulated crypto platforms). Likewise, regulations on CFD trading and leverage (ESMA’s rules, etc.) have tightened in recent years, Swissquote appears to comply fully, but if leverage caps further reduce client trading, eForex income might stagnate. On the flip side, higher regulations often drive clients to trusted platforms like Swissquote, benefiting them over shadier competitors and building a moat. Swissquote’s emphasis on transparency and compliance (it even had shareholders vote on its sustainability report) shows it wants to stay ahead of the curve in governance, which should mitigate regulatory surprises.

One area where Swissquote could face competitive pressure is pricing. Fintech disruptors often compete via lower fees. While Swissquote doesn’t charge an arm and a leg (its fees are moderate and it has free offerings like Yuh’s zero-commission stock slices), competition in Europe is heating up. For instance, US zero-commission broker Trade Republic is expanding in the EU, and Revolut offers commission-free trades as a hook. Swissquote may need to adjust pricing or emphasize its superior service to justify costs. Thus far it has defended its turf by offering more products and a premium experience (and indeed, many investors seem willing to pay a bit for a reliable Swiss platform). But the fee compression trend in brokerage globally is something to monitor, Swissquote might see margins squeezed if it had to cut commissions dramatically. The saving grace is that Swissquote has alternate revenue sources (interest, FX spreads) that pure “free-trading” apps lack, so it can afford to be flexible on visible fees while still earning elsewhere.

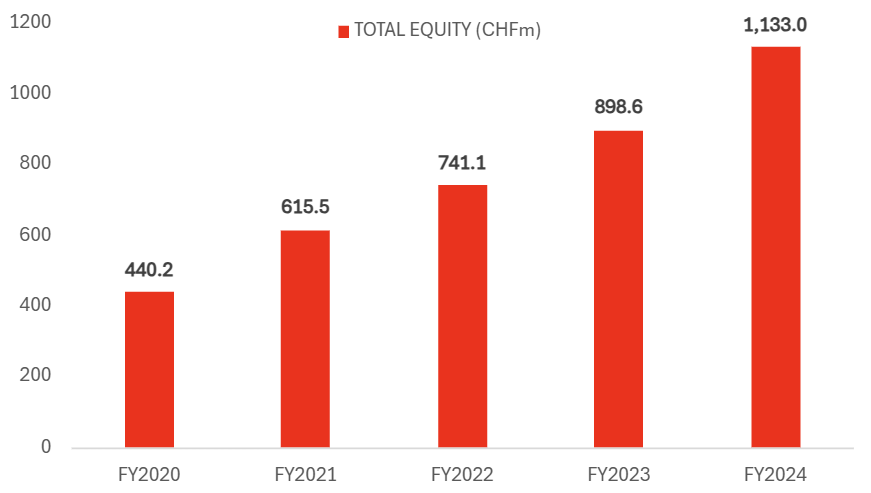

From a long-term investor’s lens, Swissquote’s story is compelling: a consistently profitable, founder-led fintech with a strong moat in technology and a growing international footprint. The company has virtually no debt, a fortress equity base of CHF 1.13 billion, and generates high returns on that equity (~25% ROE). Management also appears to be sensible capital allocators, balancing growth investments with shareholder returns (the dividend is growing and they opportunistically do share buybacks to neutralize option dilution, holding ~2.5% in treasury shares).

In the coming years, watch for Swissquote’s moves in new markets. The company has hinted at expanding further in Asia (it opened a Singapore office previously) and perhaps deeper in the Middle East where it already has a Dubai presence. Any accretive acquisitions (like Keytrade) or partnerships could accelerate growth. Swissquote also continues to innovate in-house, a “digital wealth coach” AI tool is mooted as a next step, potentially moving into robo-advisory more seriously. These could unlock new revenue lines (e.g. advisory fees). The management’s demonstrated skepticism of inefficiency means they likely won’t over-hire or overspend to do this; expect disciplined R&D that targets specific client needs (like the 2024 launches that were very much client-requested).

Market volatility will, of course, create year-to-year swings in Swissquote’s growth. But an investor with a long view can appreciate that each market downturn often benefits Swissquote in the end: volatility sparks trading (short-term revenue) and drives more people to take control of their investments, many of whom end up at Swissquote (long-term clients). For instance, 2022’s bear market slowed earnings, but Swissquote still added net new money and then reaped the rewards when 2024 markets recovered, hitting new highs in assets. This ability to weather the storm and come out stronger is a hallmark of a robust business model.

Conclusion 🎯

In conclusion, Swissquote stands out as a fintech success story blending innovation with profitability. The 2024 results crystallized the thesis: Swissquote can grow vigorously (revenues +25%, profits +35%) while staying lean and adaptive. It’s hard not to be impressed by a 27-year-old online broker from Gland, Switzerland evolving into a global digital bank with CHF 76 billion in client assets. The company’s strategic choices, embracing crypto early, investing in AI tools, expanding internationally, and diversifying income, are paying off in spades. There’s a certain Swiss prudence in how Swissquote is run (strong capital ratios, cautious guidance, high transparency), yet also a boldness in vision (aiming to “constantly outperform legacy banks” through tech). This combination bodes well for delivering long-term returns to shareholders.

At ~21x forward earnings, Swissquote’s stock isn’t a cheap bargain, but you often get what you pay for: a debt-free, high-margin business growing its moat. Compared to less efficient incumbents and less profitable fintech upstarts, Swissquote hits a sweet spot. It has the optionality of a fintech (new products, new markets can unlock growth) with the stability of a bank (recurring income, loyal clients). Risks like market swings and fee pressure are real, but manageable given Swissquote’s adaptability. For investors, Swissquote offers exposure to secular trends (digitization of banking, rise of self-directed investing, crypto adoption) through a profitable vehicle that has proven it can execute. Crucially, it also benefits from a naturally counter-cyclical trait: when interest rates fall, trading volumes tend to rise, a human impulse Swissquote is well-positioned to monetize. That built-in hedge, combined with its flexibility and execution track record, gives Swissquote resilience across rate cycles.

In a world of flashy fintech IPOs that flame out, Swissquote is refreshingly substance over style. The stock’s journey may have its ups and downs, but the underlying trajectory is one of consistent innovation, growing assets, and expanding earnings power. In other words, the Swissquote story still has plenty of chapters to write, and it’s one that merits a close read for any long-term investor seeking fintech exposure with a solid safety net. Swissquote has dared to do things differently, and it’s working, to the benefit of both its customers and shareholders.

If you enjoyed this, a follow and a share go a long way to support my deep dives. I’ll continue sharing deep dives on $SQN and other asymmetric opportunities. I focus on compounding businesses, smart capital allocation, and tax-optimized investing, with a long-term lens. To stay updated, just subscribe below ⬇️.

Final Veredict & Excel Model (For Paid Subs) 📊

It could be the next potential addition to the Swiss Transparent Portfolio? The setup is getting too good to ignore. Founder-led, insanely profitable, and quietly

Keep reading with a 7-day free trial

Subscribe to Swiss Transparent Portfolio to keep reading this post and get 7 days of free access to the full post archives.