Where’s the Money in AI?

One of our Swiss Portfolio members recently shared with us a delightfully contrarian article titled “There Is No AI Revolution”, essentially a scathing take on generative AI hype, perfectly timed as everyone buzzes about GPT-5. (Ad: Become a member for less than a McPork!). The piece goes so hard against ChatGPT & Co. that I half-wondered if it was ghostwritten by one of OpenAI’s rival AI models (Gemini or xAI, perhaps?). We love hearing out smart contrarians. Their arguments either save us from a bubble or strengthen our conviction by forcing us to address the tough questions.

And the key question this article poses is: “Where’s the real money in AI?” 🤔

Before we answer that, let’s recap what the AI-skeptic is saying, and then see why we still think AI could be an Amazon-in-the-90s kind of opportunity.

The Contrarian Case: “No, Really, Where’s The Money?”

The skeptic’s arguments can be summarized as follows:

Hype vs Revenue Reality: Generative AI may be revolutionary in theory, but actual profits are scarce. The author notes that tech giants investing heavily in AI (Google, Amazon, Microsoft) are strangely quiet about how much revenue these AI services bring in, likely because it’s “pretty god damn small” so far. Companies boast about “growing demand for AI” and deals signed, but with little dollar detail. Revenue is not the same as profit, and in AI land, even revenue itself is elusive.

OpenAI’s Money Pit: The poster child of the AI boom, OpenAI, is burning cash. Its flagship consumer product (ChatGPT) has a paid tier, $20/mo for Plus or a hefty $200/mo for the Pro plan with extra features, yet even those subscriptions lose money because heavy users rack up huge cloud compute costs. New OpenAI features like the “Deep Research” analysis tool are very compute-intensive and costly, and they’ve been quickly copied by rivals (Perplexity.ai, xAI’s systems, etc.). In short, OpenAI spends a fortune to deliver fancy demos that aren’t (yet) profitable. The contrarian dryly calls OpenAI and Anthropic “not real companies, just venture-backed welfare cases” living on investors’ dime.

Commoditization & No Moat: The moment OpenAI launches something, a dozen competitors (or open-source projects) launch their own version. The commoditization of generative AI is rapid. If everyone has similar large language models, margins erode and winners are hard to pick (aside from perhaps the cloud providers selling the compute, more on that later). The article argues that no durable moat has emerged, there’s no proprietary tech or network effect yet that locks users in, aside from maybe scale of data/compute (which just makes the burn bigger).

“Where’s the killer app?”: The skeptic questions the use-case for which people will pay big money. Yes, ChatGPT can write poems and code, but can it do something so indispensable that businesses or consumers will open their wallets at scale? Thus far, generative AI is “cool” but often unreliable, sometimes wrong, and arguably making humans lazier without truly “augmenting” us. The article bluntly claims “generative AI, at best, can be kind of cool yet mostly sucks” and that we’re reaching the limit of current LLM tech, further improvements are costing exponentially more compute without yielding fundamentally new capabilities. In other words, diminishing returns are setting in, with no clear killer app to justify the hundreds of billions being spent.

Bubble Fears: If you detect dot-com bubble vibes, you’re not alone. The contrarian frames this as a classic hype bubble: a “runaway narrative” sustained by press and FOMO, not actual user adoption or profits. User numbers for many AI apps are already plateauing, and the author argues “the revenue isn’t there”. He warns that the party ends when the market or Big Tech “accept they’ve chased their tails toward oblivion” on AI, and the whole scheme collapses. The most dire take:

“There is no industry here. There is no money… no proof this will ever turn into a real industry, and plenty of proof it will cost more money than it ever makes”.

Ouch! In this view, generative AI is a dead-end money pit, a bubble that could “implode” and take a chunk of tech valuations with it.

That’s the bearish case in a nutshell, and it’s not all crazy. Frankly, the piece makes some fair points. Many AI startups are valued to more than perfection (we’ll talk about those in a moment). OpenAI itself is reportedly on track to lose ~$9 billion this year while training/launching GPT-5, with no clear path to break-even. And there is a lot of over-exuberance, every company slapped “AI” on their pitch in 2023-24 to ride the wave, often with flimsy products. As investors, we should absolutely question the hype.

But does that mean AI is a nothingburger, destined to fizzle out? 🧐 Let’s take the other side. Why AI could actually make money?.

Big news at Swiss Portfolio

Enjoying these earnings reviews?

💥 Full access is just $39.99/year, more value and transparency than most $300+ memberships out there.

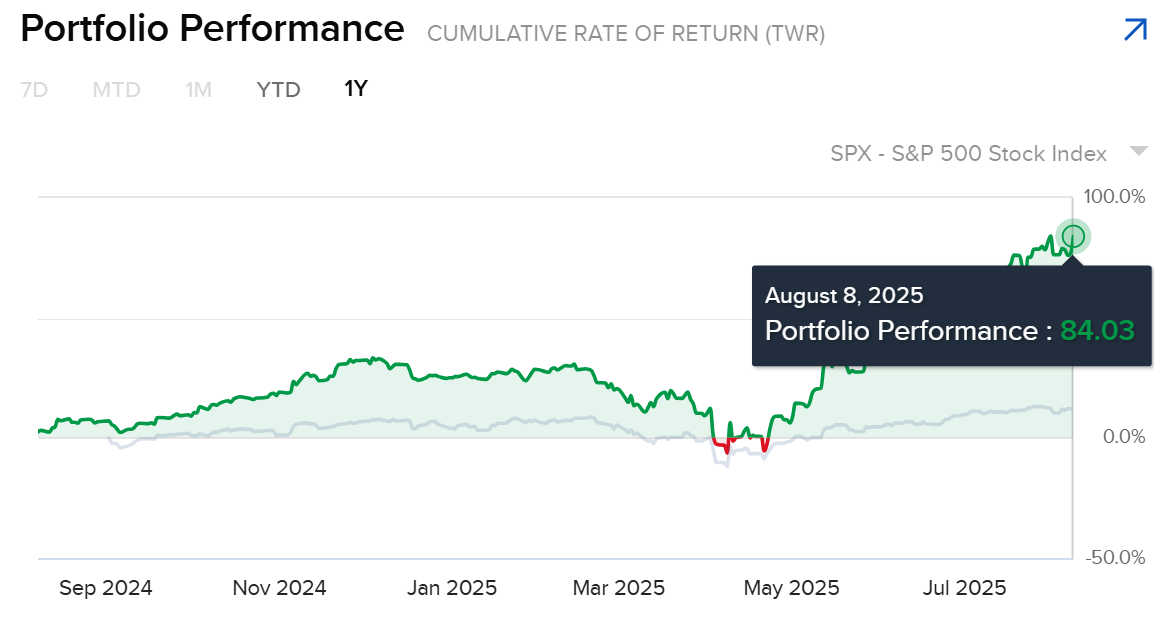

Over the past 12 months, our portfolio has returned close to 7x the S&P 500, and we publish every move with full transparency. In a world where most of finance hides behind paywalls and vague claims, we do things Swiss-transparently.

That’s not by chance. It’s the result of deep research, disciplined capital allocation, and a focus on durable, capital-light compounders, with strong management, sector tailwinds, and attractive valuations, often well before they’re widely recognized.

Become a member and you’ll gain full access to:

✅ Full access to Swiss Portfolio positions + monthly allocation updates.

✅ At least 1 high-conviction deep dive every month.

✅ Downloadable financial models to follow and stress-test each thesis.

✅ Live idea tracking once they spike, plus an S&P tracking template.

✅ Exclusive Swiss-based insights on investing, residence, and tax optimization.

🧠 The $39.99 subscription pays for itself a few times over, sometimes in just one deep dive. This isn’t about hype. It’s about transparency, consistency, and long-term compounding.

If you share our philosophy of identifying scalable compounders in high-quality jurisdictions backed by durable megatrends, we strongly encourage you to explore how past ideas have performed (current date 8.8 before market open) :👇

HIMS +97% since deep dive (13.1)

IESC +46% since deep dive (9.2)

PSIX +182% since deep dive (5.3)

SPGI +15% since deep dive (14.3)

WST +15% since deep dive (22.5)

SGX: BBW -3% since deep dive (9.6)

SWX: SQN +27% since deep dive (26.6)

The Other Side: Why AI Could Actually Make Money

History tells us that transformative tech often monetizes in indirect ways and on a time lag. The internet boom of the late ’90s had its Pets.com busts, but it also gave birth to Amazon and Google, companies that figured out the business model later and now print cash. We see a similar dynamic with AI. Here’s why we’re not writing off generative AI just yet:

The Cloud’s Hidden Goldmine: Generative AI might not be a big revenue line today for Google or Amazon, but it’s driving enormous demand for cloud computing. Training and running AI models is absurdly resource-intensive, and guess who sells those resources? The hyperscalers (Amazon AWS, Microsoft Azure, Google Cloud). For example, Nvidia’s data-center GPU sales have exploded thanks to “insatiable” orders from cloud providers building AI supercomputers. Nvidia literally recorded more revenue in a single quarter than in all of last year, largely due to the AI boom. That is real money, just not in a consumer-facing app, but in the ones supplying the boom. Every ChatGPT query might cost fractions of a cent in cloud compute, but scale that to billions of queries and someone is paying AWS or Azure a hefty bill. So even if OpenAI isn’t profitable, AWS (Amazon) and Azure (Microsoft) are profiting by renting out the GPUs. And guess who’s behind ChatGPT? Yes, the once-hated, now-behind-the-scenes Microsoft. The article’s author frets that hyperscalers are dragging along “half a trillion in capital expenditure” for AI, true, but those are investments to build capacity they intend to monetize for years to come. Today it looks like higher capex; tomorrow it’ll be usage-based revenue.

Free Users → Paid Subscribers: The contrarian asks “Where are the users?”, yet ChatGPT reached 100 million users faster than any app in history. True, most are free users, but this is a classic land-grab strategy. Big Tech knows how to convert free traction into paid services. OpenAI’s own plan (according to Sam Altman) is to offer richer features on paid tiers and eventually charge higher prices for more “intelligence” or usage. We see this already: many ChatGPT users have upgraded to the $20/month Plus for faster responses and plugins. Microsoft, for its part, is directly monetizing AI: it rolled out Copilot (an AI assistant) across Microsoft 365 and promptly put a $30/user per month price tag on it for enterprises. That’s essentially an AI upsell on top of Office, and companies are paying for it because it adds value in workflows. Google is doing similar with its Workspace (offering AI writing assistance in Gmail/Docs for a premium) and with Google Cloud’s AI services. The point is, the hyperscalers are experts at the freemium-to-subscription funnel. Generative AI features are quickly moving behind paywalls or into higher tiers. Yes, the initial period was a free frenzy (funded by VC $$$), but that’s shifting. Don’t be surprised when a year or two from now a significant chunk of heavy AI users are paying, either directly or as part of a cloud or SaaS package. In other words, the mass user base that skeptics dismiss as “not monetized” can be monetized with a flip of a switch (or rather, a tweak of a pricing plan). Also consider major partnerships, such as the announced plan to give every Dubai resident free ChatGPT Plus, a rollout that appears to be just around the corner.

Efficiency = $$ in Disguise: Not all ROI from AI will show up as “AI revenue”. A lot of it will come via cost savings and productivity gains, which bolster the bottom line. Take Duolingo as an example. This scrappy ed-tech company embraced generative AI to automate content creation. The result? They just launched 148 new language courses in under a year, basically doubling their total courses. For context, Duolingo’s first 100 courses took 12 years to build by human effort! AI dramatically accelerated their content pipeline. More courses = more learners = more potential subscription revenue for Duolingo, achieved with relatively minimal increase in headcount. That’s a direct efficiency win. Similarly, software developers using GitHub’s AI assistant are completing tasks faster; customer support teams using AI chatbots handle more inquiries with fewer agents, etc. These improvements reduce costs or increase capacity, which translates to better margins over time. You won’t see a line item on the income statement labeled “AI profit”, but it’s embedded in companies running leaner or selling more thanks to AI. As investors, we love to see that kind of quiet margin expansion.New Capabilities & Services: AI is also enabling new products and revenue streams that simply weren’t possible (or economical) before. For instance, Amazon is rolling out generative AI to enhance its e-commerce: from personalized product recommendations and search results (tailored to your browsing history) to AI-generated ad creatives that help sellers market better.

This has a flywheel effect, customers find what they want faster, buy more, and advertisers get higher ROI on Amazon’s platform. More sales and ad clicks = more revenue for Amazon, powered by AI behind the scenes. Another example: media and gaming companies are using generative AI for content (NPC dialog, virtual world creation), potentially reducing content costs and enabling more immersive experiences that attract users. None of these use-cases individually is the “killer app” that will justify the entire AI hype, but collectively they add real value to existing industries. Over time, that value creation can be captured as profit by the companies that deploy AI well (while those who don’t adopt may fall behind).

Commoditization Favors the Big Boys: The article laments how quickly every new AI feature gets copied, that’s true, and basic GPT-like capabilities are fast becoming a commodity. But when a technology commoditizes, the advantage often shifts to those who have scale and distribution. In other words, commoditized AI benefits the hyperscalers! They can afford to offer AI at low cost (even free) as part of their platform, undercutting smaller players. They also own the channels to millions of customers. Think about it: an upstart AI chatbot company might struggle to sell subscriptions when there are open-source models out there, but Microsoft can bundle a comparable AI into Windows or Office and instantly reach a billion users. Who’s in a better position to eventually profit? We’d bet on the one with the ecosystem. So yes, maybe “OpenAI is the AI industry” as the skeptic says, but that industry is getting absorbed into every major tech company’s offerings. When AI is everywhere, it might not be a standalone profit center; instead it becomes a feature that makes every existing profit center more effective (from search ads to e-commerce to enterprise software sales). This is how the next Amazon or Google will likely emerge, by using AI to reinforce a strong core business, rather than selling AI in a vacuum.

Valuations: Bubble or Early Amazon Moment? We’ll concede: some current AI darlings carry sky-high valuations that assume a lot of future success. For example, Anthropic (maker of the Claude AI assistant) last raised funding at an estimated $30-40 billion valuation, and even smaller outfits like Perplexity.ai have been rumored valued in the high single-digit billions. These are essentially “priced for perfection” or more. If AI progress stalls, many such startups will face consolidation or collapse (we might have our generation’s Pets.com lurking in the herd). However, recall Amazon in 1999: it was losing money, valued astronomically, and almost went under when the bubble burst, only to utterly dominate commerce a decade later. The winners of the AI era could justify today’s valuations and then some; the trick is picking the winners. Our approach? Prefer the platforms and toolmakers that benefit from AI’s rise no matter who wins the model quality wars.

Conclusion: Is Generative AI a Real Industry?

The contrarian article provocatively claims “there is no industry here”. In one sense, he’s right, generative AI is not a standalone industry with clear profits (yet). It’s more of a general-purpose technology, like electricity or the internet, that feeds into many industries. If you look for a line on a balance sheet that says “AI revenues”, you might be disappointed (or misled, as when Microsoft included AI by counting Azure deals). But that doesn’t mean no one’s making money or that it won’t become a sustainable business. From our humble point of view, it just means the money might show up in different places than we expected.

Generative AI is very real, not as a traditional industry with its own Fortunes 500 giants (again, not yet), but as a transformative force across multiple sectors. The economics of it are still shaking out. We’re in the heavy investment phase: companies are spending big (often sacrificing short-term earnings) to build AI capabilities and market share. This is much like the early 2000s with the web, or the early days of smartphones. It takes time for the monetization machine to catch up to the user excitement.

So, “Is AI a real industry?” If you mean are there profitable businesses built on generative AI today, the honest answer is “just a few, and mostly the infrastructure providers”. But if you ask will AI generate real profits in the future and for whom, our answer is an emphatic yes, for those who integrate it best.

Crucially, we believe the winners will be the ones with strong existing platforms and those enabling the AI surge, rather than pure-play AI startups burning cash on speculative tech. That’s why in the Swiss Portfolio, we’re focused on companies that embed AI into a broader value engine or benefit from AI demand:

Alphabet (Google): a hyperscaler with massive reach, using AI to protect and expand its core ad/search business and cloud services. Google’s AI research also ensures it remains at the cutting edge, converting “AI demand” into cloud contracts and new features that keep users in its ecosystem.

NVIDIA and AMD: the chipmakers powering the AI revolution. As noted, Nvidia’s revenues are skyrocketing thanks to AI chip demand. AMD, too, is developing AI accelerators and stands to gain as demand diversifies beyond Nvidia.

ASML: the less obvious hero. ASML makes the lithography equipment needed to produce advanced semiconductors (the brains behind AI). Every surge in AI chip orders means fabs need more ASML machines. It’s a more steady, behind-the-scenes beneficiary of the AI trend.

Microsoft: worth mentioning given its heavy AI push (OpenAI partnership, Azure AI services, and integrating Copilot across its product suite). Microsoft is turning AI into higher software prices and sticky cloud usage, a playbook that will likely pay off handsomely over time.

Amazon (and Meta): another Big Tech juggernaut benefiting on multiple fronts: AWS selling the compute and the company’s retail side using AI to boost sales and ad revenue. Amazon’s recent AI features in ads and shopping show how it can directly convert AI into commerce dollars. (And let’s not forget Amazon’s $4B investment in Anthropic, they know cloud clients will want AI, and they aim to serve it to them).

Netflix, Spotify, Duolingo: we highlighted this as a case of a nimble company using AI to outpace competitors. It turned AI into faster product rollouts, which should strengthen its market position in language learning, edutainment, streaming, music, etc. It’s a model for how even small/mid companies can leverage AI for competitive advantage.

Infrastructure & Industrials (IESC, PSIX, etc.): Interestingly, the AI boom has physical-world ripple effects. All those new AI datacenters being built require electrical systems, cooling, and backup power. Holdings like IES Holdings (IESC), which installs electrical and tech infrastructure, or Power Solutions International (PSIX), which provides power systems (think generators, engines), can get a piece of the action as the need for robust power and infrastructure grows. These may not be pure AI plays, but they’re part of the supply chain that will see increased demand as AI expands.

In summary, while the contrarian raises valid concerns (and we should remain vigilant about valuation bubbles), we believe generative AI is more than just hot air. It may not mint profits in isolation today, but it is steadily weaving itself into the fabric of business. The money, in our view, will increasingly flow to those companies that harness AI to deliver better products/services or to run operations more efficiently. That’s where our investments are focused.

“The time to be greedy is when others are fearful”.

The doom-and-gloom take that “there is no AI industry” is certainly fearful, and maybe a bit premature. We’d rather learn from it, temper our expectations, but still position ourselves for the very real AI-driven future unfolding. After all, contrarian arguments are most valuable when you’ve done your homework and still arrive at a different conclusion.

So, is Generative AI a real industry? Not in the simplistic sense, it’s not a gold mine you can just dig profits out of today. It’s more like a new electricity: it will shock some companies, illuminate others, and ultimately power those who know how to use it. And we intend to be on the side of those who use it. 🚀💡

🫶 Once again, a HUGE Thank You for supporting the Swiss Portfolio. Every like, share, and comment helps us reach more thoughtful investors. Thanks a lot for spreading the word.

📬 Read us. Join us. Sleep well.📈✨✨

🚀 Coming soon on the Substack:

👉 In upcoming posts, We’ll cover:

More strategies to track your finances and build a clear 5-year financial plan.

How to optimize taxes when investing from Switzerland, a huge advantage vs US & EU (free).

Continued deep dives on asymmetric opportunities we’re tracking, including my recents Azeus deep dive, Tetragon deep dive (free).

The “move to Switzerland” playbook for investors and entrepreneurs (paid).

The Swiss Portfolio allocation strategy, which has returned 80%+ in a year and 35%+ CAGR over the past 5 years (paid).

Everyone wants to call AI the “next internet” — but the internet scaled with falling costs. Generative AI is scaling with rising costs. Until that flips, calling this the next Amazon feels more like hope than analysis.

Focus on the few that are trending and have an edge. Compound the winners. Protect your downside through risk and exit management. Keep it simple.