$NFLX Quick Thoughts

Bullish Crowd, But a Harder Game in 2025

Netflix ($NFLX) reports Q1 2025 earnings this Thursday, April 17, after the market close.

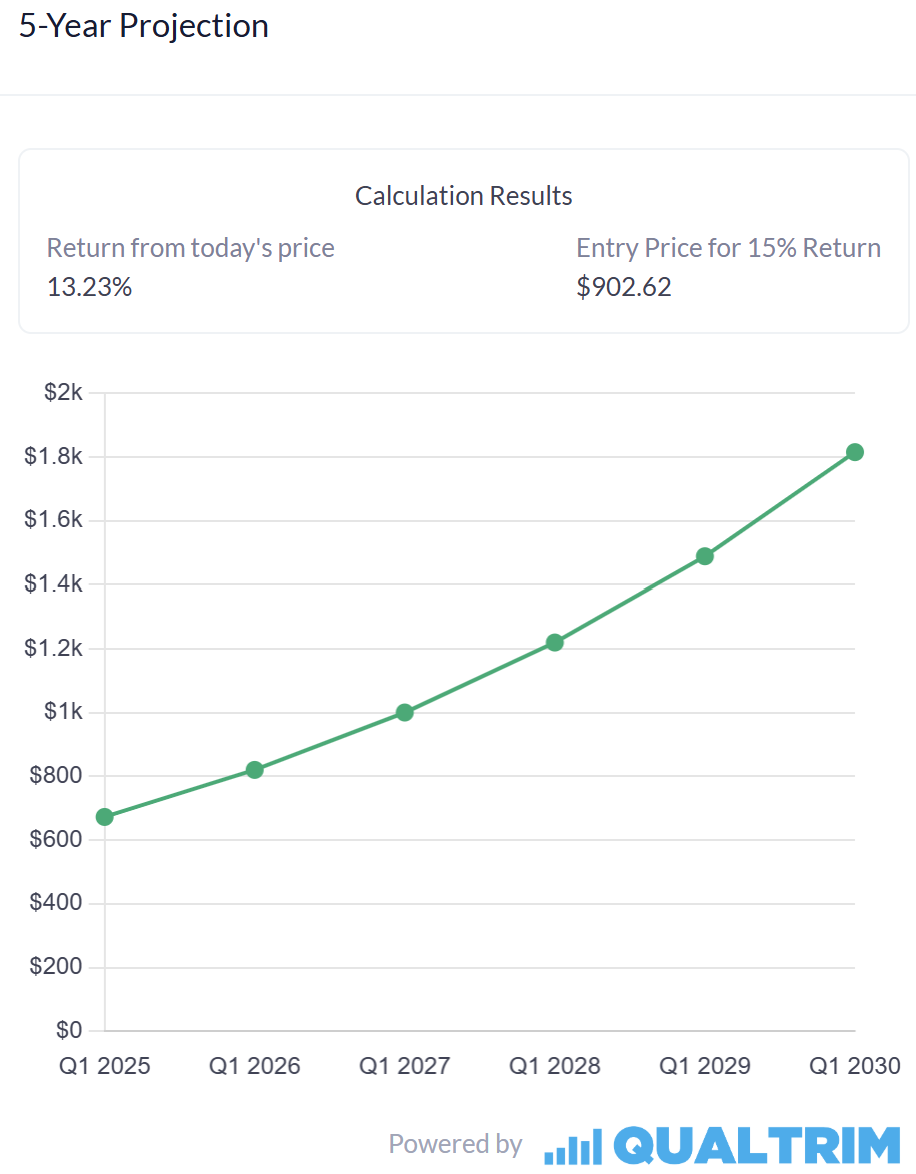

Let’s make a few long-term assumptions. Using trailing 12-month EPS of $19.83, a 5-year EPS growth rate of 25%, and a forward multiple of 30x during next 5 years (well below its current P/E of 48x), you’d land on a 13% annual return. To hit a more ambitious 15% target return, you’d need to buy shares around $900, not an outlandish ask given current momentum and historical growth rates.

These assumptions are far from aggressive. EPS has grown over 30% annually across the past 1, 2, and 5 years, a rare consistency for a tech platform in a post-pandemic world that continue to surprise the most experienced investors.

However, last quarter’s guidance was more tempered:

Revenue: $10.42B, up 11% YoY.

Diluted EPS: $5.58, up 5.7% YoY.

That may look underwhelming on paper, but it's worth noting that Q1 2024 saw EPS up 83% YoY, setting a very tough comparison base. The real question now is: can Netflix show it's not just growing, but doing so consistently and efficiently?

Netflix now trades at around 39x forward earnings, no longer in value territory. The market treats it less like Disney and more like Meta: a high-margin platform that demands near-perfect execution to maintain its premium.

The risk? Netflix is volatile. A slight miss on earnings or subs (well, no longer reporting subs), and the stock can drop 10–20% overnight. But a beat, especially on ads or engagement, could send it roaring higher.

To a degree, yes. Netflix offers an affordable, high-value entertainment product, which historically performs well in slowdowns, it’s the classic “stay-at-home” trade.

But there are caveats:

Cost-conscious consumers may downgrade to the ad-tier.

Currency pressures and inflationary content costs could compress margins.

That said, recurring revenue, global scale, and a growing ad business make Netflix relatively insulated, especially compared to ad-only models or companies reliant on physical goods.

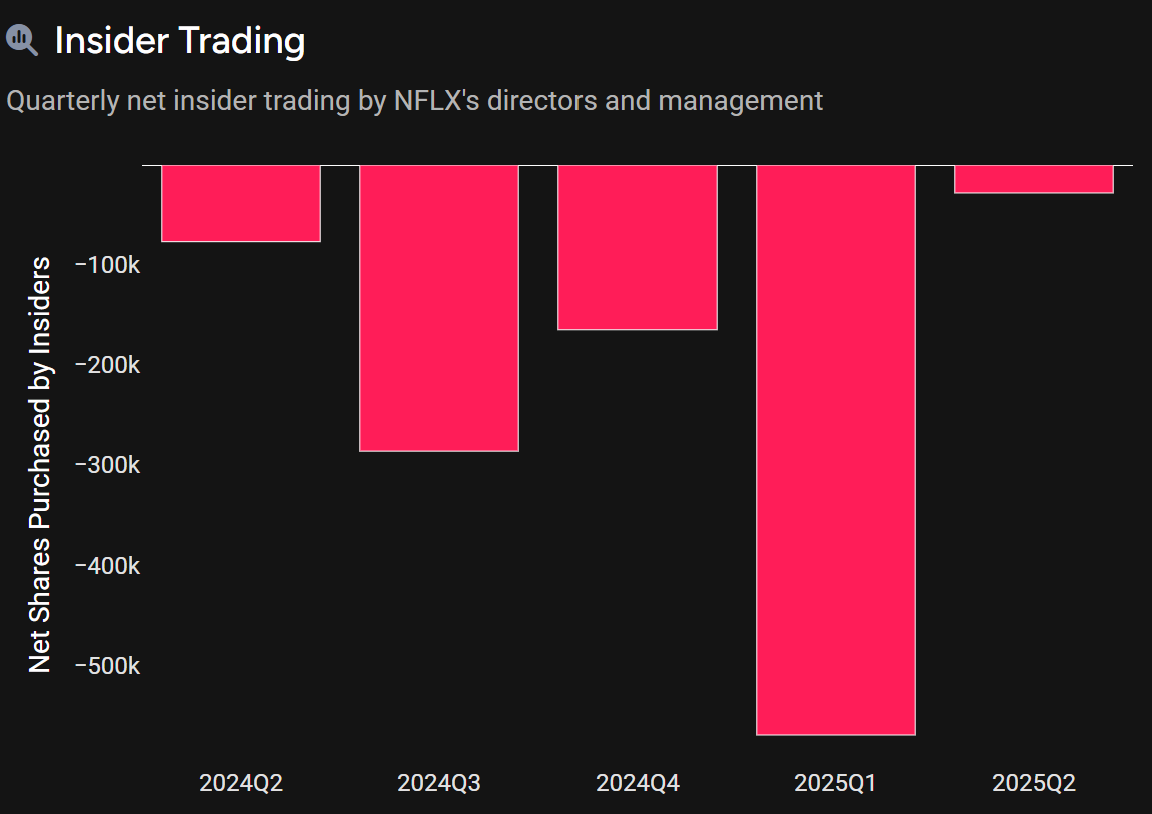

Insider activity has been notably elevated during the first quarter, a signal worth watching in light of current valuation levels and broader inflation/recession risks.

But one thing remains clear: Netflix has consistently outperformed both the S&P 500 and the Nasdaq over time, a true testament to its competitive moat, ability to reinvent itself, and global scale.

But 2025 is not a repeat of 2020. The easy wins, like the password-sharing crackdown and initial price hikes, have largely been captured. That said, Netflix still holds strong pricing power, and if they announce further increases, subscribers are likely to follow.

From here, growth will depend on new levers: gaming, live sports, deeper ad-tech, or something we haven’t seen yet.

Netflix remains a streaming juggernaut. But now, the treadmill gets faster.

(Not financial advice, of course — just a quiet thought).