Leading Edutainment: Duolingo ($DUOL)

Will Edutainment be as Lucrative as Netflix’s Entertainment?

1. Summary

1.1 Investment Idea

Duolingo (NASDAQ: DUOL) is the world’s leading digital language-learning platform, known for its green owl mascot and gamified lessons. The company’s freemium model and huge user base position it to dominate a large, growing market in education technology. Duolingo has rapidly expanded its user reach and revenue while recently achieving profitability, demonstrating an ability to scale sustainably. Investing in Duolingo is essentially a bet on continued robust user growth, successful monetization of its massive user base, and expansion into new learning verticals – all driven by a tech-savvy, founder-led team with a long-term mission. In short, Duolingo offers exposure to a category-leading “edutainment” business that blends serious growth with a playful brand.

1.2 Why It Is Compelling

Explosive User Growth & Market Leadership: Duolingo’s app has become the world’s most popular way to learn languages, with over 40 million daily users (DAUs) (vs 26.9 in 2023) and 116 million monthly users (MAUs) as of Q4 2024 (vs 88.4 in 2023) sec.gov. It is the top-grossing app in the Education category on mobile app stores. This scale provides a strong network effect and a data advantage.

Strong Financial Momentum: The company delivered record revenues of $748.0 million in 2024 (41% YoY growth), driven by a 50% YoY increase in subscription revenue. Duolingo achieved its first full-year GAAP profitability in 2024 with $88.6 million in net income, and its free cash flow impressive 36.8%. This combination of high growth and positive cash flow is rare in the edtech space.

Engaging Product & Brand: Duolingo has a unique engagement through gamification. Over 10 million users have maintained a streak (daily usage) of one year or longer. Its quirky marketing – from a 5-second Super Bowl ad to viral TikTok videos – has made the brand iconic and “unhinged” in a delightful way. In fact, AdAge named Duolingo “Marketer of the Year” in 2024 for its creative campaigns. This strong brand equity lowers customer acquisition costs and increases user loyalty.

Multiple Growth Avenues: Duolingo is expanding beyond languages. It launched Duolingo Max, a premium tier with AI tutoring features, which already accounts for 5% of paid subscribers within its first year. The company has also introduced new learning apps in math and music, tapping into broader education markets. Additionally, the Duolingo English Test (an online English proficiency exam) provides another growth vector by challenging traditional testing services.

Founder-Led with “Green Machine” Culture: Co-founder/CEO Luis von Ahn (7.5% owner) and his team instill a culture of constant experimentation known internally as “The Green Machine”. This data-driven approach to product improvement and A/B testing underpins Duolingo’s ability to improve retention and conversion metrics continuously. Management’s long-term vision and significant insider ownership align their interests with shareholders.

1.3 Risks

Rich Valuation: Duolingo’s stock price reflects very high expectations. It trades around ~50–75× next-twelve-month earnings and a ~2% NTM free cash flow yield. This premium valuation means any slowdown in performance could trigger a sharp correction in the share price.

Competition & Market Saturation: The online language learning space is competitive. If Duolingo’s user growth plateaus or competitors or AI tools replicate its features, the company’s expansion could slow.

Shareholder Structure & Dilution: The founders retain outsized voting control (76.1%) via super-voting shares, so public shareholders have little say in governance. Duolingo also issues significant stock-based compensation, causing ~5% share dilution per year. While this aligns employees, it can gradually erode shareholder value if not matched by growth.

Macro & Regulatory: A global economic downturn could reduce discretionary spending on apps (fewer paid subscriptions, lower ad rates). Changes in app store policies or data/privacy regulations could create headwinds or add costs for Duolingo. As a global app, it also faces geopolitical risks (e.g. restrictions in certain countries) and currency fluctuations that can affect results.

2. Business Model

2.1 History of the Company

Duolingo was founded in 2011 by Luis von Ahn and Severin Hacker with a mission to make education free and accessible to all. Luis von Ahn, a computer science professor who sold two previous companies to Google (including reCAPTCHA), channeled his expertise in crowdsourcing and gamification into language learning. The company’s quirky name is a nod to “duo” (for two languages) and reflects its bilingual learning approach.

Duolingo’s early strategy was to offer a completely free language app and monetize indirectly. In its very beginnings, Duolingo tried a novel model: having users translate web content as language practice, then selling those translations to companies. This proved difficult to scale, so the company pivoted to more traditional monetization while keeping the learning content free. It introduced advertising and a premium subscription (originally called Duolingo Plus, later Super Duolingo and now just “Super” or Duolingo Max for the highest tier).

Over the past decade, Duolingo has grown from a tiny project (with a handful of courses and an owl mascot named “Duo” that sent playful reminder notifications) into a global platform with 500+ million registered users and dozens of language courses. The app’s focus on bite-sized lessons, game-like rewards, and a humorous tone helped it go viral. By 2014, Duolingo became the #1 education app on app stores. The company raised venture capital from notable investors (Union Square Ventures, Kleiner Perkins, Google Capital, etc.) and eventually went public in July 2021 at $102 per share, giving it a ~$3.7 billion valuation on IPO day.

Key milestones in Duolingo’s history include:

2012-2014: Launch of the app and rapid user adoption, offering courses in major languages.

2017: Introduction of Duolingo Plus (ad-free version with extra perks) as a subscription offering, marking the start of its freemium monetization in earnest.

2018-2019: Expansion into additional content like Duolingo Stories (short interactive stories for reading practice) and events. The company also began developing the Duolingo English Test (DET) around this time – an online proficiency exam to rival TOEFL/IELTS.

2020: Huge surge in usage during COVID-19 lockdowns (people stuck at home turned to language learning; Duolingo’s user base swelled). In April 2020, Duolingo surpassed 1 million paid subscribers.

2021: IPO on Nasdaq. By this time Duolingo had around 2 million paid users and 40 million MAUs. The company kept adding new courses (including fantasy languages like Klingon and High Valyrian, purely for fan fun) and features.

2022: Duolingo acquired a small animation studio (Gunner) to boost content creation. It ended 2022 with ~$369 million revenue and ~4 million paid subscribers (strong growth from 2021’s $250M revenue and ~2M subs).

2023: Launch of Duolingo Max, a higher-priced tier integrating GPT-4 AI for features like “Explain My Answer” and AI conversation practice. Also launched Duolingo Math and began working on Duolingo Music courses. By end of 2023, paid subscribers reached 6.6 million.

2024: Rapid growth continued with Duolingo finishing 2024 at 9.5 million paid subscribers and $748 million revenue. The company’s marketing stunts hit new heights (or depths?): In early 2025, Duolingo “killed off” its mascot Duo in a staged social media saga and then “revived” him after users earned 50 billion points collectively – a bizarre campaign that nevertheless drove engagement. Such antics demonstrate the company’s offbeat approach to keeping its brand in the spotlight.

Today, Duolingo’s core business is still the mobile app where users can learn 40+ languages for free. Around this core, it has built a subscription business, an ad business, and an education testing business. It has also nurtured a passionate community – many contributors to its courses are volunteers, and users often form clubs or compete on leaderboards, reinforcing the communal feel.

2.2 Key Concepts Regarding Its Business

Duolingo’s business model rests on a freemium, direct-to-consumer app with gamification at its heart. Key concepts include:

Gamification: Duolingo turns learning into a game. Users earn experience points (XP), maintain streaks for daily practice, level up, and compete on weekly leaderboards. The app is filled with friendly competition and playful animations. This gamification drives habit formation – as noted, making learning feel like a game yields “small, consistent wins” that boost confidence and retention.

Freemium Model & Scale: Duolingo’s core strategy is to offer a robust app for free to attract the widest audience. This freemium approach has amassed over 500 million registered users, far more than any paid-only competitor. The huge user base creates community dynamics (leaderboards, forums) and provides Duolingo with vast data to improve lessons. Scale is a self-reinforcing advantage: more users lead to more data and word-of-mouth, which in turn attract more users.

Efficient Content Creation: Duolingo doesn’t rely on expensive live classes or large content teams for each course. It uses a small in-house staff and community volunteers to develop and update courses (many language courses were contributed by volunteer experts). Continuous A/B testing and user feedback allow Duolingo to refine content at low cost. This approach lets the company offer 100+ courses in over 40 languages without the heavy content costs that traditional education companies would incur.

“The Green Machine” and A/B Testing: Duolingo attributes its success not to any one magic formula, but to its process. Internally dubbed “The Green Machine,” Duolingo’s approach is to run thousands of experiments to optimize everything from course content to the shade of green on a button. This data-driven culture means features are rigorously tested. Saving the distances, this philosophy could be compared to Amazon’s “Culture of Experimentation”, where continuous A/B testing and customer-centric iteration are core drivers of product and service improvements.

Multiple Revenue Streams: While the subscription is the primary revenue driver (81% of 2024 revenues), Duolingo also earns money from advertising and its English certification test:

Advertising (7.3%): Free users see short ads at the end of a lesson. Duolingo carefully balances ads so as not to hurt retention. Advertising comprised a meaningful portion of revenue (part of the ~19% “Other” revenue in 2024). Ads leverage Duolingo’s large user base and high engagement time. However, ad revenue has lower gross margins than subscriptions (in 2024 Duolingo’s total gross margin dipped slightly due to growth in lower-margin ad revenue).

Duolingo English Test (DET) (6.1%): This is an online exam that non-native English speakers can take to certify their proficiency. It costs ~$49 per test, and is an attractive alternative to tests like TOEFL, especially because it can be taken from home. Over 4,000 universities accept the Duolingo test as of 2024. The DET saw higher demand during the pandemic (when test centers closed) and continues to grow. It falls under “Other” revenue and represents a high-margin business (digital delivery of a standardized test).

In-app purchases (5.2%): Much smaller, but Duolingo does have a virtual currency (lingots or gems) that users can buy with real money to unlock cosmetic items or bonus lessons. This is not a big revenue driver but is another piece of the monetization puzzle (also included in “Other”).

In essence, Duolingo’s business model can be summarized as Acquire users for free with a great product -> Engage them via gamification -> Monetize a slice of them via subs, ads, and exams. This model yields a strong growth flywheel, as high engagement leads to more word-of-mouth and thus more new users.

2.3 Revenue Analysis by Segment

Duolingo’s revenue mix and global reach illustrate balanced growth:

By Product: Subscriptions are the largest revenue driver (~81%), followed by advertising (~7.3%) and the English Test/other (~6.1%). Subscription revenue is growing the fastest (thanks to rising paid subscriber counts and price increases), while ad revenue and DET fees, though smaller, are also climbing.

Geography: Revenue is diversified globally. Customers located in the United States accounted for 42%, 45% and 46% of total revenues for the years ended December 31, 2024, 2023 and 2022, respectively. No other country accounted for more than 10% of revenue in the periods presented. This international footprint means Duolingo’s growth comes from many regions, though it also entails navigating currency swings and local preferences.

Seasonality: Duolingo sees a mild seasonal bump in the fourth quarter (during holidays/New Year’s, when usage and subscriptions often increase), but overall growth is driven more by secular trends and product improvements than by seasonality. In general, the company has demonstrated strong user and revenue growth throughout the year.

2.4 Capital Allocation

Duolingo’s capital allocation is straightforward, as a relatively young growth company:

Reinvestment in R&D: The company prioritizes product development. In 2024, R&D expense was 31% of revenue (down from 37% in 2023). By contrast, Sales & Marketing was only ~12, reflecting Duolingo’s efficient organic growth (viral marketing and brand strength keep marketing costs low). Most spending goes into improving and expanding the product.

Cash and M&A: Duolingo is debt-free and has built a large cash buffer (about $877M in cash and short-term investments at the end of 2024. It has not engaged in any large acquisitions – the only notable purchase was a small animation studio in 2022 to bolster content creation. The company has not issued dividends or buybacks, opting to retain capital for growth opportunities. This conservative approach gives Duolingo flexibility to invest in new initiatives and withstand potential downturns.

3. Market Share and Industry Position

3.1 Company’s Dominance in Its Sector

Duolingo is by far the largest digital language-learning platform, commanding a dominant share of the market. In terms of users and usage, it vastly outpaces any competitor. With ~$750M in 2024 revenue, Duolingo likely exceeded the combined revenue of its main rivals (e.g., Babbel and Rosetta Stone).

Its scale and brand recognition make it the default choice for millions of language learners. This leadership creates a virtuous cycle: learners gravitate to the most popular app (Duolingo), which further strengthens its position. Competitors, by contrast, operate at a much smaller scale and struggle to match Duolingo’s breadth of content and pace of innovation.

3.2 Market Trends and Total Addressable Market (TAM)

The demand for language learning is massive and increasingly shifting online:

Digital & Mobile Shift: Learners worldwide are moving from classroom and textbook methods to app-based platforms. Growing internet and smartphone access, especially in emerging markets, is enabling hundreds of millions to learn online. The COVID-19 pandemic accelerated this trend by normalizing remote and self-paced learning. According to market research, the global language learning market (including offline and online) was worth about $59 billion in 2023 and is projected to reach $106 billion by 2030, ~8.7% CAGR.

Global English Demand: English learning is a particularly strong driver – in many countries across Asia, Latin America, and Europe, there is huge demand to learn English for career or educational opportunities. Duolingo, which offers English courses for speakers of dozens of languages, directly taps this trend. Overall, the language learning industry (~$60B in 2023) is projected to grow substantially, and the online segment is the fastest-growing part. With roughly 1.8 billion potential learners, Duolingo’s user base is only a fraction of its addressable market, indicating ample room to expand as more people turn to digital learning solutions.

Mobile-First Learning: An important trend is the shift to mobile devices for education. Duolingo, being mobile-first, is riding this wave. With increasing smartphone penetration globally (especially in emerging markets), many users who never had access to quality language instruction now can learn via apps. By 2025, it’s estimated over 6.5 billion smartphone users worldwide – a huge audience for mobile learning. Additionally, people prefer the convenience of micro-learning on the go; Duolingo’s bite-sized lessons align perfectly with modern attention spans and busy lifestyles.

Gamification & EdTech Convergence: There’s a broader trend of making learning more game-like (to improve engagement) and making games more educational. Duolingo sits perfectly in this convergence. Other edtech products are now adding gamified elements, validating Duolingo’s approach. Simultaneously, serious games and even some videogames now incorporate language learning or educational content. The success of Duolingo has set a benchmark for user engagement that others in edtech aim to emulate.

AI in Education: The rise of AI (artificial intelligence) is transforming language learning. Adaptive algorithms can personalize lessons. Duolingo has been integrating AI for years (its courses adapt to user performance, and its Duolingo Max uses GPT-4 for explanations). The trend going forward: AI tutors, speech recognition, and content generation will make apps even more effective. Duolingo’s recent focus on features like AI conversation partners (e.g., the character Lily for speaking practice) is tapping into this.

Acceptance of Online Credentials: Another trend benefiting Duolingo is increasing acceptance of online learning credentials. The Duolingo English Test, for instance, gained legitimacy when universities were forced by the pandemic to accept online exams.

In summary, the tailwinds for Duolingo are significant: a huge global population of potential learners, increased reliance on digital tools, and technological advances that make app learning more powerful. The company’s growth north of 40% indicates it’s capturing market share and also benefiting from market growth.

Importantly, Duolingo’s low-cost, mobile-based model is especially suited to emerging markets – places with millions of aspirational learners but limited access to traditional classes. For example, if in India alone tens of millions want to improve their English, Duolingo can tap that at scale in a way brick-and-mortar institutes cannot. This positions Duolingo as perhaps the only viable way to educate such vast numbers affordably, which underscores how large its opportunity is.

3.3 Competitors

Duolingo faces competition from other language learning providers, but none match its scale or growth:

Babbel: A subscription-based language app (from Germany) targeting adult learners. Babbel generated around $270M revenue in 2022 which grew to €330M ($350M) in 2023 – roughly half of Duolingo’s 2024 revenue. It offers comprehensive courses but requires payment after a short trial, which limits its user base relative to Duolingo’s free model. Babbel appeals to serious learners (especially in Europe) and monetizes well per user, but its overall reach and data pool are far smaller than Duolingo’s.

Rosetta Stone: A legacy brand known for its old CD-ROM language software, now offering a subscription app. Rosetta Stone emphasizes immersive learning without translations. It remains in use by some corporations and schools, but in the consumer market it’s now a niche player. Its user base and engagement are a small fraction of Duolingo’s, as many learners have migrated to more interactive, game-like apps.

Other Apps & New Entrants: Numerous smaller apps (Memrise, Busuu, Lingodeer, etc.) compete for segments of the market, often focusing on specific languages or techniques. While some have loyal followings, none approach Duolingo’s ubiquity. A potential future threat could be a major tech company or well-funded startup launching a rival product (especially one leveraging AI), but to date Duolingo’s dominance in the mass market has gone essentially unchallenged. In summary, Duolingo enjoys a very strong competitive position. Its freemium model, massive user base, and continuous innovation have created high barriers to entry. Competitors exist, but Duolingo is the clear market leader in usage and revenue.

Competitive Position: Duolingo’s edge over all these competitors lies in its blend of free accessibility, engaging design, and constant innovation. Babbel might monetize better per user, but Duolingo grabs many more users. Rosetta Stone might have deeper content, but Duolingo’s agile development adds new features faster (like AI tutoring, social features, etc.). If we look at market share of active users, Duolingo probably holds the lion’s share of the mobile language learning market – easily more than half. In terms of revenue share, Duolingo also leads now (with ~$750M, it likely surpasses Babbel, Rosetta, and others combined in consumer revenue).

3.4 Growth Potential

Duolingo has multiple avenues to continue its rapid growth:

International Expansion: The company can deepen its penetration in regions like Asia, Latin America, and others where millions of new users come online each year. Increasing localization of courses (teaching English from more native languages, adding culturally tailored content) can attract more learners in these markets. As these users gain disposable income, they also represent future subscriber growth.

New Products & Monetization: Duolingo’s expansion into new subjects (like math, and potentially other skills) can broaden its appeal beyond language learners. If the Duolingo method proves effective in other domains, it opens up education markets larger than the language niche. Additionally, Duolingo can introduce more premium features or tiers (family plans, advanced content, or live tutoring) to boost monetization. The introduction of a higher-priced Duolingo Max subscription is one step in this direction.

Duolingo English Test (DET) Growth: The DET provides a significant growth opportunity as it becomes more widely recognized. The global market for English proficiency exams is worth billions of dollars, and Duolingo’s convenient online test can capture a share of that. Continued acceptance by universities and institutions (already thousands of programs accept) will increase the number of test takers. Because many people studying English on Duolingo are doing so for academic or immigration purposes, there is a natural pipeline to convert some of those learners into DET customers. By executing on these opportunities, Duolingo can sustain a high growth rate for years. The company’s current footprint is large, but its potential reach – across more countries, more subjects, and more services – is even larger.

4. Management Quality

4.1 Experience

Luis von Ahn (Co-Founder & CEO): Luis is a remarkable figure. A native of Guatemala, he came to the U.S. for university and earned a Ph.D. in computer science. He’s famous for inventing CAPTCHA (those little “type the letters” tests to prove you’re human) and later reCAPTCHA, which he sold to Google in 2009. Luis was a professor at Carnegie Mellon University, specializing in human-computer interaction and crowdsourcing. He started Duolingo in 2011 with the idea of translating the web while teaching languages (a crowdsourcing twist). As CEO, Luis has guided Duolingo’s product vision to emphasize accessibility and fun. He is known to be passionate about education – he often repeats that the mission is to “make learning free and fun”. Importantly for investors, Luis has proven he can shepherd a startup to a successful public company and navigate transitions (pivoting the business model, embracing mobile, etc.). He’s now focused on integrating AI into learning, stating he’s “all in on AI” to turn Duolingo into an automated tutor. His track record (multiple successful ventures) and academic grounding give him credibility both in tech and education. At 46 years old, he’s relatively young for a CEO of a multi-billion company, implying many potentially energetic years ahead at Duolingo’s helm.

Severin Hacker (Co-Founder & CTO): Severin was Luis’s student at Carnegie Mellon and co-founded Duolingo at age 22. He serves as CTO, overseeing the technology and engineering teams. Severin, true to his name, is the technical wizard behind the scenes that built Duolingo’s platform to scale to hundreds of millions of users. He holds a Ph.D. in computer science as well. His focus has been on the adaptive learning algorithms and the A/B testing framework that powers the “Green Machine.” Having a co-founder CTO still with the company (and relatively young, 40) is a big asset – it means the original DNA of innovation remains strong.

Management Bench: Beyond the founders, Duolingo’s executive team includes experienced folks:

Matt Skaruppa (CFO): Joined Duolingo in 2020. Previously an investor at Capitol G (Google’s growth fund) and an investment banker. He helped steer the company through IPO. Under his financial leadership, Duolingo has achieved profitability and maintained a strong balance sheet, indicating prudent financial management.

Uulaa (Natalia) Guseva (CPO - Chief Product Officer): (If still in role; Duolingo had a CPO role to drive product strategy.) The product team’s strength is evident in the constant rollout of features. They likely have seasoned product managers and designers, some coming from gaming industry backgrounds (since Duolingo recruits people who understand engagement and mobile games).

Cammilla (Camm) Velasquez (SVP of Product): Known for leading the development of Duolingo Max and other initiatives. She had stints at LinkedIn and other tech firms, bringing user experience expertise.

Learning & Curriculum Experts: Duolingo employs linguists and learning scientists to ensure its courses are pedagogically sound. For example, Dr. Cindy Blanco, a learning scientist who often communicates how Duolingo’s methods align with language acquisition research. This blend of academic insight with tech execution is a management strength.

Marketing Team: Duolingo’s marketing, led by people like Zaria Parvez (who was behind their TikTok strategy, famously a 23-year-old social media manager who turned Duo into a TikTok star), shows that management is willing to empower young creative talent and take unconventional approaches. The fact that Duolingo’s marketing is so effective on a shoestring budget speaks well of managerial savvy in brand-building.

Overall, Duolingo’s leadership mixes academic brilliance, tech industry experience, and creative marketing chops. It’s a relatively young management team in terms of age, but with about a decade of experience running this company through various stages, which is invaluable.

4.2 Management Ownership & Governance

Founders and insiders retain significant ownership and control in Duolingo. CEO Luis von Ahn owns roughly 7% of the company and, through a dual-class share structure, holds a majority of voting power together with Co-Founder & CTO Severin Hacker. This means they effectively control major decisions. While this concentrated control can be a governance concern (public shareholders have limited influence), it also provides stability and continuity in leadership. So far, von Ahn has used this control to keep Duolingo focused on long-term growth and its educational mission. This information can be extracted from last DEF 14A released in April 2025:

Compared to last year, the founders have slightly reduced their shares by approximately 0.35% and 0.79%, respectively, modest changes that still reflect strong alignment with Duolingo's long-term potential.

The consistent insider selling over the past five quarters, most notably the sharp spike in Q4 2024, appears to be primarily driven by opportunistic sales during a period of peak share price, rather than any loss of confidence. As evidenced in the latest DEF 14A, the founders have kept their positions practically unchanged.

Management’s incentives are aligned with company performance. Stock-based compensation is used to attract and retain talent, resulting in about 1% annual dilution – a moderate level. The board includes independent directors, and to date no governance red flags have emerged. Overall, investors are largely trusting the founder’s vision and stewardship, which has been justified by Duolingo’s strong results so far.

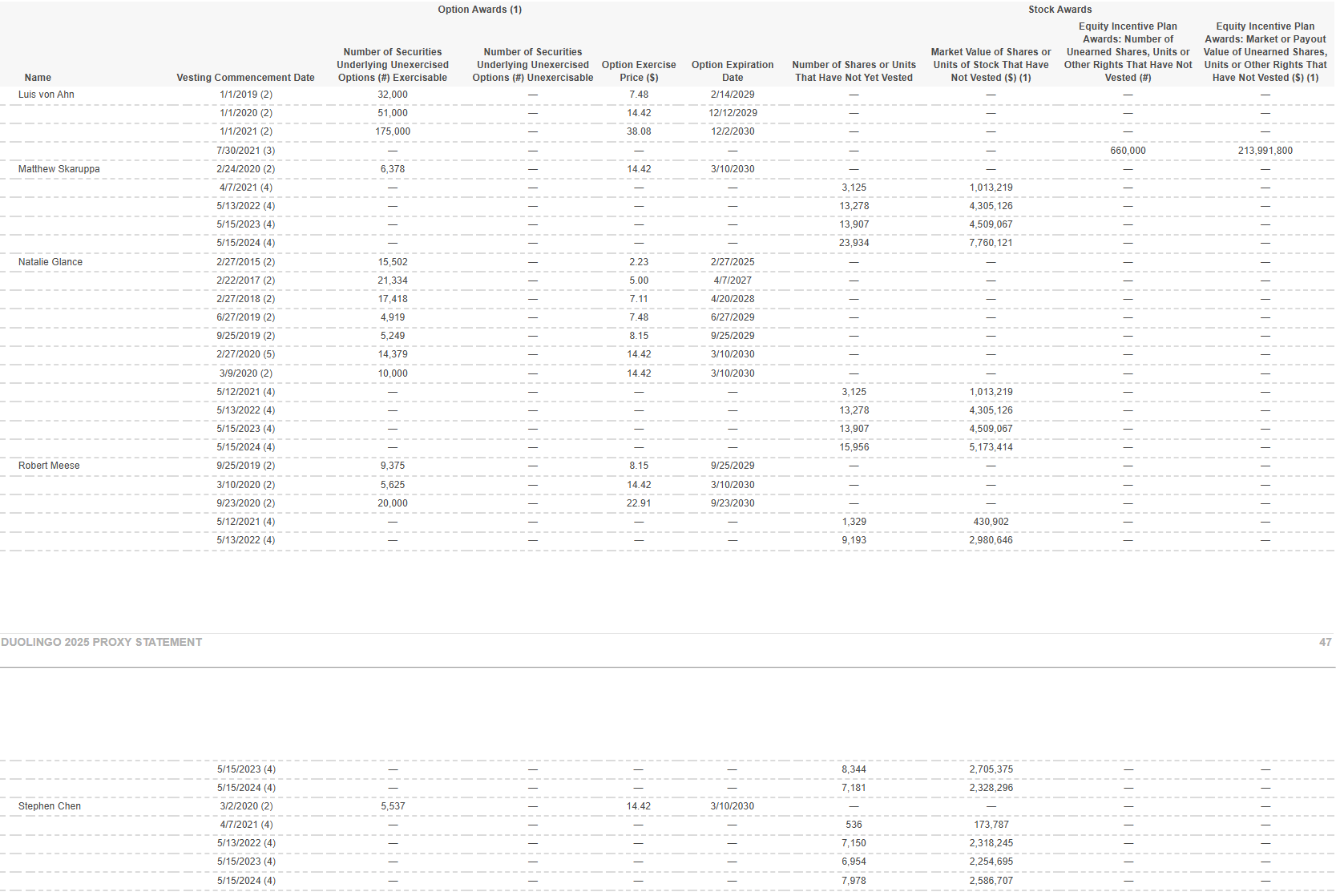

The significant value realized by Duolingo executives through option exercises and RSU vesting in 2024 highlights stock-based compensation as a key driver of insider activity, making it a critical metric for investors to monitor going forward:

The large volume of outstanding awards and unvested RSUs across the team reinforces that equity compensation remains a powerful incentive mechanism and a key metric to monitor for dilution and insider motivation.

4.3 Culture and Transparency

Duolingo’s internal culture is highly data-driven and mission-focused. The team runs thousands of experiments (A/B tests) each year, using metrics to guide product improvements – hence the “Green Machine” nickname for its rigorous optimization culture. This constant experimentation drives the app’s high engagement and effectiveness. The company also emphasizes its mission of free education to keep employees and users aligned with its core purpose.

From a shareholder perspective, management has been reasonably transparent and long-term oriented. They regularly share detailed metrics (e.g., DAUs, subscriber counts, and even streak statistics) and have a clear strategy to balance growth with profitability. Despite the concentrated voting control, management has treated minority shareholders equitably by focusing on increasing the overall value of the company. In sum, Duolingo’s management – in vision, execution, and cultural ethos – is a strong asset for the business.

5. Competitive Advantages (Moat)

Duolingo has built several competitive advantages that protect its market position:

Brand Recognition & Large User Base: Duolingo’s brand is exceptionally strong in the edtech space. Its friendly green owl mascot and reputation for fun, effective learning give it broad appeal and user trust. This popularity attracts many new users organically. Moreover, Duolingo’s massive user base creates a community network effect (active forums, competitive leaderboards, etc.) that smaller rivals cannot easily replicate.

Data Advantage & AI Integration: With millions of daily exercises completed, Duolingo has an unparalleled dataset on language learning behavior. It leverages this data to personalize lessons and improve its courses continuously. Additionally, the company has been an early adopter of artificial intelligence in its product – integrating machine learning and GPT-4 to enhance conversational practice and feedback. This combination of rich data and AI-driven improvement makes the learning experience increasingly effective, widening the gap between Duolingo and its competitors.

Freemium Model & Accessibility: By lowering the cost barrier to zero, Duolingo has attracted far more users than any paid-only service. Its efficient cost structure allows it to sustain this free model, which in turn builds goodwill and a huge funnel for upselling. Competitors that charge upfront have a much smaller user funnel, whereas Duolingo’s free tier draws in learners globally and then converts a portion to paid subscribers.

Duolingo English Test (DET): The DET is a unique asset that extends Duolingo’s reach into the language certification market. It provides a convenient, online alternative to traditional exams like TOEFL. As DET acceptance grows, it reinforces Duolingo’s ecosystem (users learn on the app and can certify their skills with Duolingo’s test). No major competitor offers a comparable in-house test, giving Duolingo a differentiated edge in the broader language learning and assessment landscape.

6. Risk Factors and SWOT Analysis

6.1 Long-Term Risks (5–10 Years)

Technological or Competitive Disruption: In the long run, new technology could diminish the need to learn languages (e.g. flawless AI real-time translation devices), or a new competitor with a revolutionary learning approach could emerge. Either scenario could erode Duolingo’s user base if it fails to adapt.

Shifting Consumer Habits: The popularity of gamified learning apps might wane over time. Future learners might prefer different formats (such as VR immersive learning or live tutoring platforms). If Duolingo’s approach falls out of favor or a new trend gains traction, the company would need to pivot to maintain engagement.

Overexpansion & Focus Drift: If Duolingo expands into too many areas too quickly, it risks losing focus on its core language product. Spreading resources thin or entering areas where it lacks expertise could undermine the quality that drives its success. The company must carefully manage expansion so that the core user experience remains strong.

6.2 Business-Specific Risks

User Engagement Fatigue: Duolingo’s gamification (streaks, points, leaderboards) keeps learners coming back daily, but some users could eventually get “burned out” or hit a learning plateau and drop off. Keeping content fresh and ensuring learners see progress are crucial to retaining long-term users.

Limited Conversion of Free Users: Duolingo relies on converting a small fraction (~5% of MAUs) of its huge user base to paid subscribers. If that conversion rate stagnates or declines, revenue growth will slow even if overall usage grows. In some markets, users may love the product but never pay due to income constraints, limiting monetization despite high engagement.

Platform Dependence: Duolingo is subject to the rules and fees of Apple’s App Store and Google Play. App store commissions (up to 30%) reduce its net revenue from subscriptions, and any adverse changes in platform policies or algorithms (for example, around app rankings or notifications) could impact Duolingo’s business. While such changes are beyond Duolingo’s control, they remain an ongoing risk of operating in the mobile ecosystem.

Perceived Efficacy: If Duolingo gains a reputation that it’s “just a game” and not sufficient for serious language mastery, some learners (especially those willing to pay) might turn to other solutions. The company needs to continually improve outcomes – through advanced content, AI tutors, and practice features – to demonstrate that learners can achieve meaningful proficiency using the app. Failing to do so could limit its appeal among serious learners.

6.3 Financial Risks

High Market Expectations: Duolingo’s valuation assumes years of high growth and rising profitability. If the company’s growth noticeably decelerates or margins plateau, investor sentiment could turn quickly and the stock’s valuation multiples could compress. In short, any sign that Duolingo’s growth story is losing steam could lead to a sharp decline in the share price given the current high multiples.

Share Dilution: Ongoing stock-based compensation means Duolingo’s share count increases each year. If not offset by commensurate growth in earnings, this dilution will gradually erode existing shareholders’ ownership percentages. While the current dilution rate (~2–3% per year) is moderate, it requires the company to consistently grow value to ensure shareholders aren’t diluted faster than the business is expanding.

Cost Inflation: Certain costs could rise faster than expected. For example, as Duolingo expands, it may incur higher cloud infrastructure expenses, localization costs for new markets, or personnel costs (particularly with competition for AI and engineering talent). If expense growth outpaces revenue growth, it could pressure profit margins. Prudent cost management will be necessary to maintain the company’s path to higher profitability.

6.4 Macroeconomic & Regulatory Risks

Economic Downturn: In a recession, some users might cut back on discretionary spending like Duolingo Plus subscriptions, and advertisers might reduce their ad budgets. While Duolingo’s free tier could see higher usage during tough economic times, its paid subscriber growth and ad revenue could slow. A prolonged downturn could thus impact Duolingo’s financial performance.

Regulatory Changes: Duolingo operates across many jurisdictions and must comply with data privacy laws (GDPR, etc.), consumer protection regulations, and education-specific rules. Changes in these laws or new regulations (for example, restrictions on app data usage or online education content) could increase compliance costs or limit certain features. Additionally, geopolitical events or government actions (like censorship or app bans in certain countries) could restrict Duolingo’s access to some markets, affecting user growth.

6.5 SWOT Summary

Strengths: Duolingo’s strengths (brand, scale, data, profitability) give it an edge over weaknesses (low conversion rate, dependence on app stores). It has major opportunities (expansion into new markets/subjects and English testing) but also faces threats (competition, technological shifts, macro/regulatory risks).

7. Financials Deep Dive

(FY2024 is used as the reference year.)

7.1 Debt and Cash

Duolingo has no long-term debt and a very strong cash position. As of Dec 31, 2024, it held about $785.8 million in cash and equivalents plus $91.9 million in short-term investments (roughly $877 million total). This debt-free balance sheet provides a significant buffer and flexibility, allowing the company to invest in growth initiatives or weather unexpected downturns without financial strain.

7.2 Expense Structure and Capex

Duolingo’s business model is highly asset-light and scalable. Capital expenditures are minimal (around 1% of revenue) since the product is a digital app and content creation is not capital-intensive. Key operating expenses include:

Research & Development: The largest expense, reflecting Duolingo’s continuous product improvement and content development. R&D was 31% of revenue in 2024 (down from 37% in 2023).

Sales & Marketing: Thanks to organic growth, S&M spend is relatively low – about 12% of revenue in 2024 (down from 14% in 2023). Duolingo benefits from viral user acquisition and a strong brand, which keep marketing costs low.

General & Administrative: G&A was roughly 12% of revenue in 2024, covering corporate overhead and support functions. These expense ratios have all been improving (shrinking as a percentage of revenue) as Duolingo grows, demonstrating operating leverage. Duolingo’s cost structure – with low capex and relatively modest marketing needs – supports its path toward higher profitability as revenue expands.

7.3 Income Statement

Duolingo’s financial performance shows rapid growth and improving profitability:

Revenue Growth: 2024 revenue was $748.0 million, up 41% from 2023. This robust growth was driven by increases in paid subscribers (both more subscribers and higher average revenue per subscriber) as well as growth in advertising and English Test fees. Duolingo has sustained a ~40%+ annual growth rate in recent years, reflecting strong execution in monetizing its growing user base.

Net income: Duolingo enjoys high gross margins (estimated above 70%) because the cost of delivering digital lessons to additional users is very low. In 2024, the company also turned an operating profit for the first time – operating income was about 8% of revenue. Net income was $88.6 million (a ~12% net margin).

Achieving double-digit net margins while growing revenue 40%+ underscores the scalability of Duolingo’s model. As revenue continues to grow, the company has the potential to further expand margins by spreading fixed costs over more users.

7.4 Cash Flow

Duolingo’s cash generation is very strong, outpacing its accounting earnings:

Operating Cash Flow: The company generated $285.5 million in operating cash flow in 2024, which is substantially higher than its net income. This is largely due to deferred revenue: many users pay upfront for annual subscriptions, so cash is received early even though revenue is recognized over time. These upfront payments (deferred revenue grew significantly in 2024) provide a cash flow boost.

Free Cash Flow: After minimal capital expenditures, free cash flow was $273 million in 2024 – about 37% of revenue. Such a high free cash flow margin indicates that Duolingo converts a large portion of its revenue into cash. It demonstrates the quality of the earnings and the low capital intensity of the business.

Cash Usage: Duolingo has primarily used this cash to strengthen its balance sheet. It hasn’t needed external financing to fund growth; in fact, it is accumulating cash. The company has ample resources to invest in new initiatives (like developing new courses or features, or selective acquisitions) without needing to raise capital or incur debt. Overall, Duolingo’s financials depict a company that is growing rapidly while already generating profits and significant free cash flow – a rare combination for a tech company of its size and age. This financial strength gives Duolingo the flexibility to continue investing in innovation and expansion.

Stock-Based Compensation (SBC) is something to watch closely. As shown in the chart, SBC reached $110.48 million in 2024, accounting for a significant portion of the company’s financial profile, even as Free Cash Flow rose impressively to $273.4 million. While DUOL is scaling rapidly and FCF growth is strong, the magnitude of SBC, over 40% of FCF for 2024, could raise dilution concerns if the trend continues. It’s a key line item to monitor when evaluating the sustainability and quality of the company’s profitability.

8. Valuation

8.1 Current Valuation Metrics

Duolingo’s stock trades at premium valuation multiples reflecting its high growth profile:

Market Multiples: At about $390 per share (April 2025), Duolingo’s market capitalization is roughly $17.7 billion. This equates to approximately 18× forward revenue and ~68× forward earnings.

The forward free cash flow yield is only ~2%. Investors are clearly pricing in substantial future growth and profit expansion – the stock is expensive relative to current earnings, based on the expectation of continued rapid growth.

However, it is historically rare to find Duolingo trading at a higher yields than it is today.

8.2 Stock Performance & Sentiment

Duolingo’s stock has been volatile since its 2021 IPO, reflecting shifting market sentiment:

IPO and Trough: The company went public at $102 per share in mid-2021. During the 2022 tech sell-off, the stock fell dramatically, reaching lows around $65 by mid-2022 amid a broader retreat from high-growth tech stocks.

Surge to Highs: As Duolingo delivered strong results (high growth and the move to profitability) and market sentiment improved in 2023, the stock rebounded. It hit an all-time high of $441 in early 2025, reflecting significant optimism about the company’s prospects (including excitement around its AI-driven features).

Recent Pullback: After peaking, the stock pulled back to around $300 as of April 2025. This moderation suggests that while investors remain positive on Duolingo, some of the initial euphoria has tempered – likely due to profit-taking and a re-focus on the company’s high valuation. The overall trajectory (from $102 IPO to ~$300-400 now) still indicates strong investor confidence, but the path has seen large swings.

9. Conclusion

Duolingo presents a compelling investment thesis as a category leader at the nexus of education and technology. The company has achieved what few edtech firms have: massive global scale, a loved consumer brand, and a profitable, self-funding business model – all while still in a high-growth phase. In summary:

Dominant Product-Market Fit: Duolingo has turned language learning into an addictive daily habit for millions. Its fun, gamified approach has cracked the code on engagement in a way competitors haven’t, creating a moat of loyal users and viral brand visibility. The phrase “Have you done your Duolingo today?” has entered the zeitgeist (often said half-jokingly as people maintain their streaks).

Financial Firepower and Growth: The company’s 2024 results (41% revenue growth, 51% DAU growth show a business hitting on all cylinders. Importantly, Duolingo is no longer just a growth story; it’s now a growth-and-profit story, generating substantial free cash flow. This reduces downside risk and gives management optionality to invest in new initiatives or weather storms. Few companies are growing this fast and adding cash to the bank.

Long Runway: The journey for Duolingo is likely closer to its beginning than its end. The total addressable market spans billions of potential learners worldwide. Duolingo’s expansion into new subjects (math, music) and services (English testing) could multiply its impact. In a sense, Duolingo’s ambition is to become a universal learning platform – that’s a TAM arguably in the hundreds of billions of dollars when you consider all of education. Even capturing a modest slice of that over the next decade would justify significant further growth.

Execution and Leadership: The company benefits from being founder-led with a clear mission. Luis von Ahn’s vision of accessible education acts as a North Star, and the “Green Machine” execution model ensures data-driven decisions. This combination of vision + execution has delivered so far – and there’s little indication it will falter. If anything, Duolingo seems to be accelerating its pace of innovation (embracing AI, launching new products faster).

Risks in Check (Though Not Absent): Every investment has risks, and Duolingo’s have been discussed: high valuation, competition, sustainability of user engagement, etc. However, Duolingo has shown a knack for proactively addressing challenges – whether it’s adding features to improve speaking skills (mitigating the criticism that “Duolingo doesn’t teach speaking” by introducing Video Calls with AI) or carefully managing monetization not to alienate users. The dual-class share structure means investors are largely betting that the founders will steer the ship wisely – and to date, that bet has paid off.

In a lighter sense, investing in Duolingo is an investment in that persistent green owl who reminds everyone to do better each day. The owl has proven it can not only get people to learn a language, but it can also get investors to believe in the viability of education technology.

For both institutional and retail investors, Duolingo offers an accessible growth story: it’s easy to understand (a globally popular app with subscription revenue), yet has sophisticated underpinnings (AI and behavioral science driving its success). This duality makes it an attractive addition to growth-oriented portfolios, with the caveat that one must be comfortable with the volatility and high multiples that accompany such stocks.

Bottom line: Duolingo has the makings of a long-term compounder – a company that could continue doubling its business over the next few years and beyond. If it executes on expanding its product suite and converting even a fraction of its huge user base to paid subscribers, the upside could be substantial. The company’s mantra of making learning “accessible, effective, and delightful” not only serves a noble purpose but is proving to be a very good business. In conclusion, Duolingo represents a unique blend of mission-driven growth and competitive strength, making it a compelling investment idea for those looking to bet on the future of education.

10. 5-Year Scenario Projections (Excel file for paid subscribers)

To give a sense of Duolingo’s potential trajectory, here we outline scenario projections for the next five years (2025–2029). These projections are estimates and for illustrative purposes:

Base Case: In a base case scenario for Duolingo ($DUOL), we assume a Free Cash

Keep reading with a 7-day free trial

Subscribe to Swiss Transparent Portfolio to keep reading this post and get 7 days of free access to the full post archives.