$GOOGL Quick Thoughts

Sleeping giant or an "Apple moment" in the making?

Alphabet ($GOOGL) reports Q1 2025 earnings this Thursday, April 24, after the market close.

Despite being battle-tested through recession, inflation, and geopolitical volatility, Alphabet is no longer seen as a pure monopoly. With competitive disruption rising, here’s what the market expects:

Revenue: $89.18B, up 10.7% YoY.

Diluted EPS: $2.01, up 6.3% YoY.

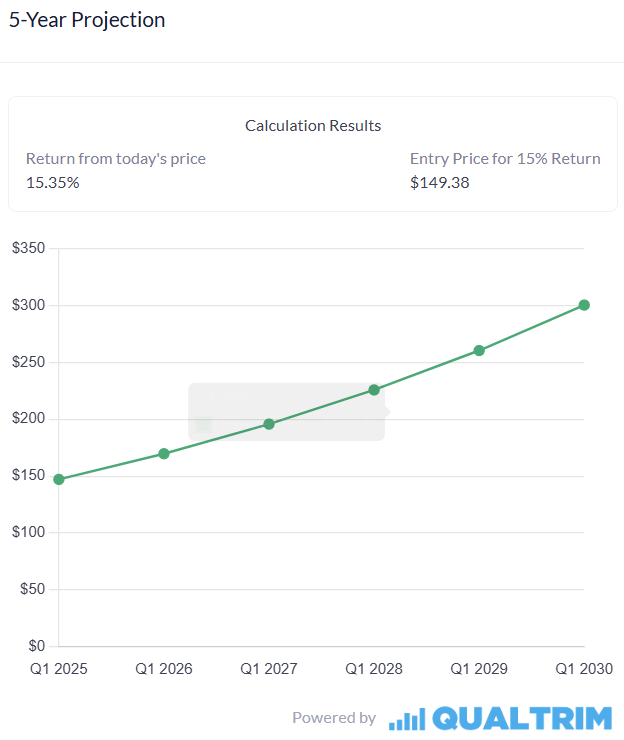

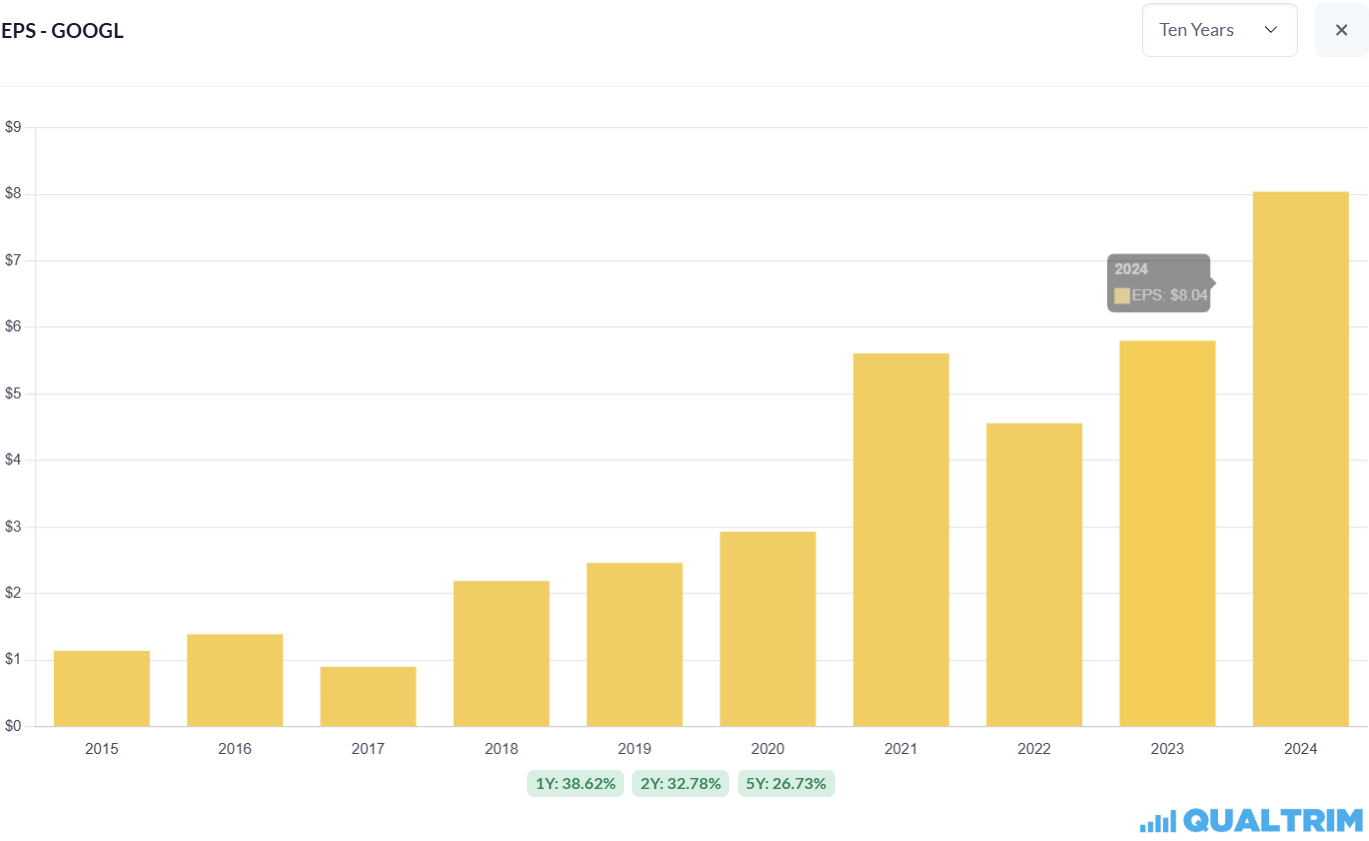

Let’s make a few long-term conservative assumptions. Assuming TTM EPS of $8.05, a 5-year EPS CAGR of 20%, and a forward P/E multiple of 15x during the next 5 years (below today’s 18x), you could expect a 15% annual return over the next five years.

And these aren’t overly optimistic numbers. Alphabet has grown EPS at 25%+ annually over the last 1, 2, and 5 years, impressive consistency for a tech giant defending its dominance in Search since the early 2020s.

Here’s the problem: while Alphabet talks a big game on AI, its product traction isn’t quite keeping pace with the hype.

Despite Google’s infrastructure, distribution, and brand power, Gemini remains far behind OpenAI’s ChatGPT in adoption.

And here's a fun twist: Alphabet is facing increased regulatory scrutiny in the U.S., U.K., and Europe for its Search and advertising dominance. But calling Google a “monopoly” in 2025 seems increasingly outdated.

Today’s competition includes ChatGPT, Grok, Perplexity, Amazon, Meta, Microsoft Copilot, TikTok, Reddit, and many more.

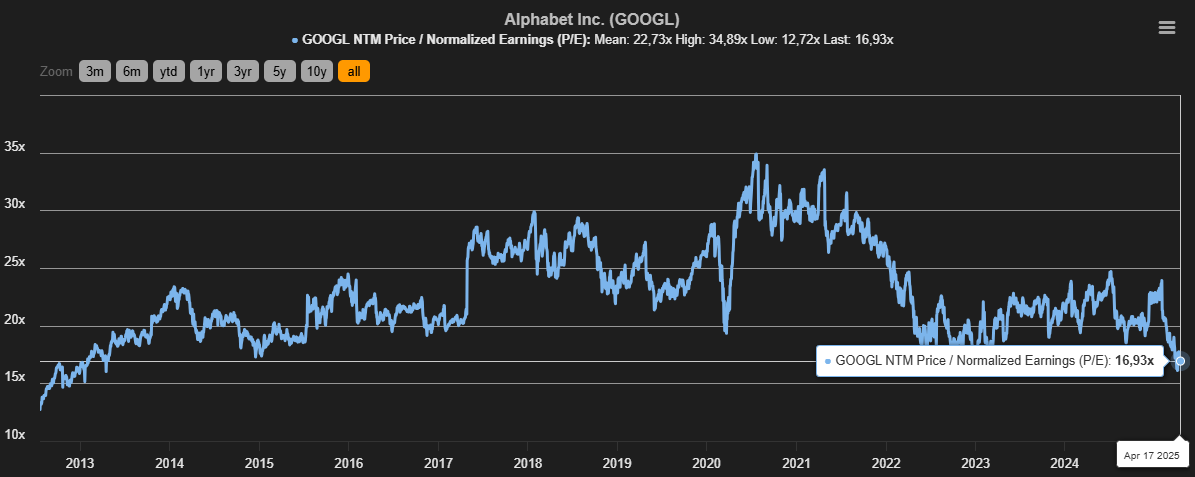

That brings us valuation in its historical lows:

Why? Because for the first time in two decades, its core product is being seriously disrupted.

What’s interesting is that Google is starting to "Appleize", not always being first, but releasing polished, deeply integrated, and user-friendly products.

A great next step? Improving Gemini’s integration into Chrome, Android, and Workspace, turning it from a sidekick into a default experience.

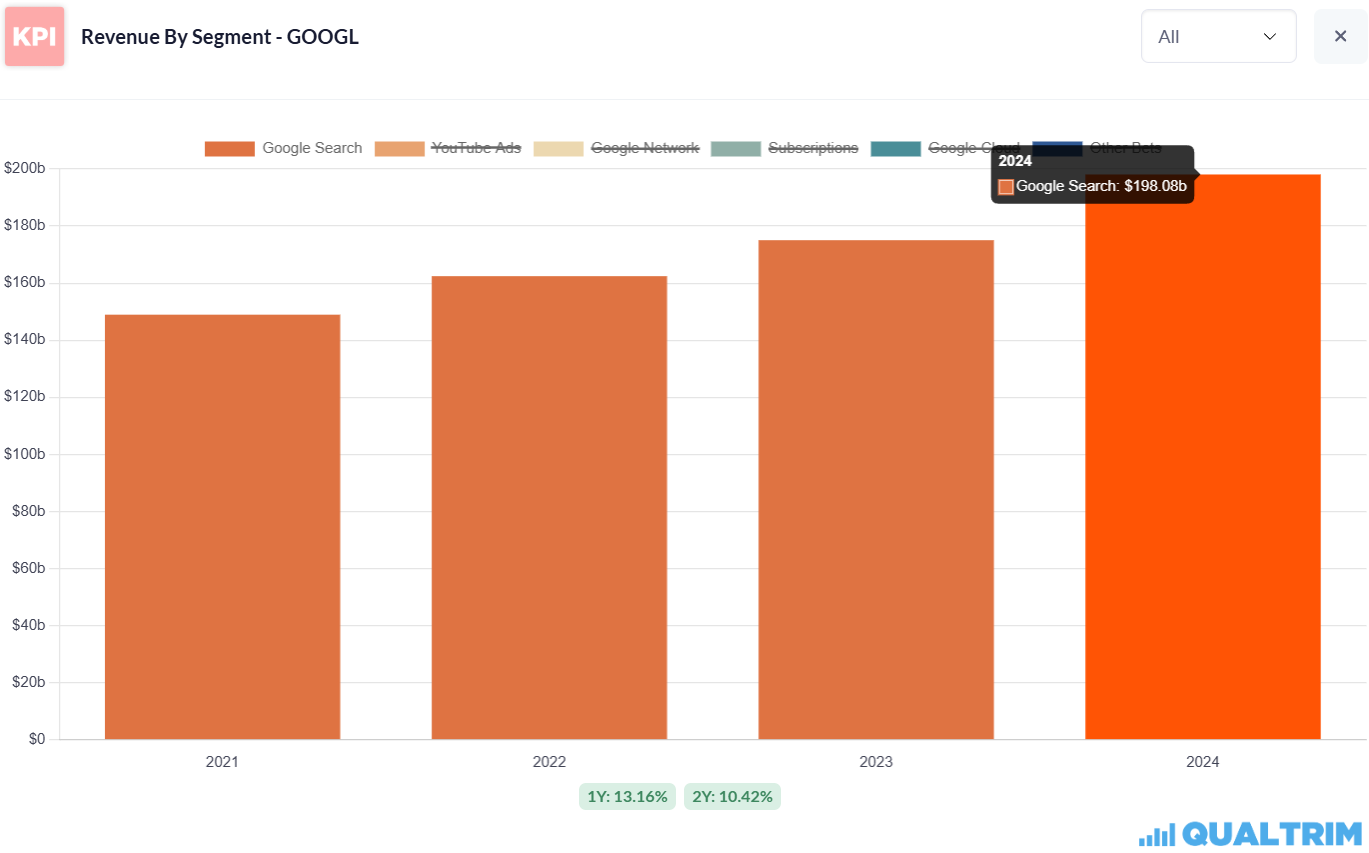

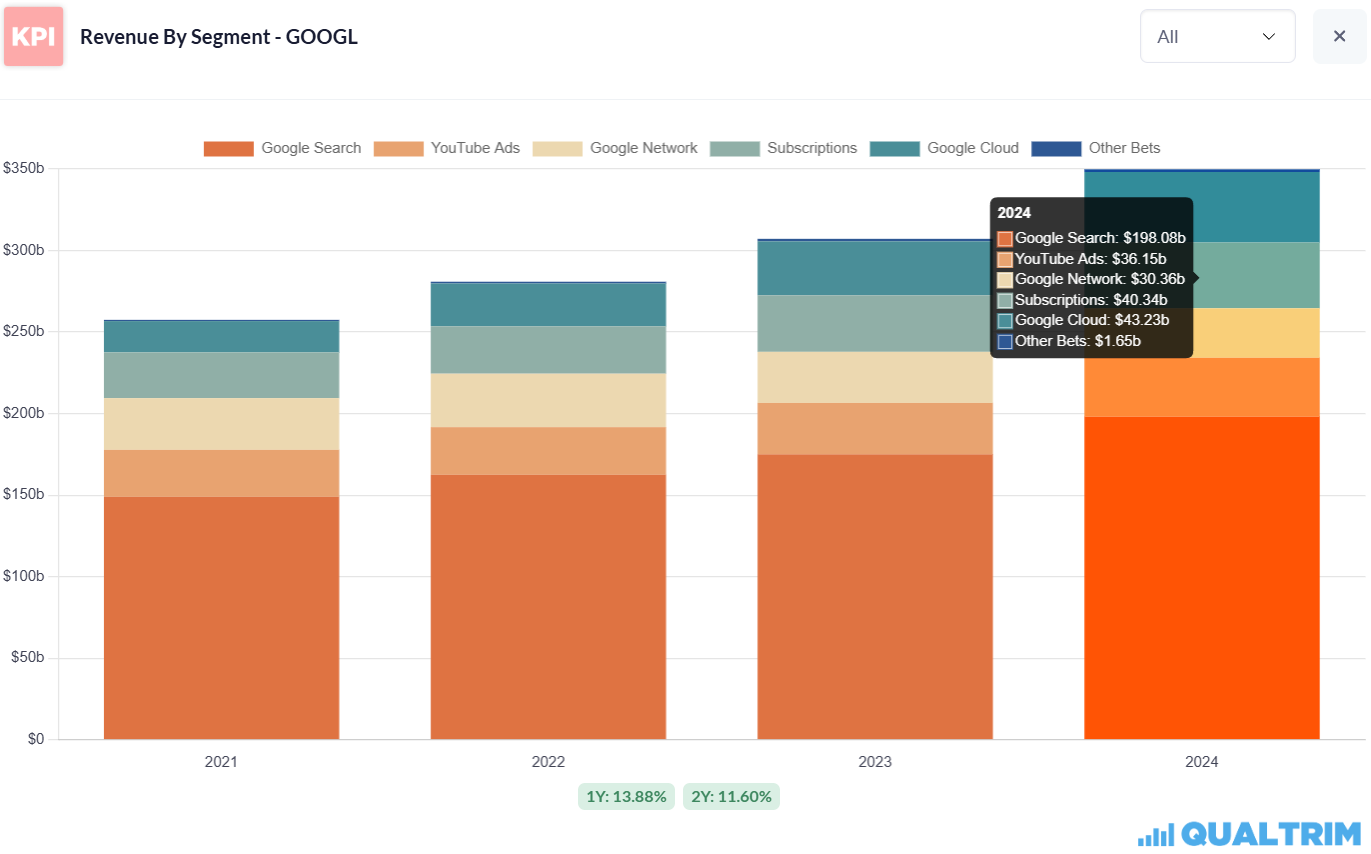

Even amidst this disruption, Google Search still grew 13% last year, proving the business isn’t crumbling, it’s evolving:

And other segments are accelerating too:

Specially in Cloud:

Which continues to post solid growth with improving margins, inching closer to AWS and Azure in both scale and profitability. But the real story lies in strategic execution, and the recent acquisition of Wiz is a great example.

Wiz, one of the fastest-growing cloud security startups, gives Google a major edge in cloud-native security, a critical area for enterprise clients adopting multi-cloud and AI infrastructure. This smart move positions Google Cloud as not just a hyperscaler, but a trusted enterprise platform for AI + cybersecurity, two of the biggest TAMs (Total Addressable Markets) of the next decade.

Finally, all of these concerns surrounding Google place enormous pressure on Sundar Pichai’s leadership. While there’s plenty of debate over whether he’s the "best" CEO, one thing is clear: he has done a remarkable job steering the company through a complex environment.

Much like Zuckerberg did in 2022 when he pivoted Meta’s narrative away from the Metaverse, a similar shift could happen at Google, and signs of increased discipline are already visible. Since 2023, the company has made notable improvements in efficiency, particularly with stock-based compensation (SBC) and broader cost controls.

Alphabet holds massive cash reserves, which it is channeling into future growth:

and historically, this capital has delivered strong returns on capital employed (ROCE):

While share repurchases aren’t our preferred use of capital at these ROCE levels, it’s still a form of value return for shareholders in the meantime.

All that said, it wouldn’t be surprising to see Warren Buffett eyeing another “Apple moment” with Google. While the comparison isn’t perfect, Alphabet faces unique challenges in its core advertising business, ongoing regulatory scrutiny, and the need to diversify its revenue streams, the potential is clear.

If Google continues to advance in AI, sustain the momentum in its Cloud division, and gradually build stronger brand affinity across its ecosystem, we could see a period of significant outperformance, one that prompts the market to re-evaluate its current valuation.

Whether Alphabet reaches its own version of an "Apple moment" will ultimately depend on its ability to:

Navigate the regulatory landscape

Monetize AI at scale

Maintain Cloud growth

And expand user engagement across multiple verticals

It’s a story still very much in progress. Bill Ackman is already on board, and it will be interesting to hear his perspective as the narrative evolves.

Despite the noise, we have strong conviction in Google’s ability to be a long-term winner. The current sell-off, paired with compelling metrics and a historically low valuation, presents a strong case for outperformance over the next 5 to 10 years, especially in an uncertain world where resilience and optionality matter more than ever.

(And all that without considering its Other bets):

(Not financial advice, of course — just a quiet thought).