50%+ Margins with 58% Segment Growth and Record Cash Flows - Lam Research Corporation

Deep Dive into the Undisputed Leader in Etch & Deposition, Capitalizing on the AI Boom with an Expanding Market Share and a Powerful Recurring Revenue Flywheel.

If you only look at the finished product, you’ll never understand the machine that built it.

Great investors, like great engineers, know that true insight lies not on the surface, but deep within the process. You can admire a skyscraper, but the real genius is in the cranes, the tools, and the architectural blueprints that made it possible. This is the difference between being a spectator and being a strategist.

The lesson is inescapable: to master an industry, you must master its means of production.

Nowhere is this more critical than in semiconductors. This sector isn’t just about the chips in your phone; it is the physical substrate of the digital universe. Its fabrication plants are the most complex factories ever built by humankind, operating at a scale that defies imagination. To understand the future of AI, data centers, and global technology, you must first understand the companies that build the tools that build the chips.

This is why, for the first time, we are collaborating with The Small Cap Strategist for a special four-part series. Over the next four weeks, we will deconstruct one of the most important, yet underappreciated, pillars of the entire tech ecosystem.

While we typically focus on small caps, understanding Lam Research isn’t a detour; it’s a prerequisite. It is the keystone species in the technology jungle. Ignoring it is the difference between seeing the world in high resolution versus living in the blur.

In this deep dive, you’ll find:

The "Complexity is Cash Flow" Moat: Why Lam’s dominance in etch and deposition becomes more critical as chips evolve into 3D skyscrapers, turning technological difficulty into financial strength.

Riding the AI Tsunami: How Lam's technology is an indispensable enabler for the next generation of AI processors, high-bandwidth memory (HBM), and advanced packaging techniques that power the AI revolution.

A Valuation Deep Dive: A complete analysis of Lam's valuation against key peers like ASML and Applied Materials, assessing whether the market is fairly pricing its renewed growth and expanding margins.

The Geopolitical Chessboard: A breakdown of the immense China paradox—currently 35% of revenue, and a rigorous look at the primary risks, including cyclical downturns and escalating trade tensions.

A Look Inside the Machine: A comprehensive overview of Lam's strategy to win critical technology shifts, its veteran management team, and the operational engine that powers the world's most advanced fabs.

To give you a sharper collateral on a sector entirely dependent on semiconductors, we’ve published one of the most in-depth free deep dives on Generative AI you’ll find online, a real blueprint for where the industry is heading:

Stay posted with us for the full four-part series. This is more than an analysis; it's a masterclass in the foundational industry of our time.

At Swiss Portfolio, we’ve made it our mission to uncover hidden opportunities before the crowd. In recent months, we’ve published over a dozen sector deep-dives, including:

Our research community is built for investors who want an edge:

Institutional-grade analysis usually locked behind paywalls.

Unrivaled diligence, creative, painstaking work others avoid.

A proven record of identifying global compounders that consistently beat the market.

This isn’t just research, it’s a blueprint for compounding wealth with conviction.

If you want to understand not only where technology is headed, but also how to capture the hidden compounding opportunities that enable it, subscribe to Swiss Transparent Portfolio and The Small Cap Strategist.

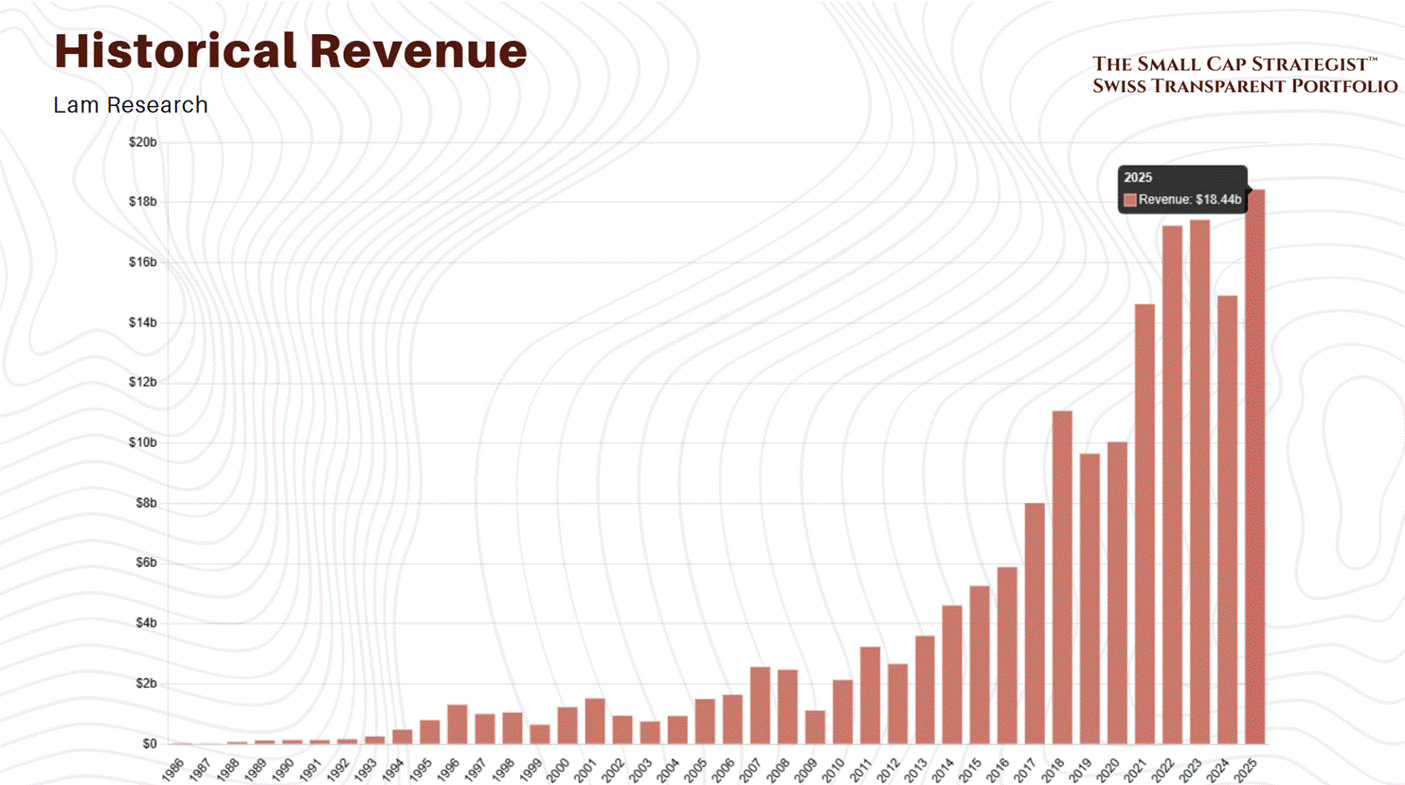

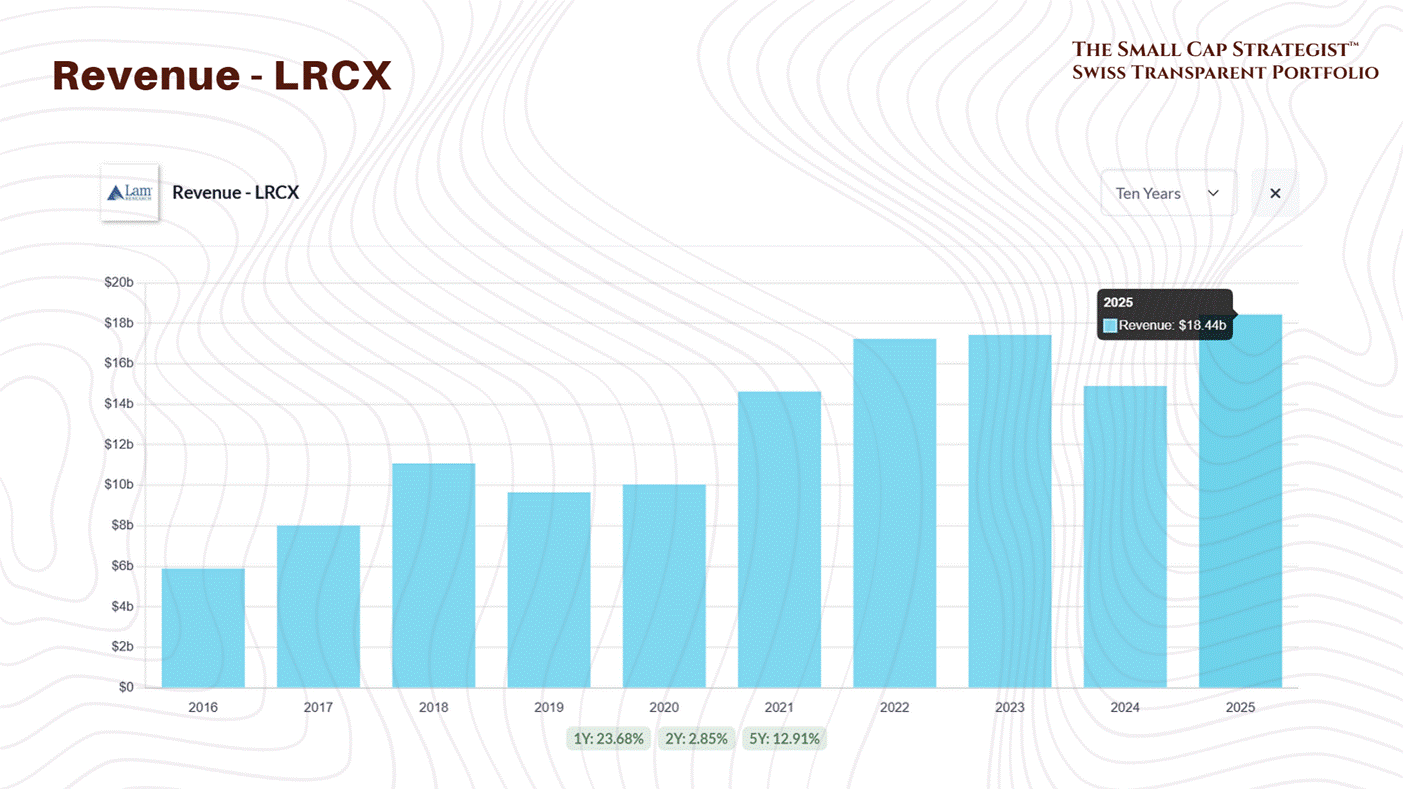

Record-Breaking FY2025 Comeback

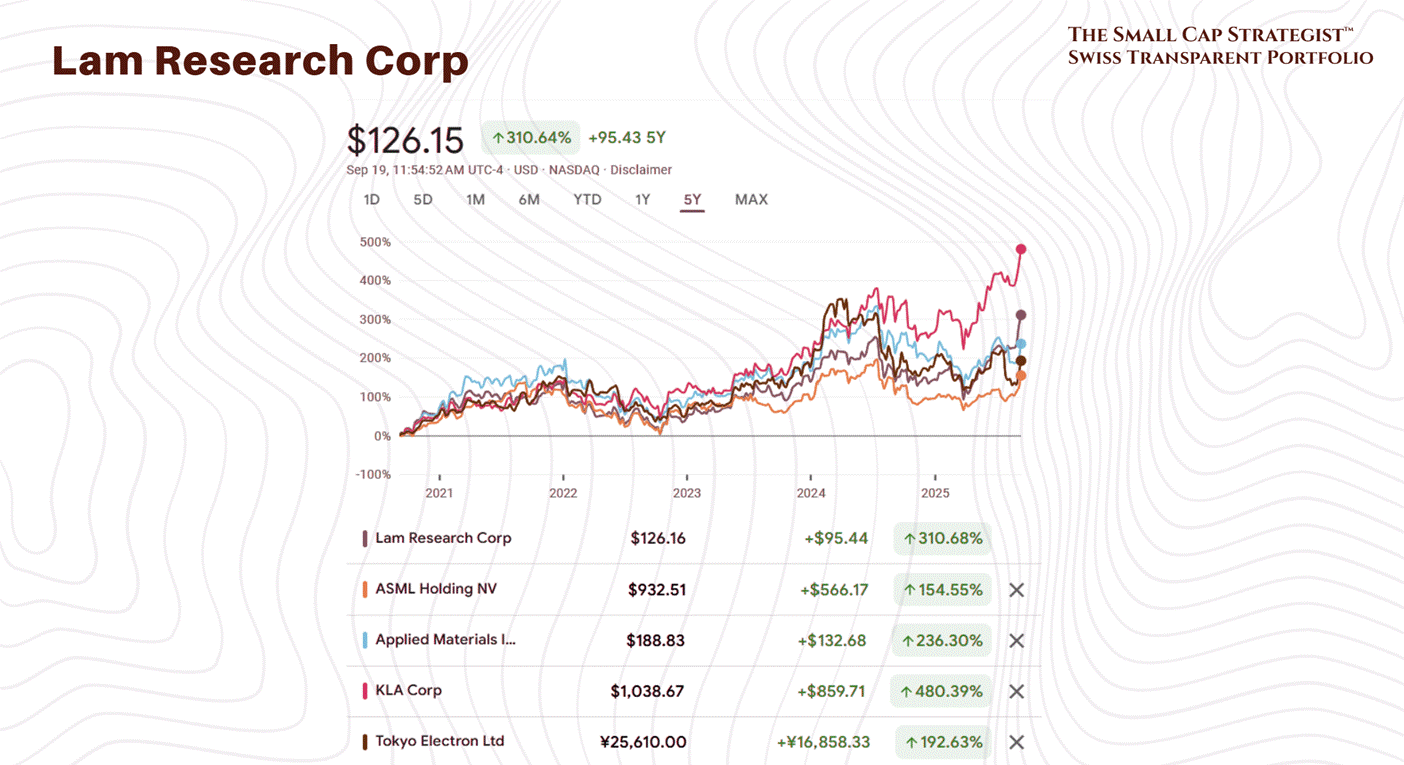

Lam Research has snapped back from the downturn: revenue grew 23.7% in FY2025 to $18.44B after a 14% decline in 2024.

The June 2025 quarter set records, revenue +33.6% YoY, gross margin >50%, underscoring how quickly industry leaders reassert earnings power when the cycle turns. The share price has recovered from ~$56 (52-week low, post-split) to ~$100, yet the valuation remains reasonable against renewed growth and expanding margins.

The market’s stance is cautious, not euphoric, a nod to prior boom-busts.

The question isn’t whether Lam is essential to advanced semiconductor manufacturing, (it is), but whether today’s price fairly discounts the next phase of AI-driven wafer-fab investment versus the risk of another air-pocket in capex. Let’s test that trade-off, data and facts first, no cheerleading, before we decide if $LRCX earns a place in a long-term portfolio.

Business Segments

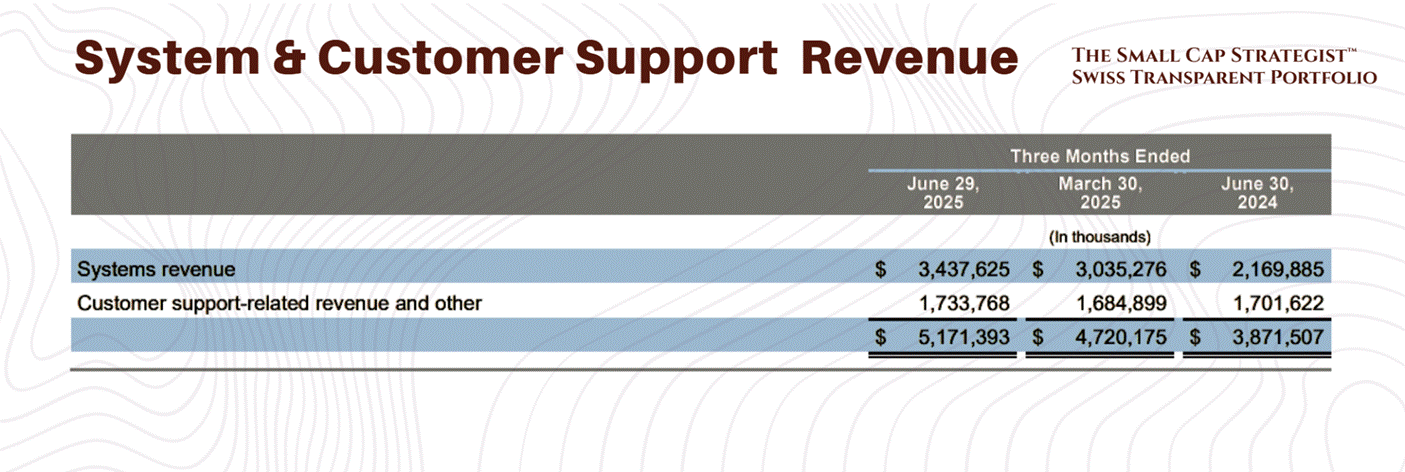

Lam’s business spans two main segments: (1) Systems, sales of new wafer fabrication equipment (primarily etch and deposition tools for chipmakers), and (2) Customer Support, services, spare parts, and equipment upgrades (Lam’s Reliant® product line covers legacy nodes). In the latest quarter, systems revenue was roughly $3.44 billion and services/others about $1.73 billion, together totaling $5.17 billion. Notably, system sales are rebounding strongly, up 58% year-on-year in Q2, as chipmakers ramp capital spending again.

Meanwhile, the support business has been a steady workhorse, growing to a quarterly record (around $1.73 billion in Q2) thanks to the expanding installed base. This mix provides a nice balance: volatile big-ticket equipment sales when the cycle is hot, and a buffer of recurring revenue from servicing all the machines out in the field.

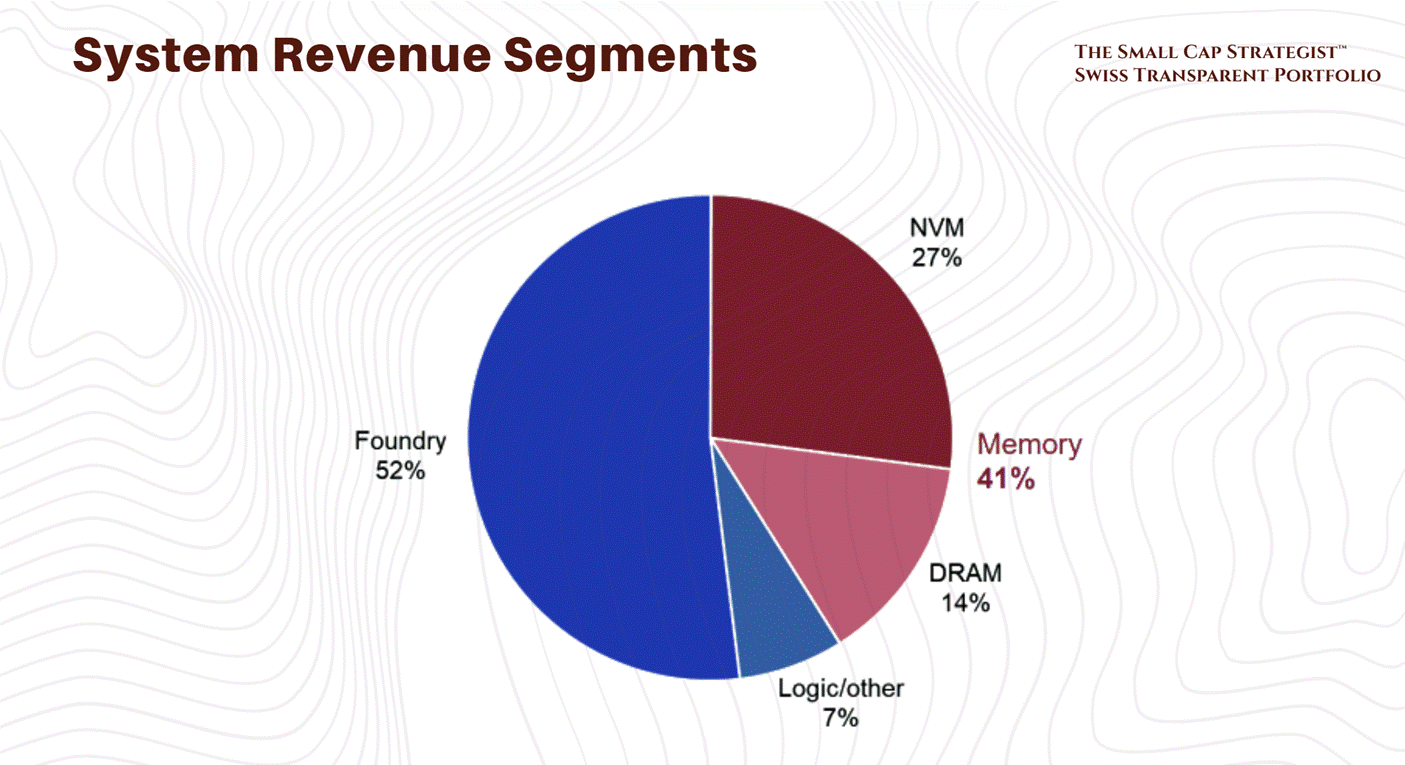

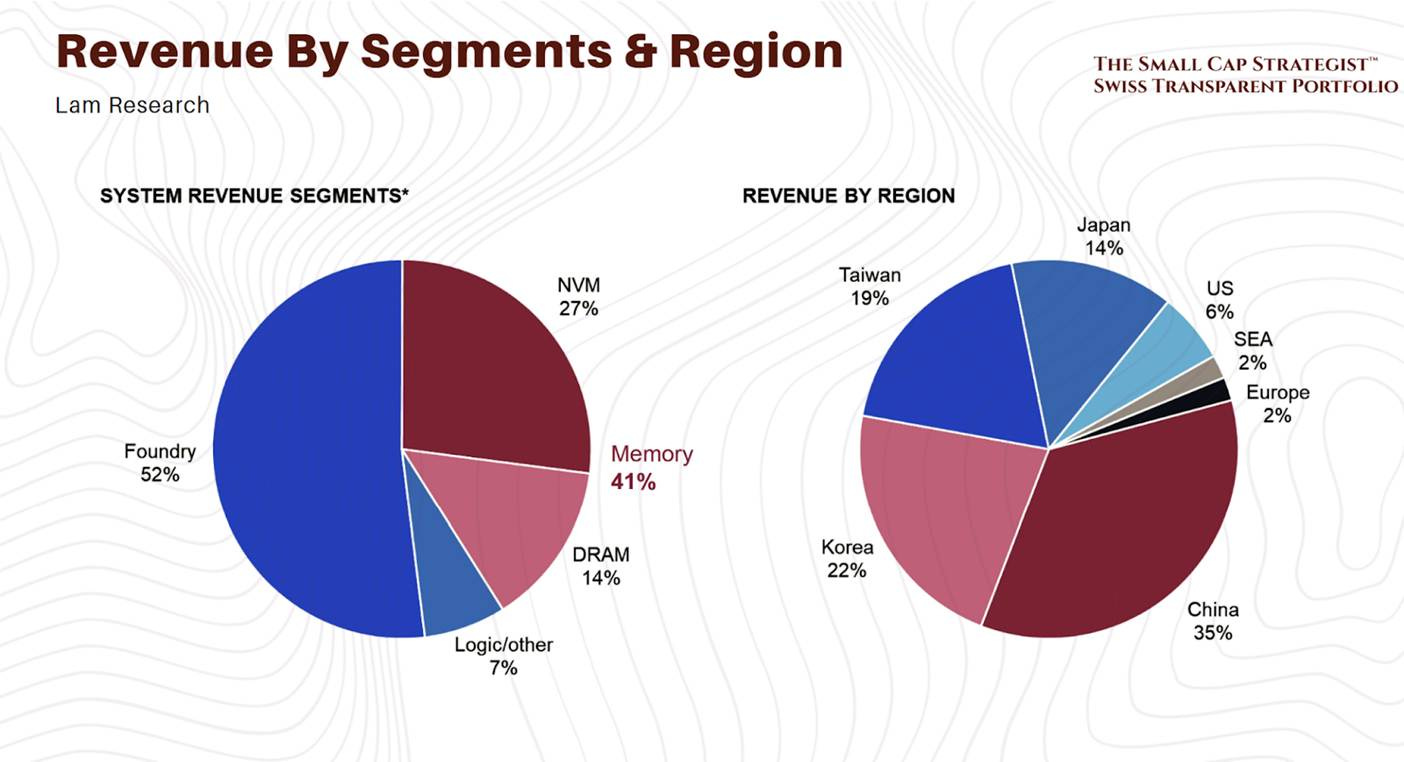

Foundry/Logic vs Memory: Within system sales, Lam enjoys a broad customer base across semiconductor markets. In the June quarter, about 52% of system revenue came from foundry customers (e.g. TSMC and other logic chip manufacturers), 41% from memory makers (NAND flash and DRAM combined), and the rest ~7% from logic/other categories. This is a critical point. Lam isn’t a one-trick pony tied only to memory.

In fact, during the recent downturn, it was the slump in memory capex that hurt 2024’s results, and now the memory rebound (especially NAND) is driving a big part of 2025’s surge. Going into late 2025 and 2026, the outlook by segment is mixed but generally positive: foundry/logic spend is expected to remain healthy as leading foundries invest in next-gen nodes (to support AI, 5G, and high-performance computing chips), while memory spend is in early recovery after a severe pullback, as memory prices stabilize, makers of DRAM and NAND are cautiously adding capacity for new technologies (like higher-layer 3D NAND and EUV-driven DRAM).

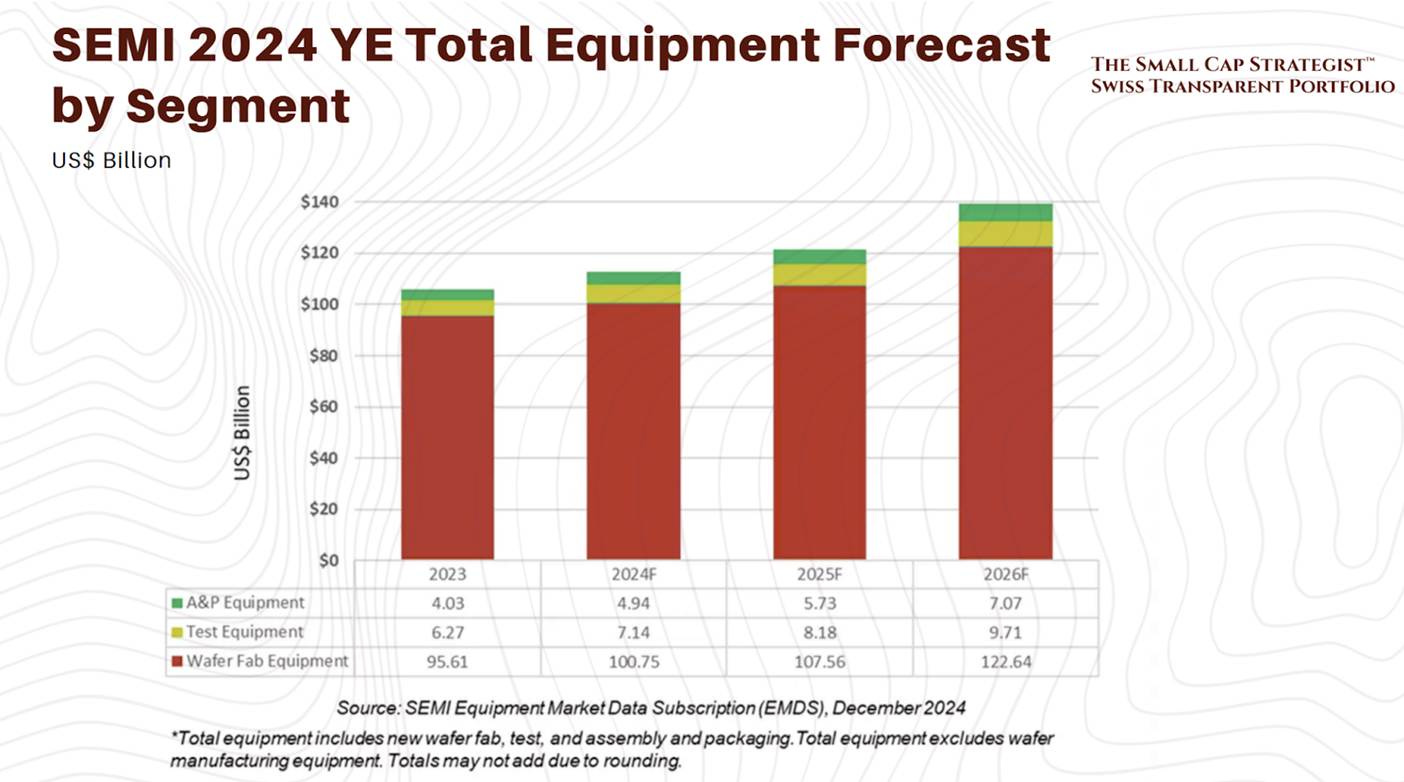

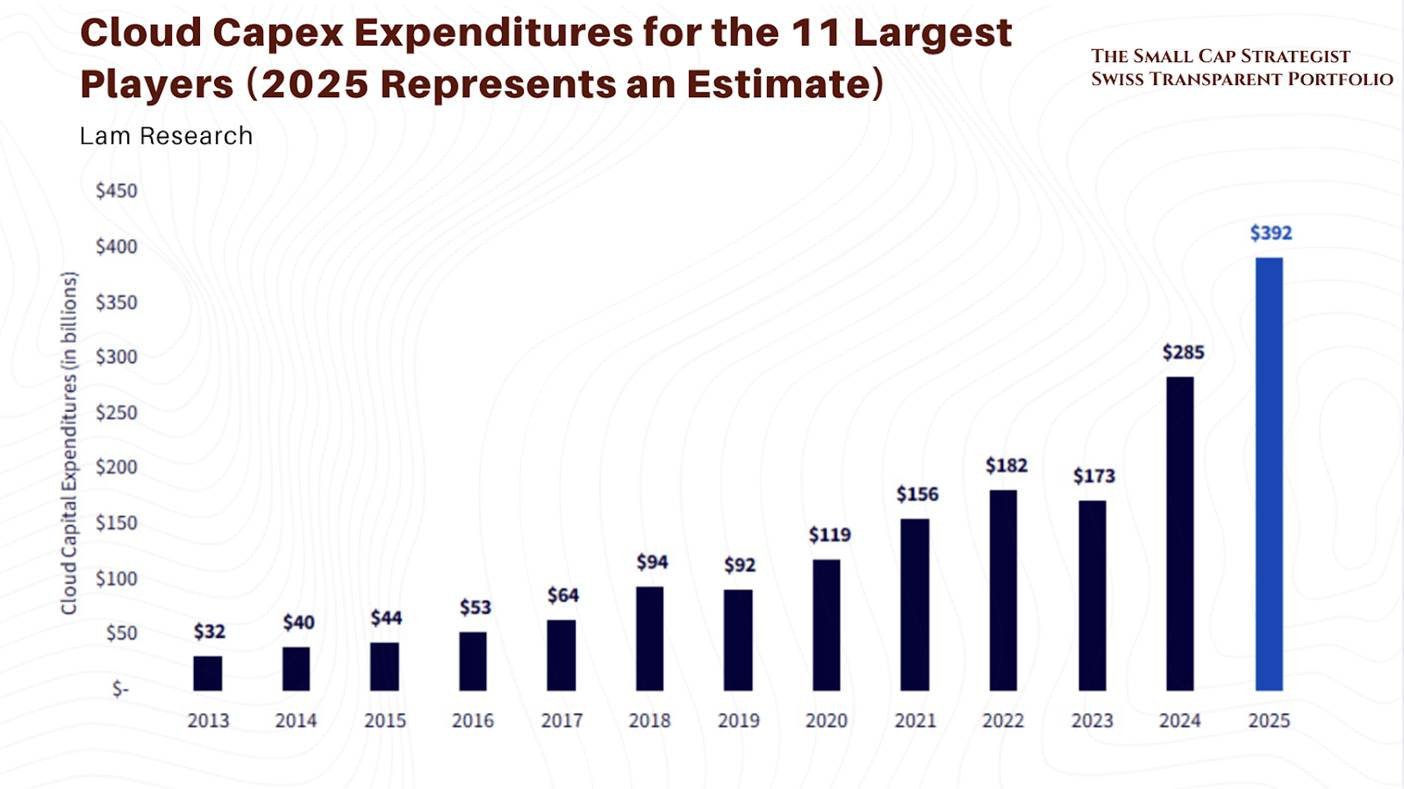

The macro question is whether this upcycle has legs: Lam’s management raised its 2025 wafer fab equipment (WFE) outlook to ~$105 billion (from ~$100B) amid improving demand, and noted that H2 2025 is pacing flat-to-slightly up versus H1, a sign that the recovery has been underway all year. It’s “too early to comment on 2026” in detail, according to Lam’s CEO, but the company positions itself for continued growth, assuming deposition and etch needs will only intensify. In other words, barring a macro-economic hiccup, 2026 could see further WFE expansion (or at least sustain 2025’s high level) driven by new chip technology transitions.

Services (Customer Support) Momentum: Lam’s Customer Support Business Group (CSBG), which handles after-market sales, spare parts, and tool upgrades, contributes roughly one-third of total revenue. This business has been growing steadily even during cyclical dips, as more machines in the field (Lam has thousands of tools at customer fabs worldwide) lead to more service contracts and replacement parts sales.

In Q2, services revenue hit $1.73B, up from $1.68B in the prior quarter and slightly above the year-ago level, indicating resilience. This segment’s outlook is solid: as long as Lam keeps selling new tools, the installed base (and thus service demand) increases. For the rest of 2025 and into 2026, we can expect CSBG to continue growing at a stable clip (high single-digit % annually, historically), providing a nice cushion of recurring revenue if new equipment orders wobble.

Lam’s H1 2025 performance shows: new equipment sales booming again with the industry upcycle, and services reaching new highs. If the macro environment remains constructive (global GDP avoiding recession) and tech investment stays strong (AI server build-outs, 5G infrastructure, etc.), Lam’s business segments are set to finish 2025 robustly. There is upside into 2026 from continued memory recovery (memory spending is still below prior peak levels) and the onset of mega-projects like U.S. and European fab expansions (spurred by government CHIPS Act incentives, albeit those will ramp slowly).

The downside scenario would be if demand for electronics falters or inventories bloat, prompting chipmakers to once again slash capex, a cycle turn that would hit Lam’s systems orders quickly. For now, though, the near-term trajectory is positive, with Lam’s broad segment exposure allowing it to capture growth wherever it appears in the chip world.

Growth Drivers

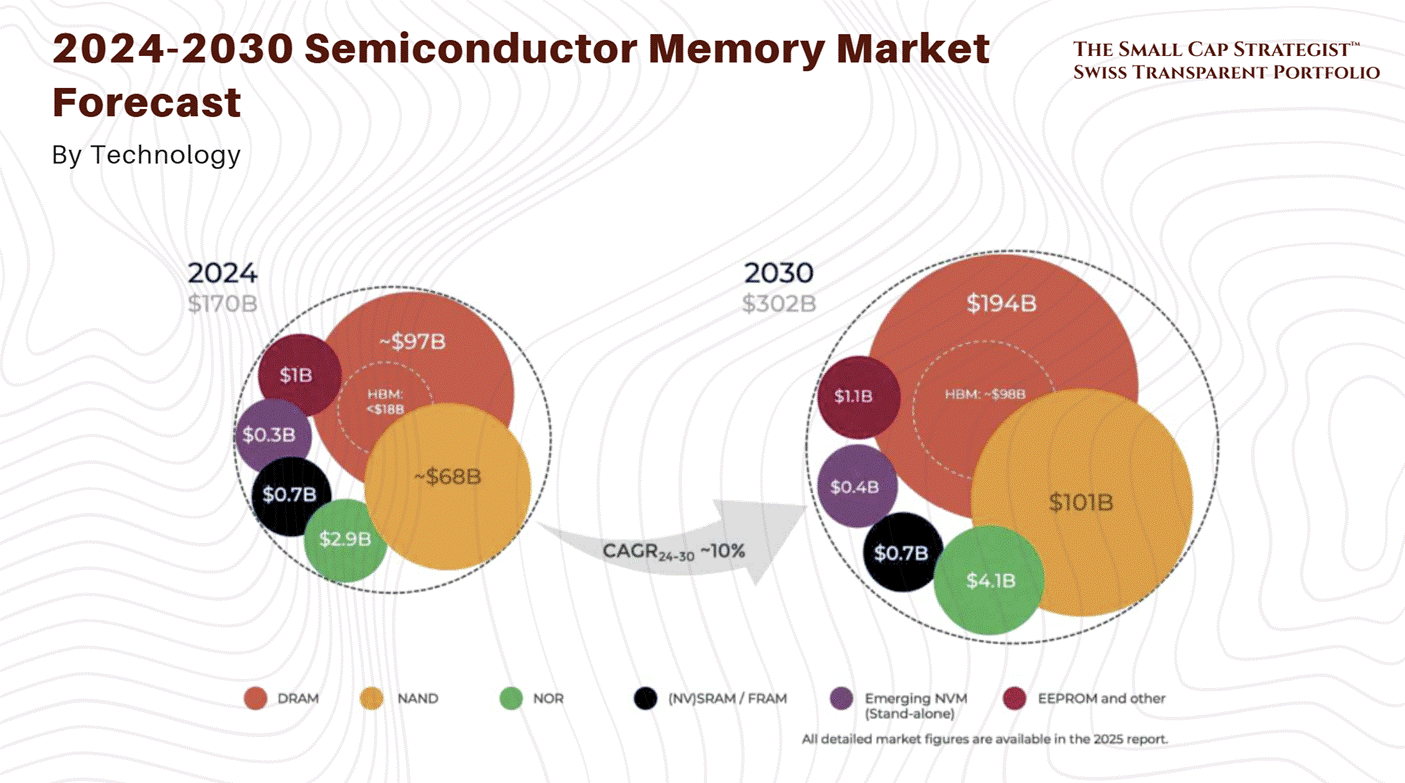

What’s powering Lam’s growth spurt, and more importantly, can it continue? The key drivers are rooted in technological sea changes that play directly into Lam’s strengths in deposition and etch. We’re essentially in an “Age of AI and High-Performance Computing”, a new wave of demand for advanced chips that require more complex manufacturing processes. Lam’s management emphasizes that in this AI era, deposition and etch steps are becoming even more critical (and numerous) in chip production. Let’s break down the growth catalysts:

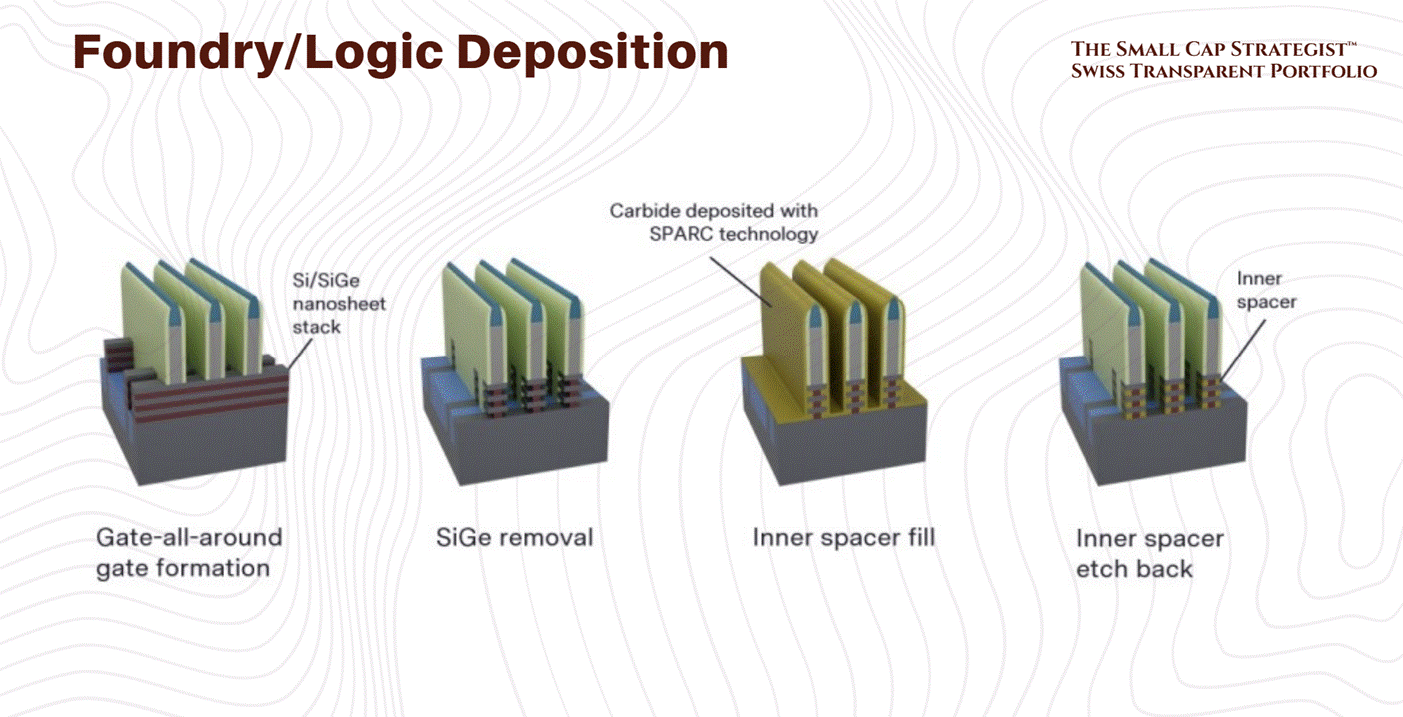

Explosion of AI and Data Center Chips: The rise of generative AI, machine learning, and big data is driving massive investment in cutting-edge logic chips (GPUs, AI accelerators, advanced CPUs). These chips are at the most advanced nodes (5nm, 3nm and moving toward 2nm), which involve new structures like Gate-All-Around (GAA) transistors. GAA and other next-gen transistor designs demand more deposition/etch steps (e.g. nanosheet layering, new materials deposition, etc.).

Lam is front-and-center here, it noted that AI-related performance requirements are accelerating the inflection to GAA, which in turn triples the metallization steps per wafer (a boon for Lam’s deposition tools). In 2025, Lam’s served available market is expanding to the mid-30s% of total WFE as these trends unfold. In plain English: as chip designs get more complex, Lam can sell more equipment per wafer fabricated.

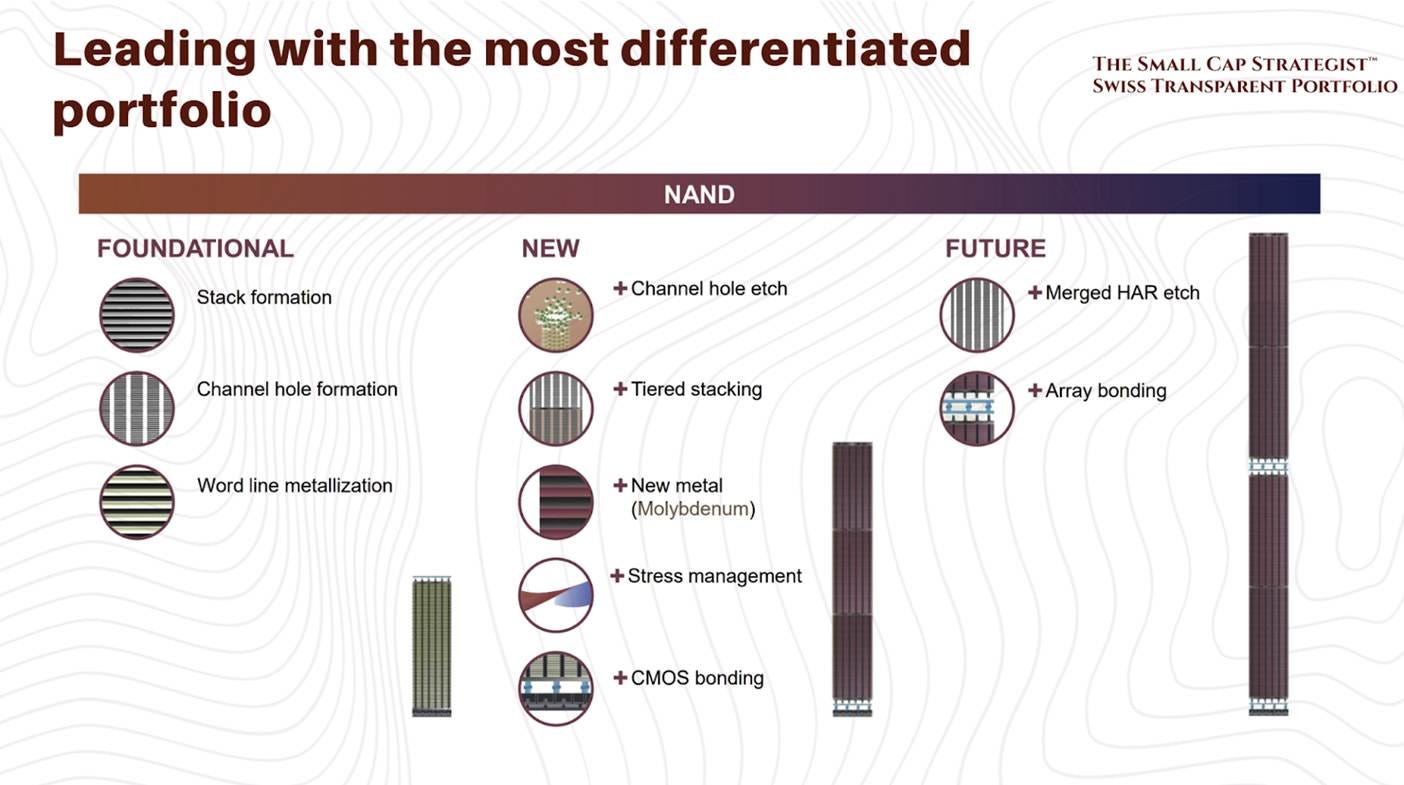

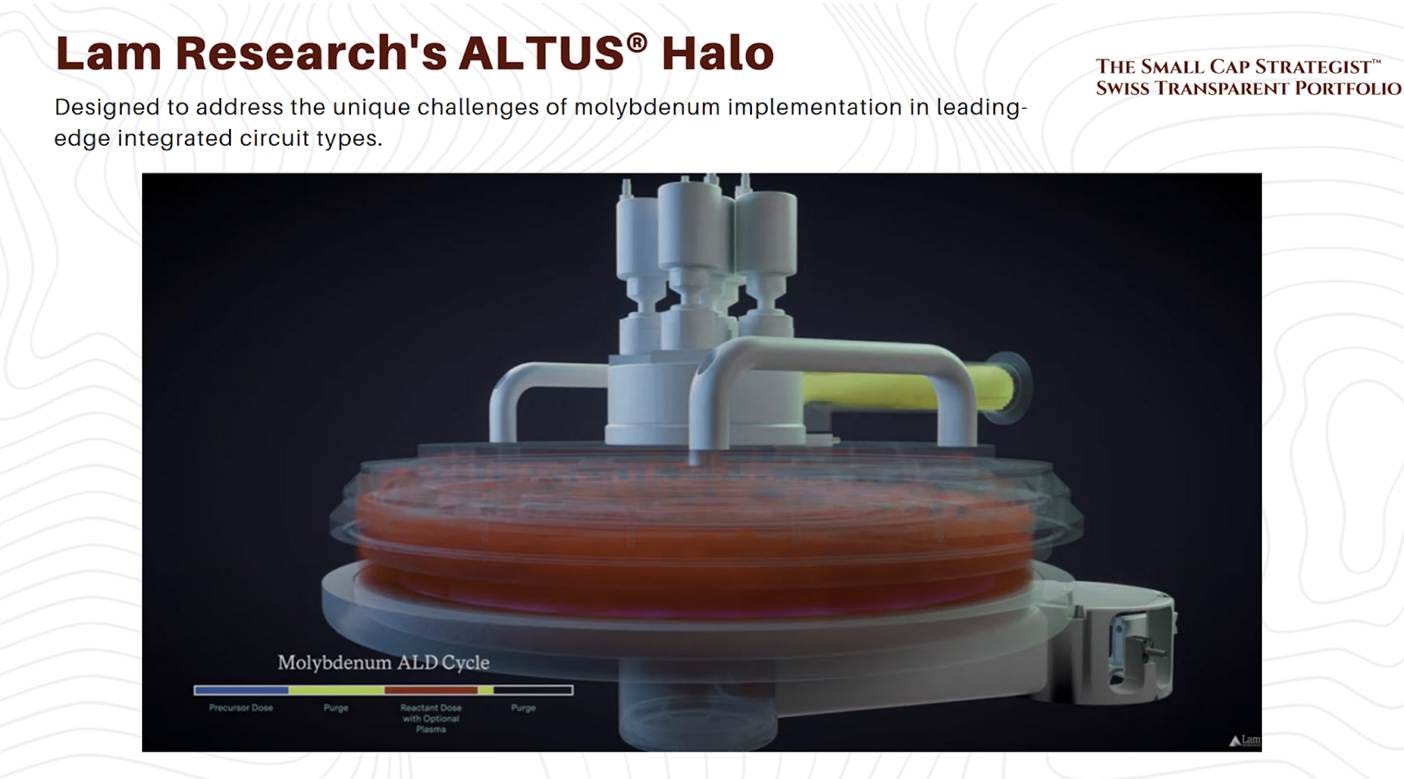

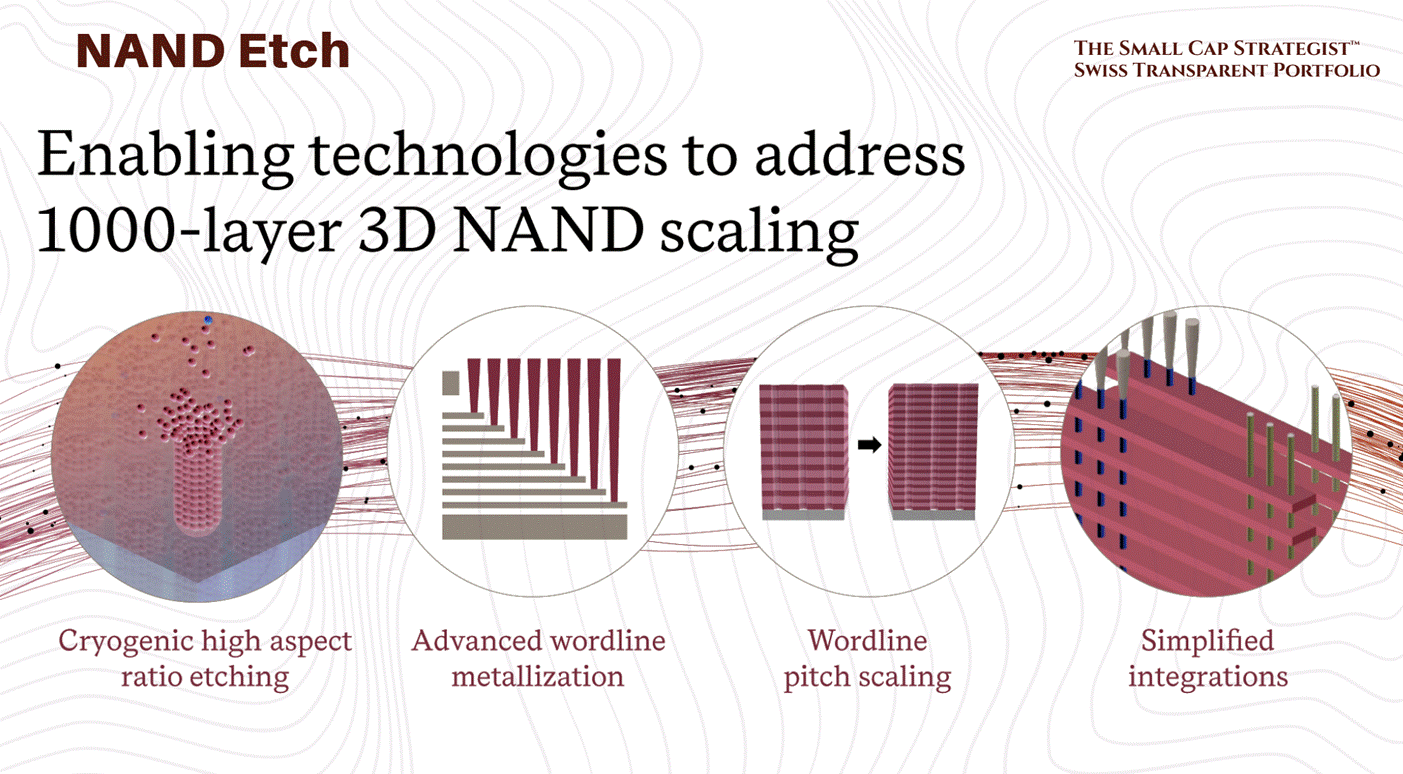

Memory Technology Transitions: On the memory side, 3D NAND flash is a huge driver. NAND manufacturers are racing to increase the number of layers in their chips (moving from ~200 layers toward 300+ in coming years). More layers = more etch and deposition needed to construct those towering structures. Lam has specifically highlighted the adoption of its new ALTUS® Atomic Layer Deposition (ALD) systems for depositing molybdenum (Mo) in 3D NAND devices. This technology, ramping at multiple NAND customers now, enables chips with 200+ layers by providing high-quality, precise metal deposition. As NAND makers convert fabs to higher layers, Lam stands to ship a lot of these tools.

DRAM (the other memory type) is also evolving, manufacturers are starting to use EUV lithography and new materials, which drive demand for advanced etch tools. Lam’s Vantex etch system with cryogenic tech for high-aspect-ratio etching in NAND, and its new Akara conductor etch for DRAM, have scored multiple wins at memory customers. With memory capital spending expected to rebound off 2024 lows, Lam’s cutting-edge offerings position it to capture outsized share of that recovery.

Advanced Packaging & Chiplet Architecture: It’s not just about making individual chips; it’s also about packaging them in new ways (think of how Apple or AMD are now using chiplets and 3D stacking to boost performance). Lam is seizing this trend via its specialty in plating technology.

The company’s SABRE® 3D electroplating tools are crucial for advanced packaging (like filling copper interconnects in chiplet architectures). Lam proudly announced it has 6,000 installed plating cells, the largest base in the industry. With the surge in AI, there’s a need for advanced packaging to integrate HBM memory stacks with processors. Lam expects its market share in advanced packaging to jump ~5 percentage points in 2025 thanks to these solutions. As the industry adopts 3D integration and heterogeneous integration (mixing chips in a package), Lam’s revenue from packaging equipment could climb substantially.

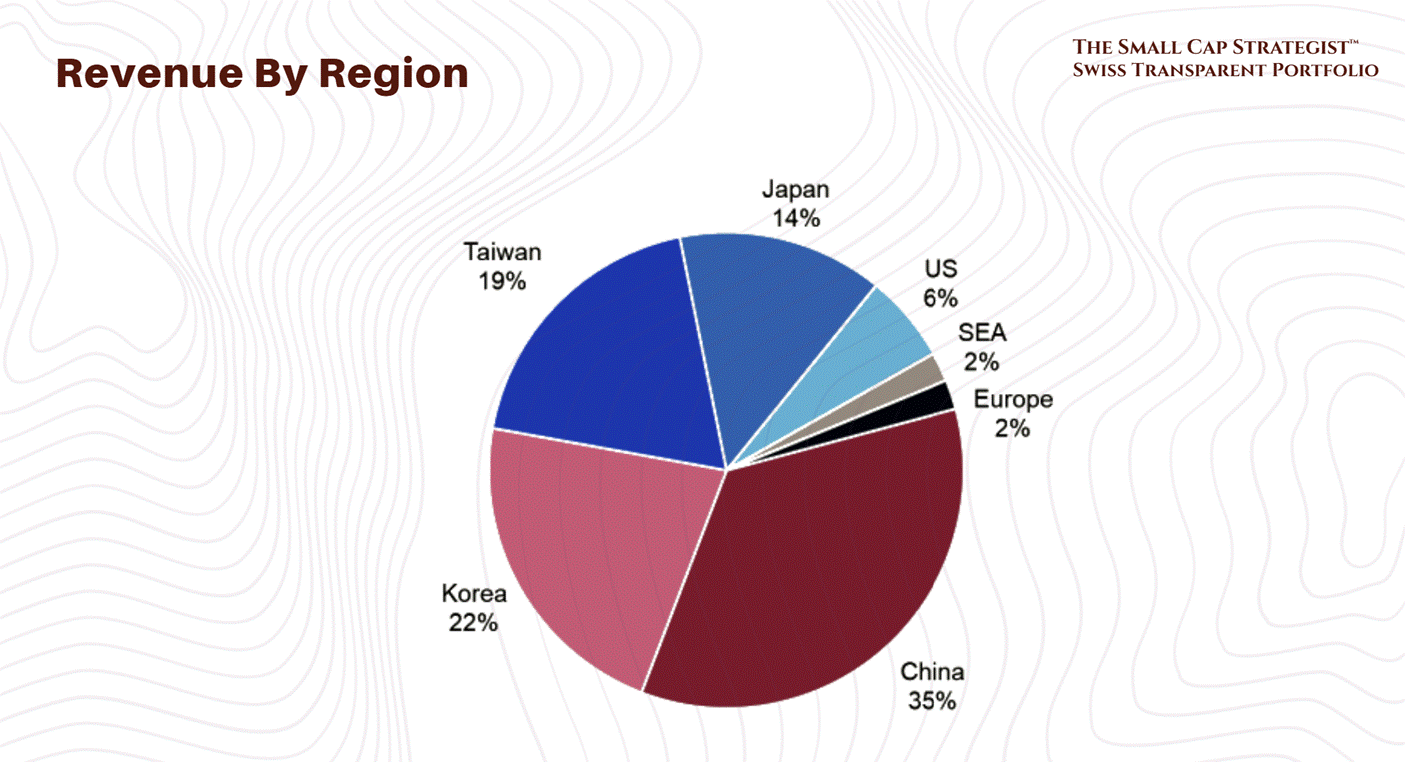

Geopolitical and Domestic Capacity Build-out: Another growth driver, albeit an indirect one, is the geopolitical push for semiconductor self-sufficiency. Restrictions on China have paradoxically led to a surge in domestic Chinese fab investments, as local players rush to build capacity with whatever tools they can still purchase. Lam noted an “uptick in domestic China spending” in 2025 which helped bump WFE higher. China accounted for 35% of Lam’s revenue last quarter, reflecting how crucial that market is. While export controls limit sales of the most advanced tools, Lam still sells a lot of equipment for slightly older nodes and memory to Chinese companies.

Going forward, continued investment in China (assuming regulations don’t tighten drastically) is a driver. Simultaneously, U.S. and Europe are incentivizing new fabs (Intel in the US, TSMC in Arizona, etc.), these projects are slow burners, but as they ramp construction in 2024-2026, they will contribute to tool demand that benefits Lam. Government-driven fab expansions provide a floor under equipment demand that didn’t exist in past cycles.

All these drivers point to a common theme: rising complexity = more tools needed. Lam’s CEO summed it up well:

“With deposition and etch criticality intensifying in the AI era, we are executing on our long-term strategic initiatives and leveraging our differentiated product portfolio to position Lam for outperformance”.

In practical terms, Lam is growing not just because the semiconductor cycle turned up, but because it’s at the nexus of multiple secular trends (AI, 5G, IoT, automotive, cloud) that require more silicon and more advanced silicon. Its R&D investments (>$2B annually) are laser-focused on these inflections, and we’re seeing the pay-off in new product wins and share gains.

The big question: can these growth drivers overcome the inevitable cyclical pauses? In the long run, industry demand for computation is only headed upward, though likely in spurts. For now, the secular tailwinds (AI, cloud, connectivity) are aligning beautifully with Lam’s offerings, which is a key reason the company is outgrowing many peers in 2025.

Valuation and Peer Comparisons

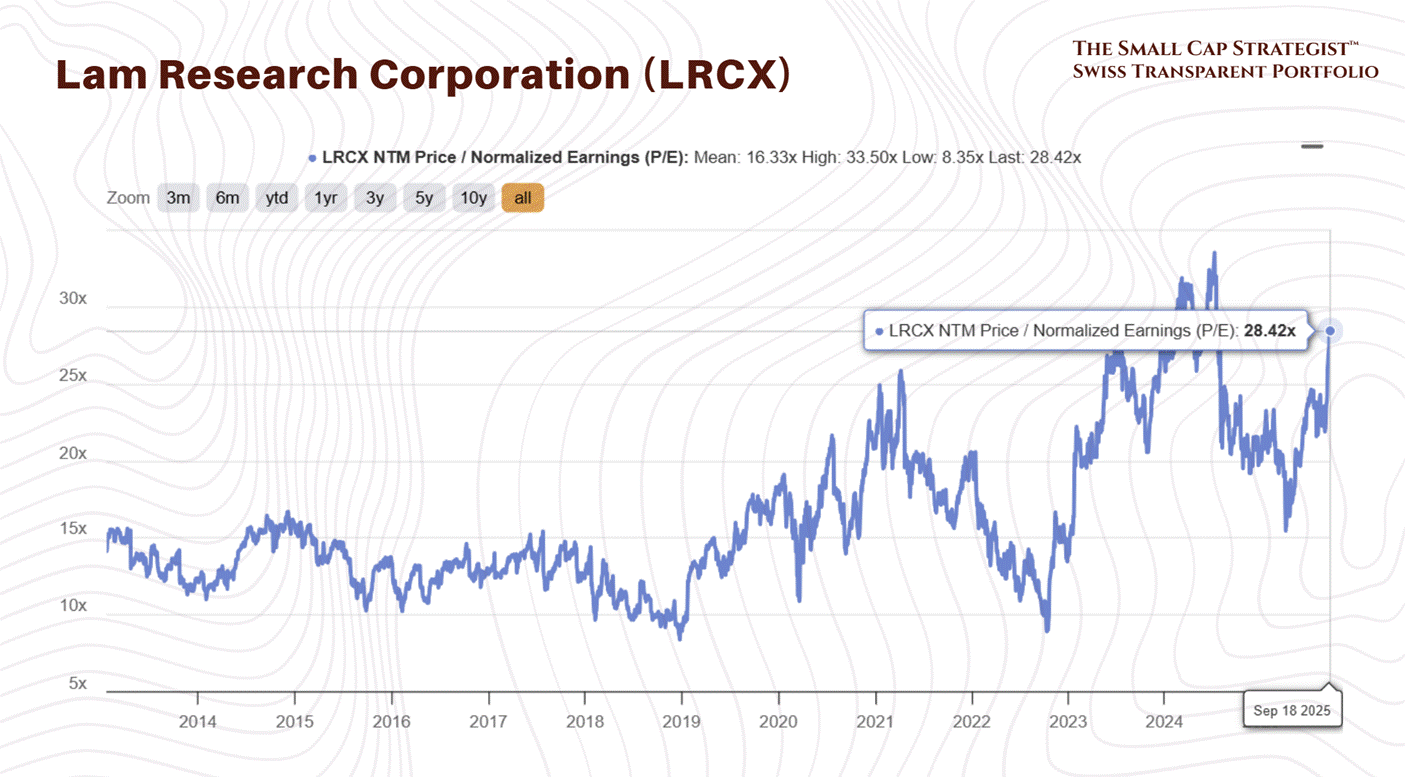

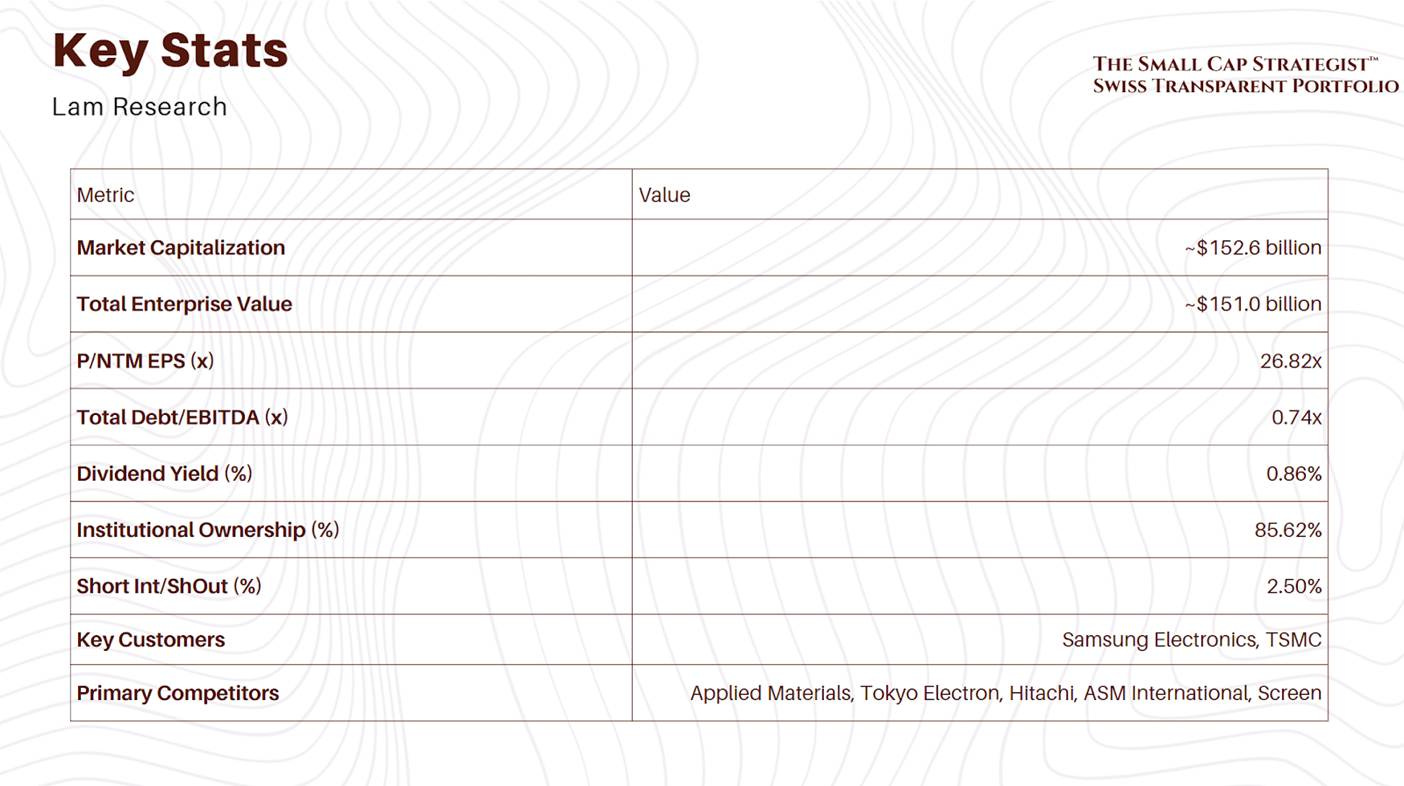

After such a robust run in fundamentals, is Lam Research still reasonably valued? In many cases, a stock delivering ~24% revenue growth with 30%+ margins would command a premium, but remember, semiconductors are cyclical, so the market doesn’t simply annualize the recent boom. Lam’s stock currently trades at mid-high 20s forward earnings (next-twelve-month P/E).

This multiple has expanded from the low-teens during the depths of the cycle to the low-20s now, as investors price in the earnings rebound. How does that stack up against peers?

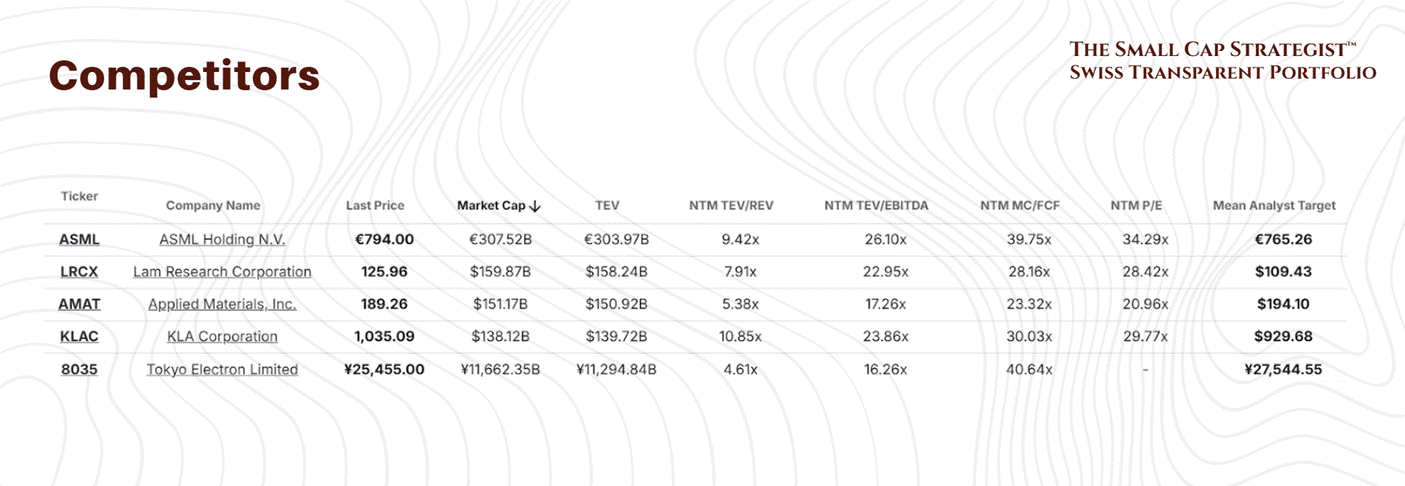

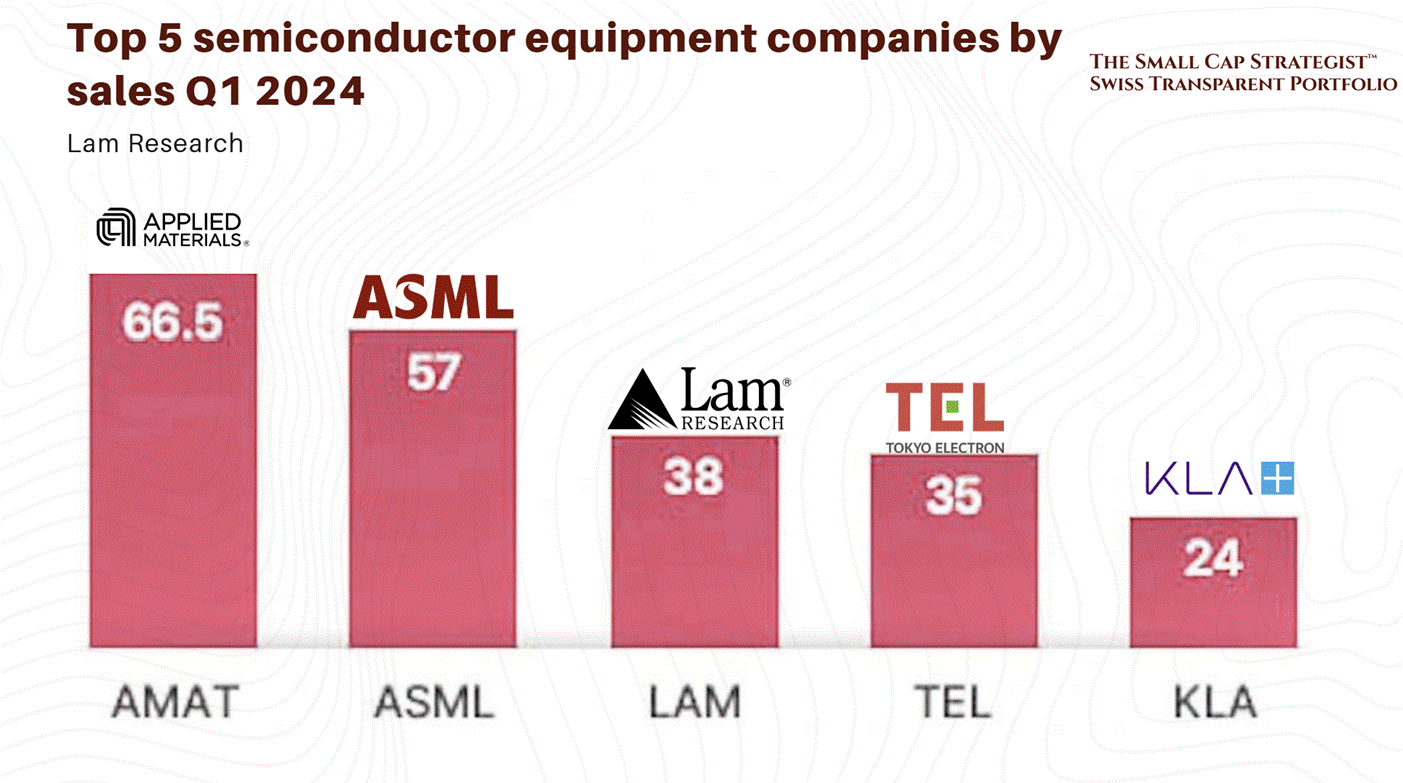

Deposition: The main rival is Applied Materials, Inc. (AMAT), with ASM International and Wonik IPS competing in specific niches like Atomic Layer Deposition (ALD) and Plasma-Enhanced Chemical Vapor Deposition (PECVD).

Etch: The key competitors are AMAT, Hitachi, Ltd., and Tokyo Electron, Ltd. (TEL).

Clean: The primary competitors are Screen Holding Co., Ltd., Semes Co., Ltd., and TEL.

Applied Materials (AMAT): Lam’s closest U.S. peer (covering etch, deposition, and more) trades at roughly ~21x forward earnings, a discount to Lam. Some of that is because Applied has a broader portfolio including slower-growth segments (display panels, etc.) and possibly more exposure to memory volatility. Lam’s higher multiple suggests the market is giving credit for its superior growth/margins this cycle.

ASML Holding (ASML): The Dutch lithography king enjoys a premium valuation, about ~30x+ forward P/E, thanks to its monopoly in EUV technology and very high backlog visibility. Lam is a bit cheaper than ASML, reflecting that Lam, while a top player, operates in a more competitive sub-sector (multiple etch/deposition competitors exist) and with more cyclicality in orders.

KLA Corporation (KLAC): KLA (focused on process control/metrology) trades around 29-30x forward earnings in line with Lam. KLA is admired for its consistent margins and somewhat more stable business (metrology demand is steady), which might warrant parity with Lam’s multiple.

Tokyo Electron (TEL): Although exact current multiples fluctuate, TEL (Japan’s big WFE supplier) usually trades in the high-teens to 20x range, similar to Lam.

Lam isn’t insanely priced relative to peers; if anything, it’s mid-pack, cheaper than ASML, dearer than AMAT. The key is how one views Lam’s growth trajectory from here. Analysts currently expect Lam’s earnings to grow at a mid to high-single-digit percentage annually over the next couple of years (coming off the big FY2025 jump). That would put Lam’s PEG ratio (P/E to growth) roughly around 2.5-3 on a 1-year view, or ~1.3 on a 5-year expected basis, not extremely cheap, but not unreasonable for a high-quality business. If one believes the WFE cycle will remain strong and Lam can continue outgrowing the market (say delivering double-digit EPS growth), then today’s ~26-28x forward multiple could actually compress quickly, making the stock look inexpensive in hindsight.

Let’s put it in simple terms: Lam is trading at about 26-28x next year’s earnings, for a business that just grew earnings 30%+ and has a secular tailwind from AI.

For comparison, many pure “AI plays” or software names trade at much higher multiples with lower profitability. Here we have a company printing >30% operating margins and over 50% ROE, available at a mid-high-20s multiple. One reason for this relative discount is, again, the cyclicality, investors know earnings could ebb in a downcycle. Also, Lam’s heavy China exposure might justify a bit of a valuation haircut due to policy risk.

However, consider Lam’s through-cycle earnings power. Averaging out booms and busts, Lam has grown its revenues and earnings at a healthy clip (10-year revenue CAGR is ~12%, and even including downturns, EPS has trended up).

If the company can indeed achieve something like high-single to low-double-digit growth going forward (which its end markets and recent product momentum suggest is feasible), then double-digit stock returns could be on the table.

In a peer context, Lam offers a bit of a Goldilocks scenario: better growth profile (recently) than Applied Materials for a higher multiple, and almost ASML-level tech criticality at a discount to ASML’s multiple. When we factor in Lam’s solid balance sheet and capital return, the valuation case strengthens, you’re arguably getting a quality compounder at a close to “compounder” price, not a speculative price, yet.

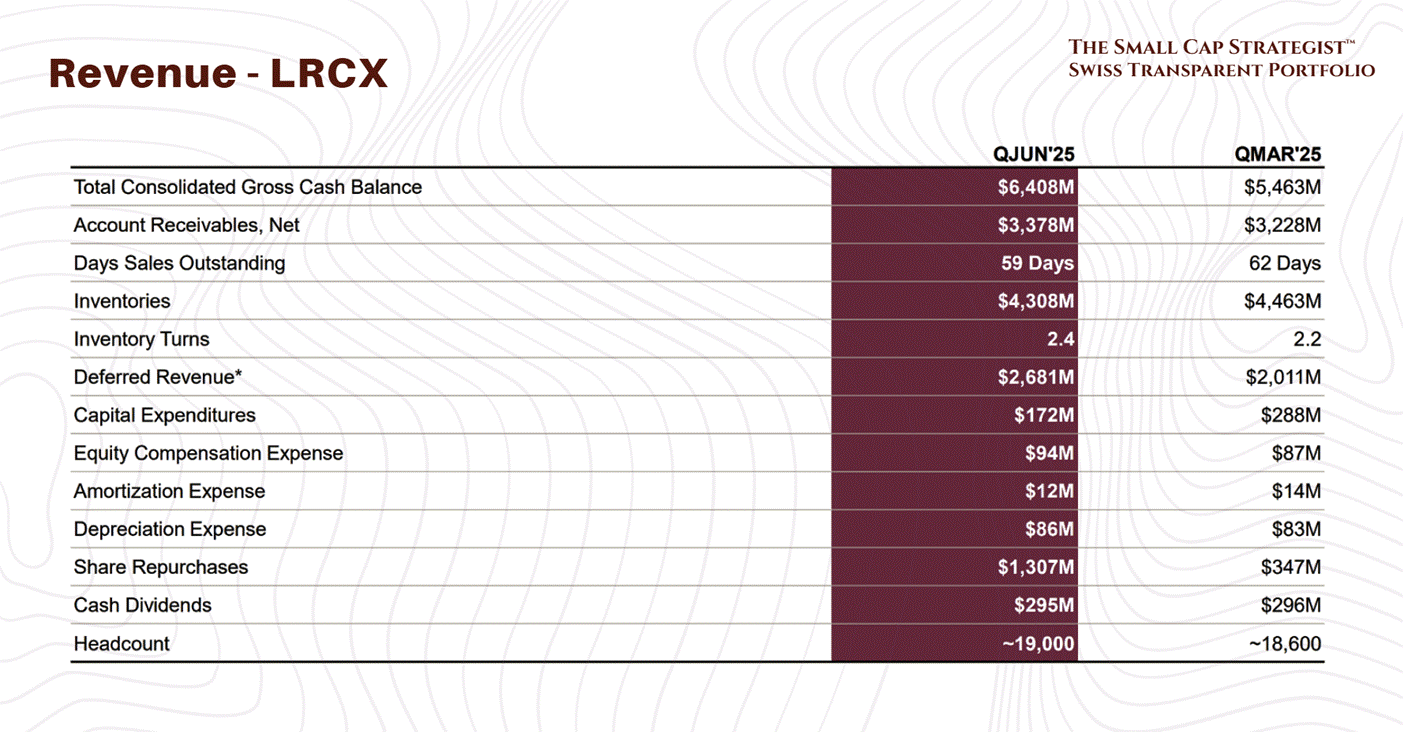

Of course, if the cycle turns down sharply, all these earnings-based multiples can shoot up (as ‘E’ falls). That’s the risk, you might pay 28x forward, only to find out later it was actually 35x if earnings drop. But given the secular demand and Lam’s backlog (deferred revenue is at a record $2.7B, indicating customers have orders in waiting), we have some visibility for the next 1-2 quarters at least.

The current valuation suggests the market is getting more optimistic lately. For long-term believers in the semiconductor growth story, Lam’s valuation leaves room for upside if the company executes and perhaps garners a bit more multiple expansion. At the very least, it doesn’t look egregiously priced, but probably fairly priced.

SWOT Analysis

Understanding Lam Research is understanding its immense strategic power and the inherent vulnerabilities that come with operating at the apex of a deeply cyclical and geopolitically charged industry.

Strengths: "Complexity is Cash Flow" Moat

Lam Research's primary strength is its indispensable role in enabling the ever-increasing complexity of modern semiconductors.

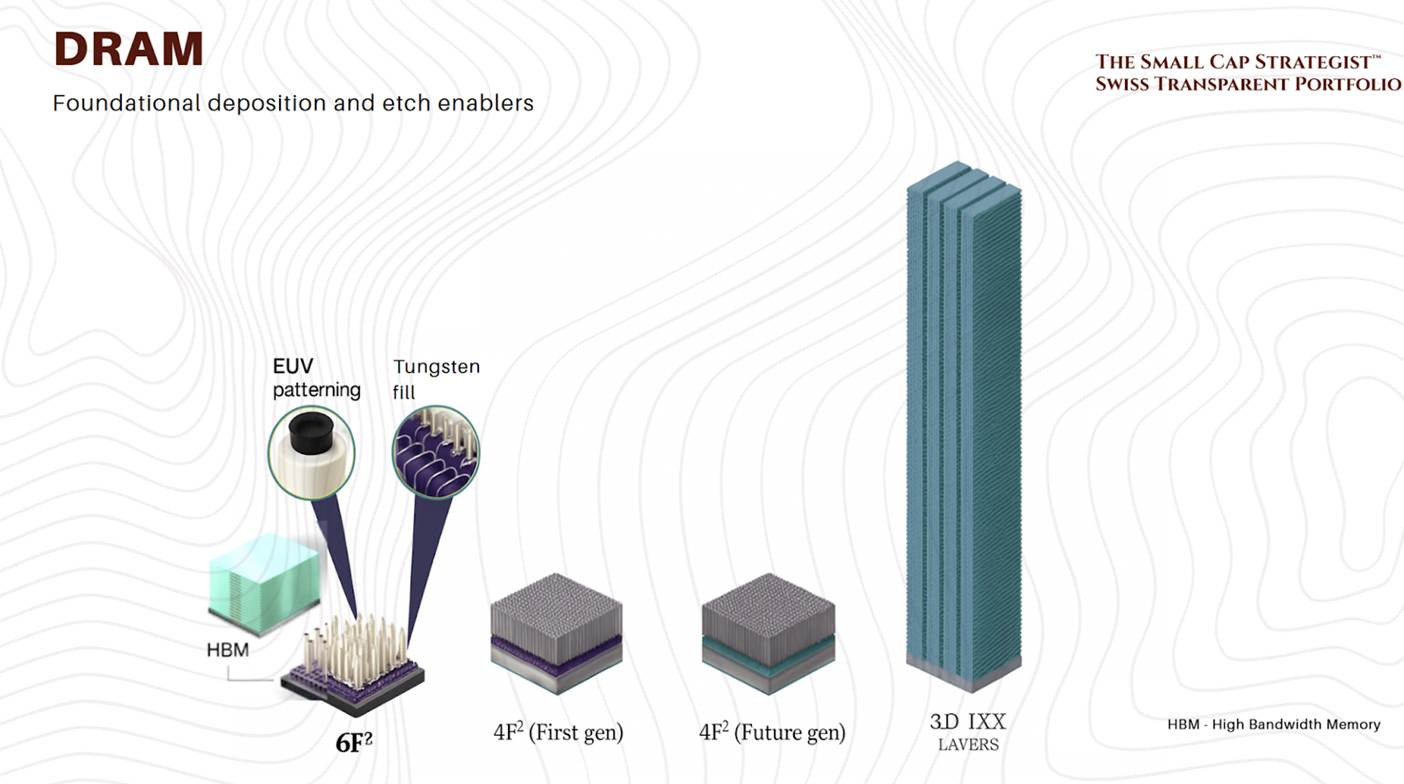

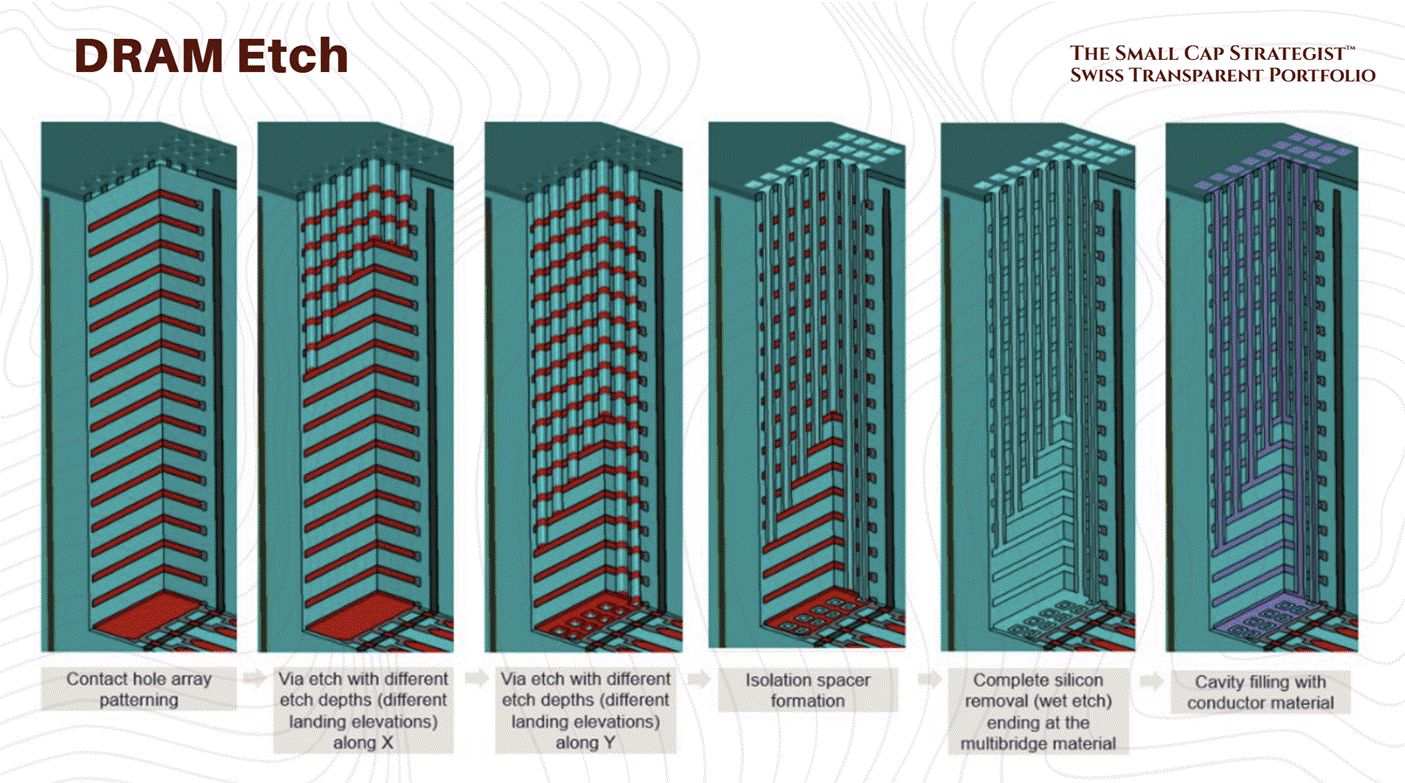

For decades, the industry's progress was largely a two-dimensional affair: shrinking transistors to cram more onto a flat piece of silicon. That era is over. The frontier of semiconductor manufacturing has gone vertical. As chips for memory, logic, and AI processors evolve into three-dimensional skyscrapers of silicon, the demand for Lam's core technologies (deposition and etch) grows at a non-linear rate.

Deposition tools build up the layers of a chip, atom by atom, while etch tools carve intricate patterns and deep channels into those layers. Building a 200-plus-layer 3D NAND memory chip, a Gate-All-Around (GAA) transistor, or stacking chips for High-Bandwidth Memory (HBM) requires exponentially more of these two fundamental processes than any 2D chip ever did.

This is the heart of Lam's moat.

The company's management has explicitly stated that "etch and deposition intensity is rising with 3D scaling," causing Lam's served available market (SAM) to expand to approximately the mid-30s percentage of total Wafer Fabrication Equipment (WFE) spending in 2025.

This is a powerful structural tailwind. Lam's growth is not solely dependent on the cyclical demand for more chips. Its market can expand even if the overall WFE market remains flat, because each new generation of chip requires a greater proportion of the processes Lam dominates. The transition to new materials for advanced transistors provides a stark example. To overcome physical limitations in next-generation chips, the industry is moving from tungsten to molybdenum for critical connections.

Lam's ALTUS Halo tool is leading this transition, and management notes that the more complex molybdenum process drives a "3x increase in metallization SAM per wafer". This is a direct and quantifiable translation of rising complexity into a larger market opportunity for Lam.

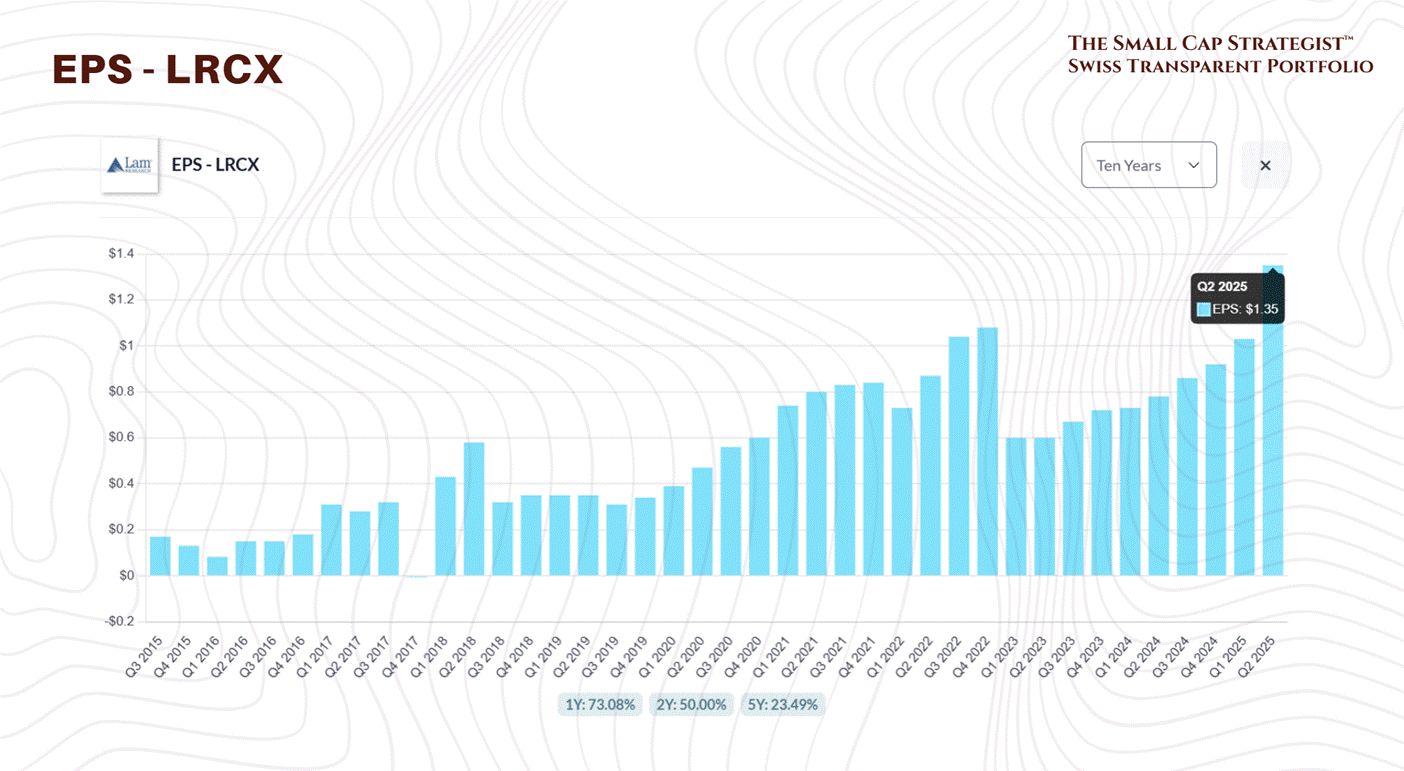

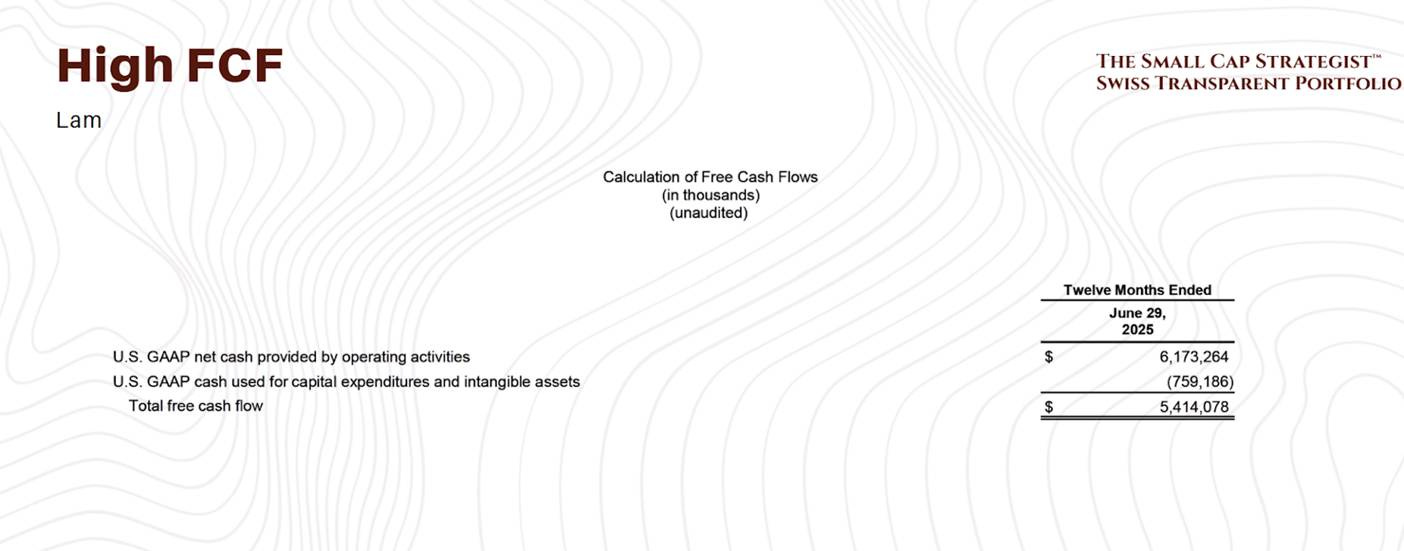

This technological dominance translates directly into financial power. The company recently delivered a record-breaking quarter, with gross margins exceeding 50% for the first time since its merger with Novellus, a new record for earnings per share (EPS), and a record fiscal year revenue of $18.44 billion. This financial strength, including a record free cash flow of approximately $5.4 billion, is the direct result of its structural position as the premier enabler of semiconductor complexity.

Weaknesses: The Concentrated Core

The very source of Lam's strength, its deep integration into the heart of the semiconductor industry, is also its primary weakness. The company's business is highly concentrated around a handful of the world's largest chipmakers and is subject to the industry's notorious cyclicality.

The company's filings explicitly name Samsung Electronics and Taiwan Semiconductor Manufacturing Company (TSMC) as its most significant customers. A strategic shift in capital spending, a change in sourcing strategy, or a technological misstep at just one of these giants could have an outsized negative impact on Lam's revenue and profitability.

This inherent volatility is quantified by the stock's 3-year Beta of 1.87, which indicates that it is significantly more volatile than the broader market, a classic characteristic of a company tied to a cyclical industry. The revenue breakdown further underscores this concentration. In the most recent quarter, the Foundry segment accounted for 52% of systems revenue, while the Memory segment (NVM and DRAM) made up another 41%. Geographically, China, Korea, and Taiwan collectively represent 76% of total revenue. A downturn in any of these segments or regions would reverberate directly through Lam's order book.

Opportunities: Riding the AI Tsunami

The rise of Artificial Intelligence represents the single greatest catalyst for Lam's future growth. AI is not just another application; it is a forcing function for the entire semiconductor ecosystem, accelerating demand for the most complex and powerful chips where Lam's technology is most critical. This opportunity manifests in several key areas.

First, AI workloads require unprecedented memory bandwidth, which is driving the rapid adoption of HBM and other advanced packaging techniques. These methods involve stacking memory chips vertically and connecting them with thousands of microscopic copper pathways, enabling up to a 4x improvement in bandwidth and a 40% gain in power efficiency. Lam's SABRE 3D product family is a leader in the electrochemical deposition processes required to create these connections. The company is capitalizing on this trend, with management expecting its market share in advanced packaging to grow by nearly five percentage points in calendar year 2025 alone.

Second, the processors that power AI models require next-generation transistors. The industry is in the midst of a critical inflection from FinFET to GAA transistor architectures. This shift necessitates new materials and processes to manage power and performance at the 2-nanometer node and beyond. As noted, Lam is at the forefront of this transition with its production-proven ALD Molybdenum tools, which are essential for creating the new contacts in these advanced transistors.

Finally, these powerful secular trends are fueling an expansion of the entire market. Driven by investments in AI, HBM, and GAA, Lam's management recently increased its calendar year 2025 WFE spending outlook from a range of approximately $100 billion to a new, higher range of approximately $105 billion.

Threats: The Geopolitical Chessboard and Market Doubts

Lam Research operates on a global chessboard where geopolitical tensions, particularly between the United States and China, represent the most significant and unpredictable external threat. The company's own forward-looking statements explicitly warn of the risks posed by "trade regulations, export controls, tariffs, trade disputes, and other geopolitical tensions" that may inhibit its ability to sell its products.

These are not abstract risks. Recent news headlines provide real-world context, with a Barron's article highlighting:

"Doubts about growth" and "AI stock boom starts to stumble as investors increase bets against sector".

These market concerns are deeply rooted in the potential for geopolitical disruptions and cyclical downturns. Management has confirmed that tariffs are a direct and immediate headwind, stating that they expect tariffs to increase and negatively impact gross margins in the upcoming December quarter.

This geopolitical tension creates a profound paradox for Lam. The recent upgrade to the WFE forecast was driven almost entirely by a surge in spending from domestic Chinese customers, who now account for 35% of Lam's total revenue. This spending boom is a direct reaction to U.S. restrictions, as China pours capital into building out its domestic semiconductor capacity to achieve self-sufficiency. In the short term, Lam is profiting handsomely from China's race to catch up. However, the ultimate goal of China's industrial policy is to foster domestic equipment champions that can eventually replace foreign suppliers like Lam. Therefore, the current revenue surge from China could be a temporary "sugar high" that masks the significant long-term strategic risk of being designed out of what is poised to become the world's largest semiconductor market.

Lam's Strategy: Winning the Technology Inflections

In such a concentrated market, Lam's strategy is not to compete on every front, but to focus its resources on winning the critical technology transitions or "inflections" that create new, high-margin opportunities and redefine market leadership. Management has articulated a clear and aggressive goal: to "win over 50% share of the incremental SAM" created by these inflections.

Recent performance provides compelling evidence of this strategy in action. The company's latest earnings call was a catalog of wins at key industry inflection points :

NAND Etch: As memory makers push to higher and higher layer counts, the challenge of etching perfectly vertical, microscopic holes through hundreds of layers becomes paramount. Lam's Vantex system, equipped with a proprietary cryogenic process, recently won a "key multi-generation etch decision at a major NAND customer," solidifying its leadership in this crucial high-aspect-ratio etch market.

DRAM Etch: In the DRAM space, the new Akara conductor etch tool, which offers unique plasma pulsing capabilities for superior control, is gaining significant traction. It recently secured "multiple new application wins at a top DRAM maker," signaling a potential share gain in a historically challenging market for Lam.

Foundry/Logic Deposition: As discussed, Lam is the "only company with ALD Moly tools already in production in foundry logic" and just secured another key win for a next-generation application, cementing its first-mover advantage in this critical materials transition.

This focus on winning inflections is amplified by the power of incumbency. Lam's leadership in current-generation technologies provides a decisive advantage in developing future ones. The company's massive installed base of equipment acts as a global network of sensors, providing a constant stream of performance data and deep integration into its customers' R&D roadmaps. To develop a tool for a 2-nanometer GAA process, a company must have an intimate, real-time understanding of the challenges its customers are facing with the current 3-nanometer FinFET process.

Lam's position as a key supplier to the world's leading chipmakers gives it a front-row seat to these challenges. This deep, collaborative relationship allows Lam to co-develop solutions with its customers, effectively locking out competitors who lack that level of trust and access. In the semiconductor equipment industry, market share is incredibly "sticky," and leadership in one generation is the strongest predictor of leadership in the next.

Looking into Management

A company's long-term success is often a reflection of its leadership. In the case of Lam Research, the C-suite is not composed of generalist executives but of industry veterans with deep, specialized operational and technical expertise. This collective experience forms a critical, and often underappreciated, strategic asset.

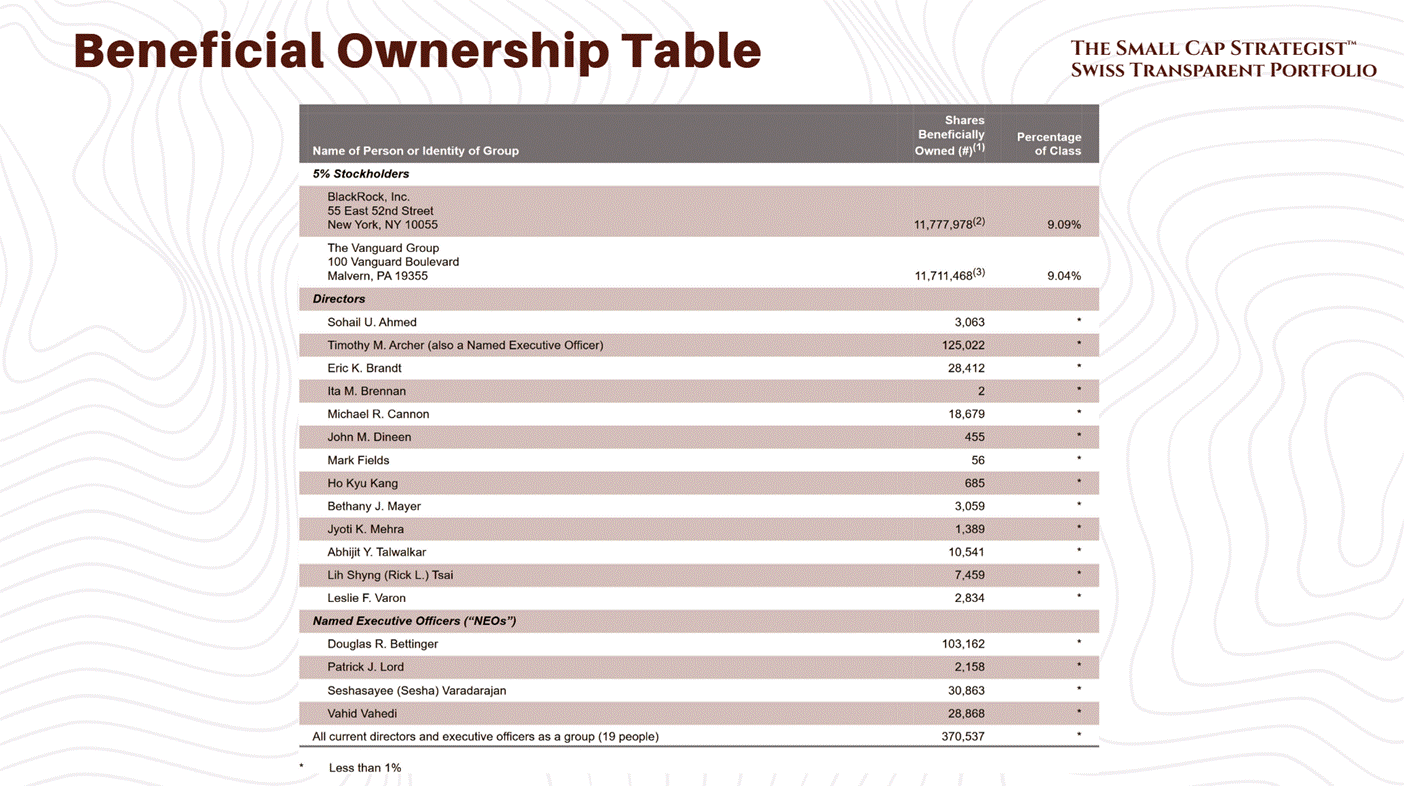

The leadership team's DNA is rooted in the very fabric of the semiconductor equipment industry, suggesting a culture focused on achieving long-term technological dominance over pursuing short-term financial engineering. Employee surveys reflect confidence in this leadership, with CEO Tim Archer receiving a high approval rating of 84/100, placing him in the top 5% of CEOs at similarly sized companies.

Timothy Archer (President & CEO): The Veteran Operator. Mr. Archer's career path is a microcosm of the industry's evolution and consolidation. He spent nearly two decades at Novellus Systems, a major equipment supplier, rising through a series of technical and business unit leadership roles before becoming its Chief Operating Officer. When Lam Research acquired Novellus in 2012, Mr. Archer became the COO of the combined, more powerful entity, and was eventually promoted to CEO in 2018. His entire career has been built on deep product knowledge and operational execution, not on abstract corporate strategy.

Douglas Bettinger (EVP & CFO): The Seasoned Financial Steward. Mr. Bettinger's resume reads like a tour of the semiconductor value chain. He spent eleven years at Intel, the world's premier integrated device manufacturer, in both manufacturing and corporate finance roles. He then served as CFO of Avago (now Broadcom), a leader in chip design, before taking the financial helm at Lam Research in 2013. This diverse experience provides him with an intimate, end-to-end understanding of the industry's capital cycles and the rigorous financial discipline required to navigate them. This prudence is reflected in the company's strong balance sheet, which features a very low Total Debt/EBITDA ratio of just 0.74x.

Dr. Patrick Lord (EVP & COO): The Technical Mastermind. With a Ph.D. in Mechanical Engineering from the Massachusetts Institute of Technology, Dr. Lord brings a formidable technical depth to the executive team. Like Mr. Archer, he is a Novellus veteran who has spent his career managing the development and support of complex semiconductor equipment. At Lam, he has led the critical Customer Support Business Group (CSBG) and Global Operations. His presence in the C-suite ensures that the immense complexities of atomic-scale engineering have a powerful and informed voice at the highest level of strategic decision-making.

The stability of this leadership team is, in itself, a strategic weapon. The R&D and product development cycles in the semiconductor industry are incredibly long, often spanning five to ten years and costing billions of dollars. A leadership team that frequently changes its strategy is doomed to fail. The long tenure of Lam's key executives, Mr. Bettinger has been CFO for over a decade, and Mr. Archer has been in top operational roles since 2012, allows the company to make and adhere to the long-term R&D bets necessary to win. This continuity builds profound trust with customers, who are themselves making multi-billion-dollar, multi-decade bets on their technology roadmaps. This stability is a core part of Lam's competitive moat.

Operational Overview

At its core, Lam Research is a company that solves some of the most difficult physics and chemistry problems on Earth. Its products are not commodities; they are highly specialized, multi-million-dollar systems designed to manipulate matter at the atomic level with flawless precision and repeatability, millions of times over.

Products That Solve Impossible Problems

Lam's vast product portfolio can be understood by grouping it according to the three fundamental challenges of semiconductor manufacturing: building up, carving down, and keeping it clean.

Challenge 1: Building Up (Deposition). This is the process of creating the hundreds of atomic-scale layers of conducting and insulating materials that form a modern chip. Lam's deposition tools act like atomic-scale 3D printers, each specialized for a different material and purpose.

Product Families: The ALTUS family uses chemical vapor deposition (CVD) and atomic layer deposition (ALD) to create the tiny tungsten and molybdenum wires and contacts that connect transistors. The SABRE family uses electrochemical deposition to lay down the copper "interconnect" wiring that links different parts of a chip. The SPEED, VECTOR, and Striker families are used to deposit the critical dielectric (insulating) layers that prevent electrical crosstalk and short circuits, with each system optimized for different film properties and structures.

Challenge 2: Carving Down (Etch). Once the layers are deposited, they must be sculpted into functional circuits. This is the role of etch, which selectively removes material to create the features of a chip. If deposition builds the block of marble, etch is the impossibly precise chisel.

Product Families: The Flex and Vantex product lines are dielectric etchers, used to carve patterns and deep trenches in the insulating layers. The Kiyo and Versys Metal families are conductor etchers, used to shape the electrically active materials. The Syndion family is specialized for deep silicon etch, a process critical for creating components like CMOS image sensors and the Through-Silicon Vias (TSVs) used in advanced packaging.

Challenge 3: Keeping it Clean (Clean). The semiconductor manufacturing process can involve hundreds of individual steps. Between each step, the silicon wafer must be perfectly cleaned. A single stray particle, no bigger than a virus, can land on a critical part of a device and ruin an entire multi-million-dollar chip.

Product Families: The Coronus family uses plasma to clean the beveled edge of the wafer, removing residues that could flake off and cause defects. The DV-Prime, Da Vinci, EOS, and SP Series are wet clean systems that use specialized chemistries to remove microscopic contaminants from the wafer's surface without damaging the delicate structures already built upon it.

Segments and Geographies

Lam's business is organized into two primary segments that work in concert. The Systems Revenue segment encompasses the sale of the new equipment described above. This is the more visible and cyclical part of the business, driven by customers' large-scale capital expenditure plans for building new fabs or upgrading existing ones.

The second, and arguably more strategic, segment is the Customer Support Business Group (CSBG). This is a massive, high-margin, recurring revenue business that provides spares, services, and upgrades to Lam's enormous global installed base of equipment. CSBG is more than just a stable source of cash flow; it is a powerful competitive flywheel that fuels a virtuous cycle. The large installed base generates predictable revenue from necessary spares and services, which recently totaled $1.73 billion in a single quarter. This same installed base creates a captive market for upgrades, a business that just hit a third consecutive record quarter, driven by NAND customers converting their existing tools to produce higher layer-count devices. Offering cost-effective upgrades makes Lam an incredibly "sticky" partner, as customers can extend the life and capability of their multi-million-dollar assets. Finally, the data and learnings gathered from servicing this global fleet, what Lam brands as "Equipment Intelligence", feed directly back into the R&D process, enabling the company to build better, more reliable, and more productive tools in the next generation.

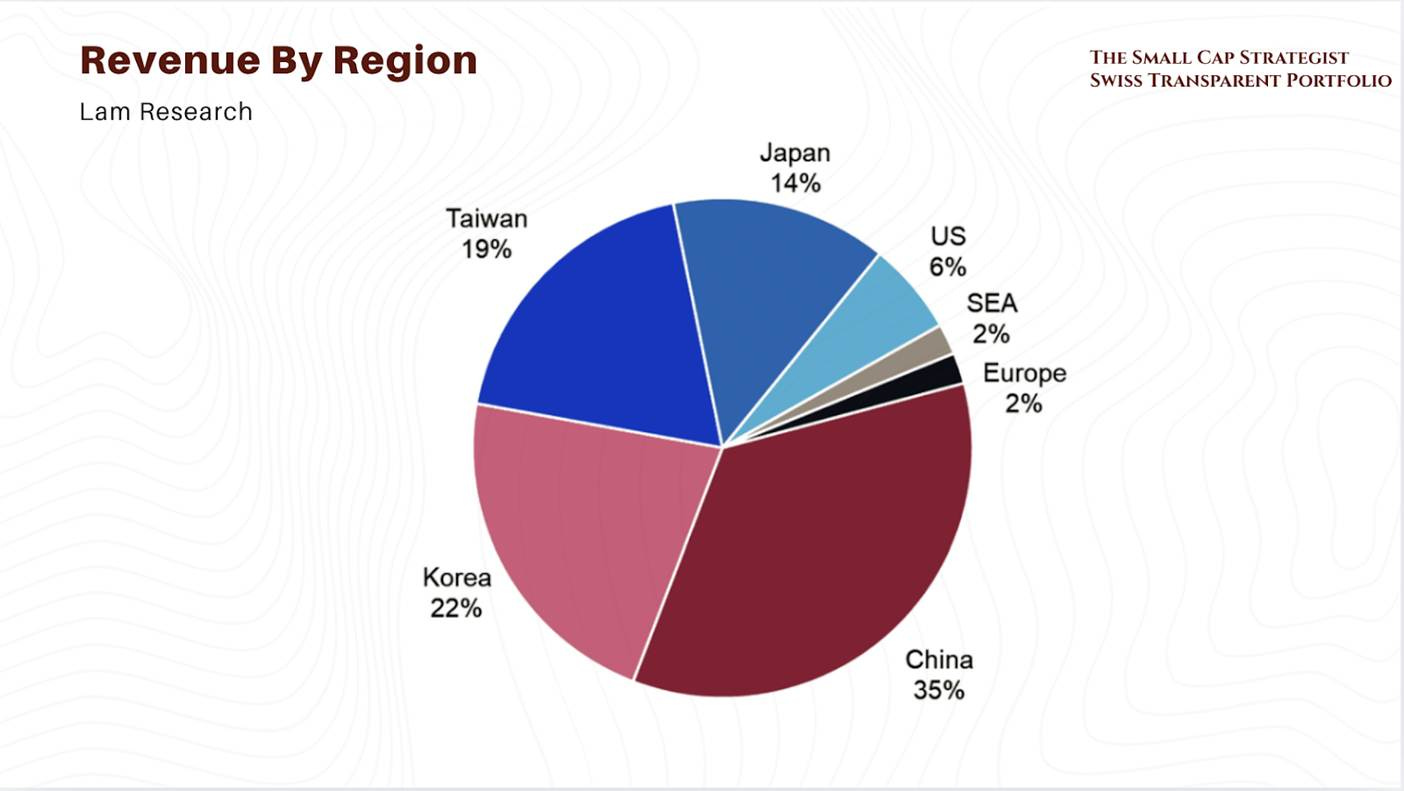

Geographically, Lam's revenue is concentrated in Asia, the global hub of semiconductor manufacturing. The latest breakdown shows China as the largest region at 35%, followed by Korea (22%), Taiwan (19%), and Japan (14%). The United States and Europe account for 6% and 2%, respectively. This distribution highlights Lam's critical proximity to the world's leading chipmakers but also starkly illustrates its exposure to any geopolitical instability in the region.

Global Capacity and Expansion

Lam's global manufacturing footprint is a key strategic asset designed to enhance supply chain resilience and place production closer to its major customers. In addition to its headquarters and manufacturing in the U.S., the company has long-standing production facilities in Austria, South Korea, and Taiwan.

In recent years, Lam has undertaken a significant expansion of its global capacity:

Malaysia: In August 2021, Lam opened its newest and largest manufacturing facility in Batu Kawan, Penang. This state-of-the-art site, with a built-up area of over 800,000 square feet, is a cornerstone of the company's strategy to fortify its global network and serve the growing Asian market.

India: Lam is making a major strategic investment of $1.2 billion to establish new facilities in Bengaluru. This investment includes a new, advanced systems lab to support the design and validation of next-generation chips and a significant expansion of its supply chain operations in the country, aligning with India's ambition to become a global semiconductor hub.

The Reverse Thesis - What Could Go Wrong?

To maintain diligence, it is crucial to remember the painful lessons of past market cycles and to rigorously challenge the bull case. Despite its formidable strengths and dominant market position, Lam Research's future is not guaranteed. A confluence of geopolitical, competitive, and cyclical factors could severely challenge the investment thesis.

Scenario 1: The Great Wall of China

The "China Paradox" could resolve in a highly negative fashion for Lam. The most acute risk is a further escalation of U.S. trade policy, leading to a near-total ban on the sale of semiconductor equipment to China. Such a move would vaporize 35% of Lam's revenue almost overnight. A more gradual but equally damaging risk is that China's massive investment in its domestic equipment industry bears fruit faster than expected. If Chinese champions in etch and deposition mature to the point where they can displace Lam, even in trailing-edge nodes, it would begin a slow and steady erosion of Lam's largest geographic market. The explicit warnings about trade regulations in the company's own filings underscore the severity of this threat.

Scenario 2: The AI Hype Cycle Deflates

The current investment thesis for Lam is heavily predicated on the continuation of the AI-driven demand boom. However, the semiconductor industry has a long and painful history of boom-and-bust cycles. If the current massive capital investment in AI infrastructure proves to be a speculative bubble, the consequences for Lam would be severe. A slowdown in demand for AI accelerators would lead to sharp capital expenditure cuts from the very customers buying Lam's most advanced and highest-margin equipment. The weak guidance from competitor Applied Materials, which cited "digestion of capacity in China" and "non-linear demand from leading-edge customers," could be a leading indicator of such a downturn.

Scenario 3: A Competitor's Breakthrough

While Lam is a leader, it does not hold a monopoly in any of its key markets. The company is locked in a relentless R&D race with equally powerful and well-funded competitors like Applied Materials and Tokyo Electron. The risk exists that one of these rivals could achieve a fundamental breakthrough in a next-generation technology. For example, Applied Materials recently announced that its etch business crossed $1 billion in quarterly revenue for the first time, driven by new wins in advanced DRAM, highlighting the intense competitive pressure. In this industry, technological leadership is paramount. Being second-best on a critical, high-volume application can mean losing an entire technology node's worth of business, a setback that can take years and billions of dollars to recover from.

Scenario 4: The Analyst Bear Case Materializes

Barron’s skepticism, reinforced by Morgan Stanley’s downgrade to Underweight ($92 target), frames the bear case. The claim is that NAND demand and China sales fade by 2026, so after 2024 to 2025 outperformance Lam’s growth reverts to the market, leaving a roughly 27x NTM multiple that looks full and vulnerable to cyclicality.

Long-Term Outlook and Key Risks

No investment is without risks, and a cyclical company like Lam Research certainly has its share. Let’s tackle the long-term outlook first, essentially, why one might be excited to hold Lam for years, and then the key risks that could upset that outlook.

Long-Term Outlook: The secular trajectory for semiconductor demand is unquestionably upward. We are digitizing everything, from AI in cloud data centers to 5G networks, electric vehicles, smart factories, and even everyday appliances becoming “smart”. All of that runs on chips.

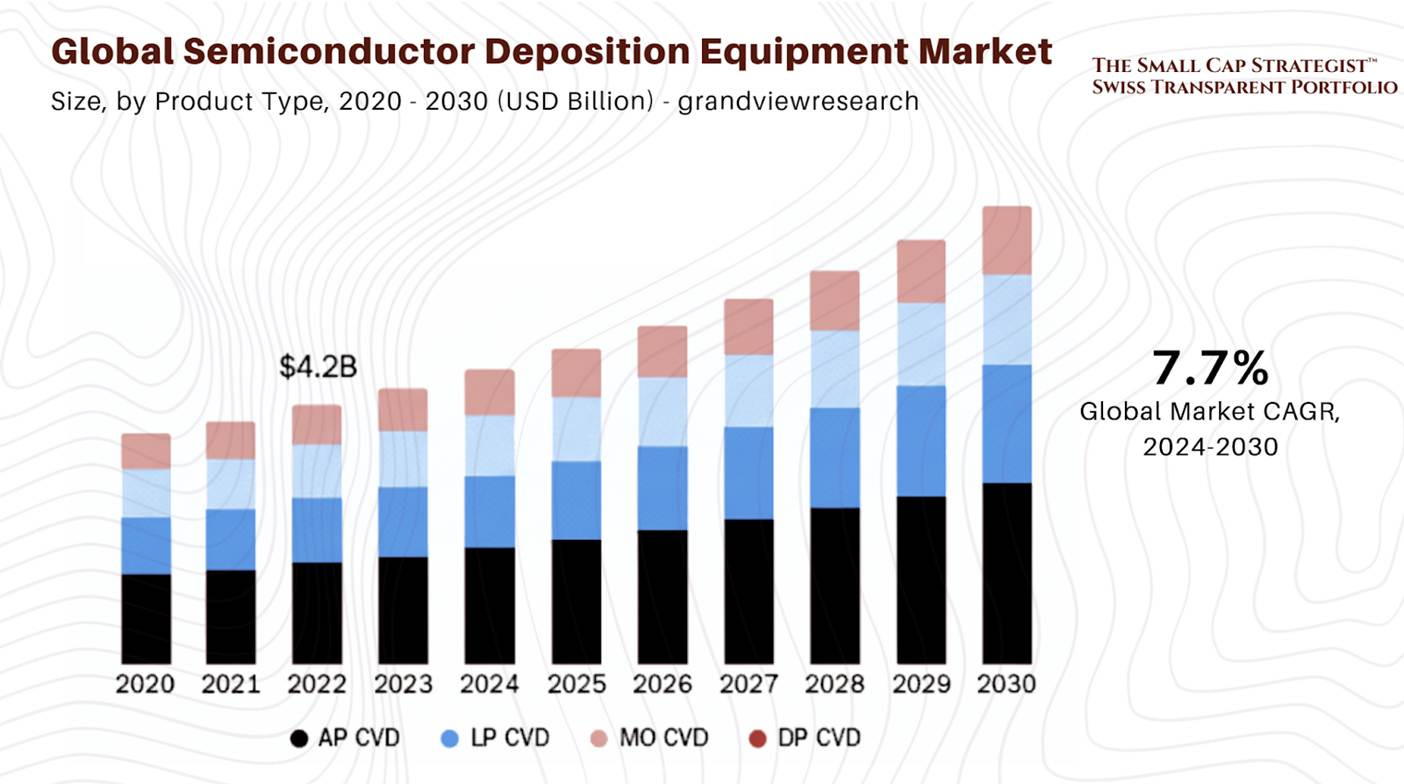

Global semiconductor sales are expected to grow at mid-to-high single digit CAGR over the next decade, and with each new generation of chips, the complexity (and cost) of manufacturing goes up. This means wafer fab equipment spending has a secular growth trend, indeed, the WFE market is projected to roughly double from 2023’s ~$87B to perhaps $138B by 2030, roughly ~7.5% CAGR. Lam, being one of the top players, is positioned to capture a good chunk of that growth. In fact, thanks to the trends we discussed (GAA, 3D NAND, advanced packaging), Lam’s served market may grow even faster than WFE as a whole (since deposition/etch intensity is rising). If Lam can maintain its tech leadership, it could potentially outpace the industry growth (gain market share in new applications).

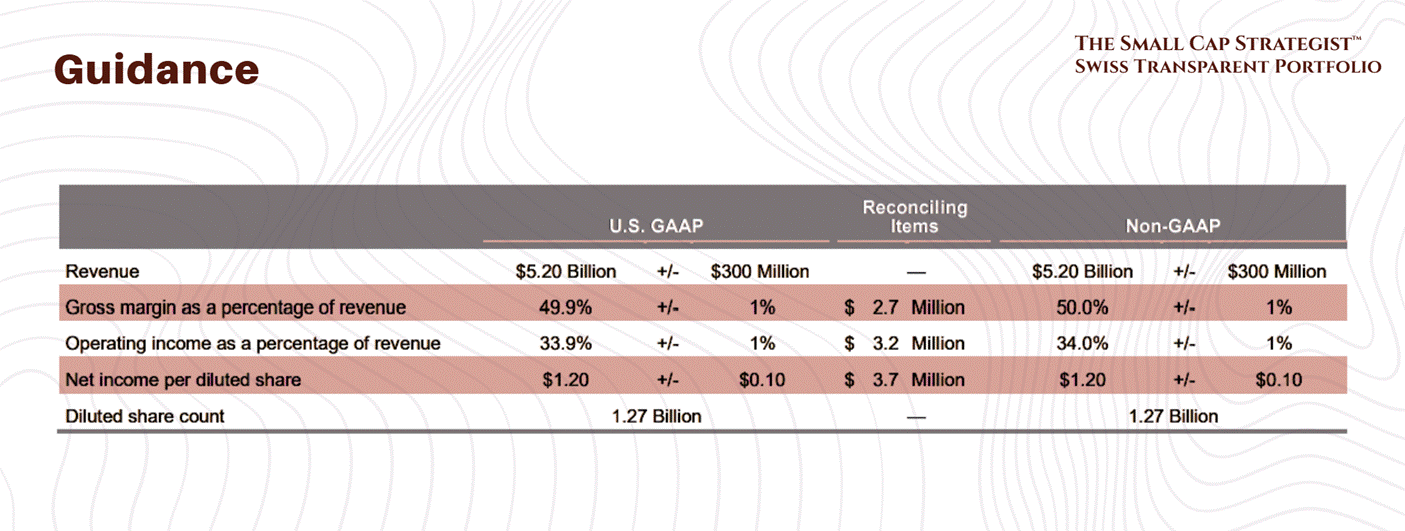

For the quarter ended September 28, 2025, Lam is providing the following guidance:

In the long run, one can envision Lam as a cash-generating compounder: selling essential gear to chip makers year after year, expanding into any new process step that arises (they could even push into adjacent areas if needed, like more surface prep or cleaning tools), all while collecting recurring service revenues. The company has also proven adept at navigating technology transitions (e.g., when new transistor structures emerged, Lam had the tools ready). Looking 5-10 years out, trends like AI, quantum computing, AR/VR, and IoT will likely drive demand for both leading-edge logic and massive amounts of memory, which means fabs will keep spending on equipment.

Additionally, geographic diversification of fab capacity (US, Europe, India, etc.) could keep investment cycles rolling in a more distributed fashion (perhaps avoiding one giant global boom/bust by spreading it). Lam’s broad customer base means it will win equipment orders from Intel’s new U.S. fabs or TSMC’s Arizona fab, and from new Chinese memory fabs, etc., as they come online.

Now, for the sobering part, Risks:

Cyclicality (Timing Risk): The most evident risk is that the semiconductor capital equipment business is highly cyclical. We only have to look at Lam’s recent history: FY2023 saw a sharp downturn (revenue -14%) when memory makers slashed spending; then FY2025 saw +24% growth when the cycle rebounded. These swings can be brutal for stock prices. If we hit another downcycle in 2026 or 2027 (for example, if chip demand overshoots and then inventory builds up, or a global recession hits electronics sales), Lam’s orders could drop quickly by 20-30%. That would pressure revenues, margins (under-absorption of fixed costs), and earnings, and likely cause a significant stock correction. Investors in Lam must be able to stomach volatility. The long-term trend might be up, but it won’t be a smooth ride; timing matters. One mitigating factor is the services segment which cushions downturns slightly, but it won’t fully offset a big capex cut by customers.

China & Geopolitical Risk: We’ve highlighted Lam’s exposure to China (35% of sales), this is arguably the top specific risk. U.S. export controls already restrict selling the most advanced tools to Chinese fabs; any tightening of these rules could hit Lam. For instance, if the U.S. further lowers the technology threshold on what’s allowed (say, banning certain etch/deposition tools that can be used for <14nm processes, or extending restrictions to NAND layers above a certain count), Lam could suddenly lose a chunk of business or face delays (licenses etc.). Additionally, there’s always a tail risk of geopolitical conflict (e.g., Taiwan tensions) which could massively disrupt the semiconductor supply chain and equipment sales. While such black swan events are hard to predict, they’d have huge negative impact on Lam. Even absent extreme events, China’s cyclical demand could cool, a lot of Chinese fab projects have been front-loaded; if government funding there wanes or they reach capacity, that 35% slice might shrink on its own. Lam would have to rely more on other regions to pick up slack.

Competition and Technological Risk: Lam faces capable competitors, mainly Applied Materials and Tokyo Electron in etch/deposition. There’s the risk that a competitor could develop a better tool for a critical process, causing Lam to lose market share at a key customer. For example, if Applied’s new etch tool or TEL’s deposition system outperforms Lam’s on a next-gen node, Lam might see a revenue hit. So far, Lam has been holding or gaining share, but competition for each new node’s process wins is fierce. There’s also the risk of technological shifts that reduce the need for some of Lam’s tools. For instance, if a new chip architecture dramatically simplified manufacturing (not likely with how physics is going, complexity is increasing, not decreasing, at least in the next 5-10 years), or if a customer found ways to extend equipment life/reuse tools more efficiently, it could dampen equipment demand. Another angle: as EUV lithography becomes more capable, it might replace some multi-etch patterning steps (a minor risk, since advanced chips still need multiple etch steps for other reasons, but worth noting historically multi-patterning litho benefitted deposition/etch, and if that need declines, it’s a small headwind).

Customer Concentration & Spending Patterns: While Lam sells to many customers, a few big players account for a substantial chunk of WFE spend (TSMC, Samsung, Intel, Micron, SK Hynix, etc. are probably 5 that together drive >50% of WFE). If any one of them significantly changes its capex plans or supplier preferences, Lam could feel it. For example, Intel has been working to increase its own share in foundry; if Intel’s plans falter, their equipment orders might slow. Or if TSMC decides to delay its next-node expansion due to softer end-demand, Lam’s shipments would be impacted. These are normal industry dynamics, but they introduce lumpiness and unpredictability in forecasting Lam’s revenue year-to-year.

Macroeconomic and Other Risks: A broad global recession would likely curtail consumer demand for electronics, trickling down to chip demand and fab investment. High interest rates can make financing new fabs more expensive (though the leading firms are cash-rich, it could affect marginal projects). Inflation in supply chain could squeeze Lam’s margins if not managed (Lam has done well on margins recently, but things like component costs or labor inflation could nibble). There’s also execution risk: ramping production to meet surging demand can strain supply chains, any misstep (quality issues, delays) could harm Lam’s reputation and finances. Lastly, environmental/social risks: semiconductor manufacturing is water- and energy-intensive; equipment companies might face future regulations or pressures to make tools more sustainable (not a huge risk perhaps, but something the industry is watching).

In balancing the outlook and risks, one has to ask: Do the long-term tailwinds outweigh the near-term turbulence? For Lam Research, the long-term thesis is very compelling, virtually every innovation in tech will require more advanced chips, and Lam enables those chips to be made. The company has shown it can adapt and even thrive with each tech transition (from planar to 3D devices, from single patterning to multipatterning, etc.). It’s not an exaggeration to say Lam’s prospects are tied to humanity’s demand for computation, a pretty good bet to hitch onto. However, the ride will be choppy. Investors should be prepared for 20-30% drawdowns in stock price when cycles turn, and understand that a stock like $LRCX requires a bit of patience and conviction through volatility. We believe the long-run rewards can justify that risk, but position sizing and timing are key to manage the journey.

Conclusion

Lam Research’s latest results underscore a narrative of resilience and opportunity. Here’s a company that, only a year ago, was navigating a harsh semiconductor downturn, yet it kept its strategy on course, and as the tide turned, Lam is now achieving record revenues, 50%+ gross margins, and record earnings per share. The first half of 2025 showed that Lam can not only weather the storm but emerge stronger, capitalizing on the furious demand for new chip technology. Lam has many ingredients of a great investment: a dominant market position in a growing industry, superb margins (with potential to expand further), robust free cash flow generation, and a management team that’s focused on long-term value (and willing to buy back stock when it’s cheap). The stock’s performance has reflected this to an extent, it’s well off the lows and has outpaced the broader tech sector year-to-date, but it’s not in nosebleed valuation territory, yet.

So, is $LRCX an investment opportunity right now? We’d say yes, correctly timing the entry. The opportunity lies in owning a foundational player of the semiconductor value chain at a time when secular forces (AI, cloud, 5G, etc.) are aligning to potentially drive years of growth. Lam is no speculative startup; it’s a proven cash cow with technological prowess that still trades at a reasonable earnings multiple. If one believes that the world’s appetite for computation will continue its exponential rise, then companies like Lam (which equip the chipmakers) are poised to benefit disproportionately. Every new fab that gets built, every new chip architecture that ramps to high volume, translates to business for Lam Research. The curiosity aspect for an investor is that disconnect: Lam’s vital role vs the market’s cautious pricing. That’s often where investment alpha is born, in the gap between perception and reality.

However, we must balance the enthusiasm with caution: Lam is not a sleepy compounder that goes up and to the right every year. It’s more like a rollercoaster on an upward slope. The major risk factors we discussed, cyclicality, China, etc. are real and not going away. A prospective investor should be willing to hold through volatility or even add on dips if the long-term thesis remains intact. In our view, Lam’s fundamental quality and strategic importance tip the scales such that the rewards outweigh the risks for a long-term investor at today’s valuation.

To put it succinctly, Lam Research is etching out its place as a beneficiary of the next tech revolution. It has the hallmarks of a compelling opportunity: strong growth drivers, relative value, and competent stewardship. Just as importantly, it has what we love to see, a business that can compound value (through reinvestment and buybacks) over time.

If you enjoyed this post, consider supporting our work by becoming a paid or free subscriber.

| A guest post by

|

| A guest post by

|