20+ Swiss Stocks to Buy and Sleep Well

The Ultimate Quality-at-a-Price Guide (June 2025 Edition)

Swiss stocks have long been synonymous with stability, quality, and global reach, the hallmarks of true long-term compounders. Instead of chasing noise, let’s focus on what matters: durable competitive advantages (moats), sensible valuations, and the compounding power that unfolds over years, not quarters.

In this deep dive, I highlight Switzerland’s top 20+ publicly traded companies (ranked by market value and significance), summarizing what they do, where their moat lies, and how their current valuations stack up against historical norms. Think of it as a high-conviction quickfire round.

We’ll then zoom in on five of the most interesting setups right now, with a closer look at companies like Roche, Swiss Re, Logitech, Partners Group, and Swissquote, businesses where today's pricing offers a potentially attractive long-term entry point.

👉 Here’s what you’ll find inside:

A full tour of Switzerland’s stock market: 20+ leading Swiss companies you should know.

Current valuations vs historical norms (we will use NTM P/E in this occasion ).

The 5 stocks I find most interesting right now.

Whether you're a seasoned buy-and-hold investor or simply looking for “buy and sleep well” ideas, these Swiss champions provide plenty of substance. Let’s dive in, and as always, bet on durable businesses (but only at the right price).

Swiss Blue-Chip Scorecard: Top 25 at a Glance

1. Nestlé (NESN):

Global leader in food & beverages, with a moat in brand portfolio (over 2,000 brands like Nescafé, Nespresso or Purina) and global distribution. Trading at ~19x earnings, roughly in line/a bit below with its long-term averages ~21x. It’s not cheap for a defensive consumer staple, but offers predictable compounding. Buy and forget.

2. Roche (ROG):

Top-tier pharma & diagnostics giant, protected by patents, pipeline depth, and scale. Now at ~13x P/E, toward the lower end of its historical range. Market worries over patent cliffs may be offering an entry point for long-term believers.

3. Novartis (NOVN):

Pharmaceutical powerhouse with strong IP and pipeline optionality. Valued at ~14x P/E, modest for big pharma. After streamlining operations, Novartis trades below many peers, possibly underappreciating its margin expansion and pipeline upside.

4. Lonza (LONN):

High-tech life sciences manufacturer with switching-cost moats. Now trading at ~35x P/E, well below the nosebleed ~60x we previously saw but still premium vs history (around 25–30x long-run averages). The market still prices strong secular growth ahead.

5. UBS Group (UBSG):

Wealth management leader post-Credit Suisse merger, with a scale moat. Trades at ~14x P/E, quite fair compared to its historical single-digit multiples. Market is pricing in normalized post-merger earnings, leaving upside if synergies deliver.

6. Zurich Insurance (ZURN):

Global insurer with underwriting and brand moat. Now trading at ~15x P/E, close to its historic 13x mean range. A solid income play with moderate upside, assuming stable underwriting performance.

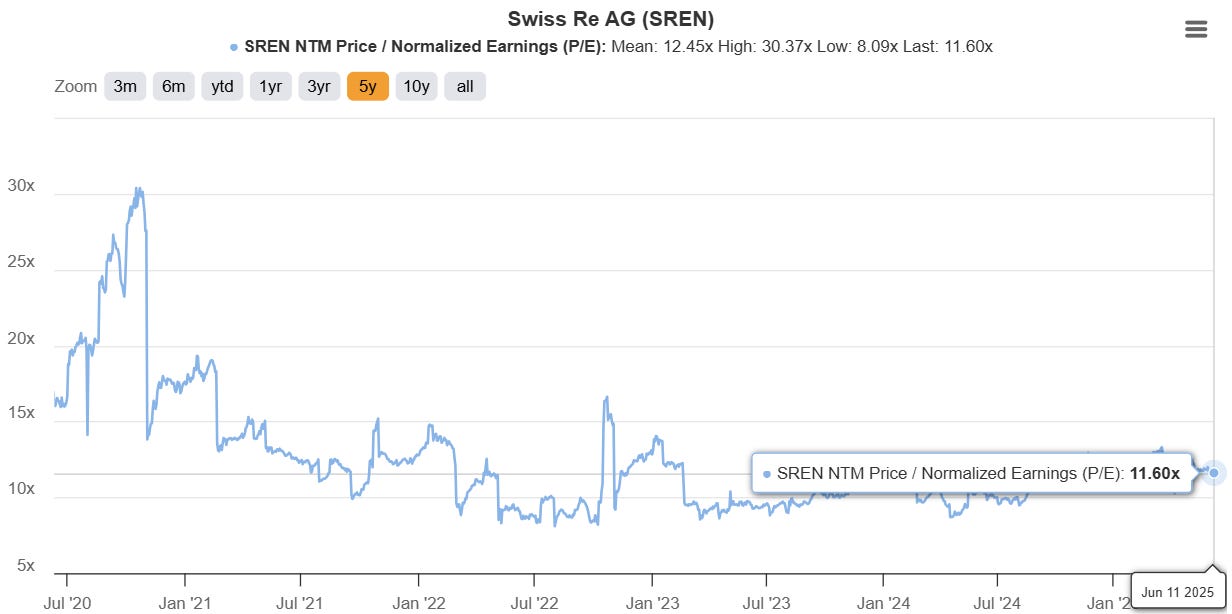

7. Swiss Re (SREN):

Reinsurance major with scale and diversification moats. Valued at ~12x P/E, slightly with its recent averages, suggesting cautious optimism baked in after previous years of underwriting volatility.

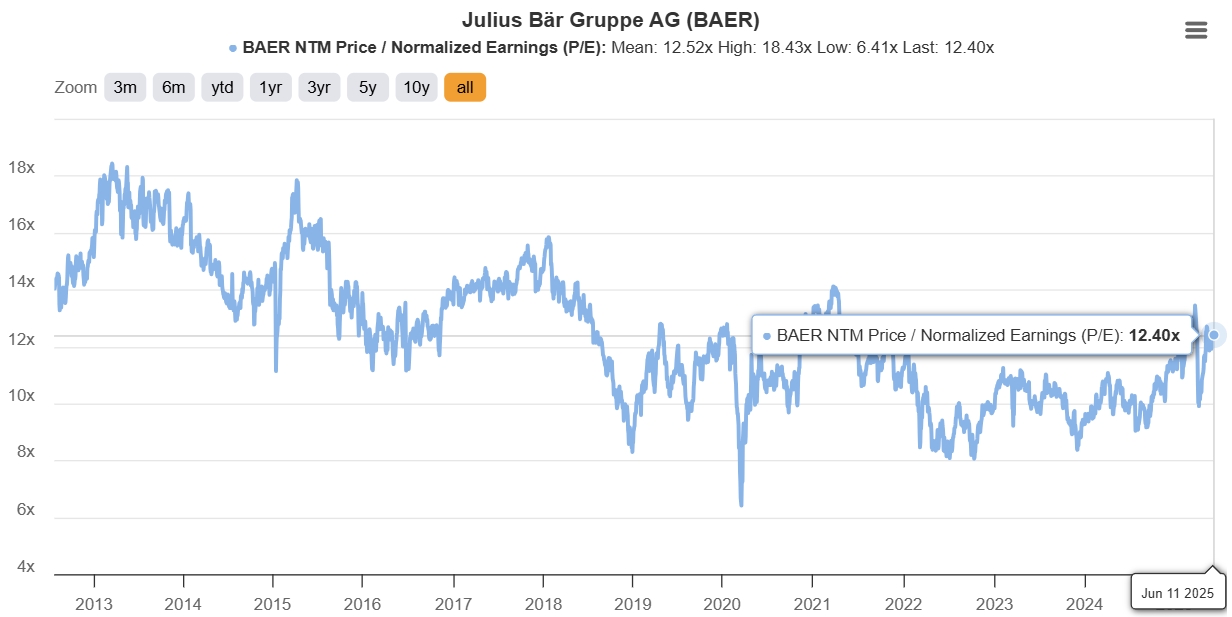

8. Julius Bär (BAER):

Swiss wealth manager with brand moat among private clients. At ~12x P/E, valuation reflects steady wealth flows and global asset growth, with modest upside if markets remain favorable.

9. Swiss Life (SLHN):

Life insurance and pension management leader, with distribution and captive client base. Trades at ~18x P/E, elevated versus historic norms (around 11-12x), reflecting higher margins and fee-based income streams.

10. Swisscom (SCMN):

Swiss telecom giant with quasi-monopoly moat. Now ~21x P/E, rich for a slow-growth telco historically trading around 16x. Investors pay for safety and yield but limited growth upside at this valuation.

11. Richemont (CFR):

Luxury group behind Cartier, Van Cleef, etc., protected by brand and heritage. Trading at ~25x P/E, right in line with its long-term premium valuation. Quality rarely comes cheap.

12. Logitech (LOGN):

PC peripherals and gaming gear leader. Now trading at ~20x P/E, roughly in line with its historical average after the post-pandemic normalization. Whith cyclicality, the current valuation offers continued upside if secular trends in gaming, remote work, and video collaboration continue.

13. Swissquote (SQN):

Swiss digital bank and trading platform with fintech scalability moat. Trades at ~23x P/E, pricing in strong recent growth, but not excessively rich for a growing platform. Interesting to watch.

14. Holcim (HOLN):

Global cement and building materials leader with vertical integration moat. Now trading ~15x P/E, in line from historical 14x levels.

15. Givaudan (GIVN):

Global number one in flavors and fragrances, with moat in proprietary formulas. Now at ~32x P/E, slightly above its long-term average of 28x, still expensive but reflecting a better business last years.

16. SGS (SGSN):

Global leader in testing and certification. Trading at ~22x P/E, below its 23-24x norm. The multiple compression could offer long-term upside for this cash-generating defensive player.

17. ABB (ABBN):

Global automation and electrification giant with installed base moat. Trading ~22x P/E, elevated vs. historical high-teens. Market prices its shift toward higher-margin automation.

18. Sika (SIKA):

Specialty chemicals leader with patents and global reach. Trading at ~26x P/E, lower than prior 35-40x highs. Investors get a fair historical valuation and consistent growth.

19. Alcon (ALC):

Ophthalmology leader post-Novartis spin-off. Valued at ~28x P/E, fairly consistent with its post-IPO mid- to high-20s range. Market pricing steady eyecare growth.

20. Partners Group (PGHN):

Global private equity manager with sticky institutional base. Trades at ~23x P/E, slightly below its previous +25× norm, reflecting recent market caution in private markets.

21. TE Connectivity (TEL):

Specialized electronics and sensors with deep OEM integration moat. Now at ~19x P/E, a fair multiple for stable earnings streams and long-term automotive and industrial tailwinds.

22. Garmin (GRMN):

GPS device maker spanning fitness, aviation, marine, and automotive sectors. Trading at ~26x P/E, higher than historical norms (18–20x), as recurring software and premium segment growth have raised the multiple.

23. The Swatch Group (UHR):

Luxury watchmaker with vertically integrated moat. Now ~23x P/E, far lower than prior trailing multiples inflated by profit drops, but still elevated relative to its cyclical history. Market is cautiously optimistic on China rebound, but it is an interesting luxury brand to follow.

24. Lindt & Sprüngli (LISN):

Prestigious chocolatier with brand moat. Now at ~42x P/E, still one of Switzerland’s priciest stocks, slightly above its historical 35–40x range. A pure quality compounder trade.

Where Are the Real Opportunities?

Let’s be clear: Switzerland rarely offers deep value.

Most of these stocks are premium businesses priced accordingly. But markets fluctuate, and even the most stable compounders occasionally open windows for disciplined investors.

After reviewing the updated valuations, these are the 5 setups that, in my humble opinion, stand out and deserve a closer look:

1️⃣ Roche (ROG): The Underappreciated Pharma Titan

NTM P/E: ~13x.

Why? Patent cliffs have created fear, but pipeline remains rich (oncology, immunology, diagnostics).

Historically trades in mid-teens P/E, this is cheap for Roche.

You collect a safe 3.5% dividend while waiting for R&D to deliver.

Global leader with enormous cash flow stability.

👉 Roche is one of the few global mega-cap pharma names trading at an actual discount today.

2️⃣ Swissquote (SQN): The Quiet Fintech Compounder

NTM P/E: ~23x.

Growing leader in Swiss digital brokerage.

Significant expansion optionality into crypto, options, and EU expansion.

Solid profitability, high scalability, still below valuations of global fintech peers.

Switzerland’s regulatory environment remains an edge.

👉 Still under the radar globally, one of the rare scalable Swiss growth stories.

3️⃣Logitech (LOGN): Back to Reasonable Levels

NTM P/E: ~20x.

Pandemic boom is over; demand normalized.

Cash-rich, strong gaming & hybrid work tailwinds.

Priced on its mean with a very stable growth.

Optionality remains in gaming peripherals, video collaboration, and esports.

👉 You’re buying a dominant cash machine at a fair price for the long run.

4️⃣ Partners Group (PGHN): Private Equity On Sale

NTM P/E: ~23x.

Private markets have cooled but long-term AUM growth remains intact.

Sticky institutional capital base provides visibility.

Historically trades ~25–27x, this is modestly cheaper.

Optionality on global alternative assets rising in coming decades.

👉 For those who believe private markets will remain strong, this is one of the best public ways to gain exposure.

5️⃣ Swiss Re (SREN): The Reinsurance Cycle Play

NTM P/E: ~12x.

Underwriting is stabilizing after a rough few years.

Rising pricing power in a harder reinsurance market.

Historically trades around 13–15x when normalized.

Cyclical tailwind + improving fundamentals.

👉 A classic "buy quality cyclicals when hated". Not my approach though.

🧭 Conclusion:

Switzerland remains one of the world’s most fascinating public equity markets for disciplined long-term investors.

Moats? Extremely strong.

Balance sheets? Mostly fortress-like.

Volatility? Lower than global peers.

Valuations? Selectively interesting in 2025.

True deep value? Rare.

But if you’re playing the long game, some of these franchises offer you exactly what Swiss investing has always promised: quality that lets you sleep at night, and compound for decades.

🚀 Coming soon on the Substack:

👉 In upcoming posts, I’ll cover:

A full deep dive on one of the Top 5 Swiss companies highlighted in this article (free).

How to optimize taxes when investing from Switzerland, a huge advantage vs US & EU (free).

Continued deep dives on asymmetric opportunities I’m tracking, including my recent Azeus write-up (free).

The “move to Switzerland” playbook for investors and entrepreneurs (paid).

My personal Swiss allocation strategy, which has returned 40% this year and 25%+ CAGR over the past 5 years (paid).

Disclaimer

These opinions are solely those of the individual author. The content of this material is provided for educational purposes only and does not constitute investment advice. No discussions herein should be interpreted as an offer to sell or a solicitation to buy any securities of any company. All information is subjective, and readers are encouraged to conduct their own due diligence.

Swiss Transparent Portfolio makes no representations, warranties, or guarantees, whether express or implied, regarding the accuracy, reliability, completeness, or reasonableness of the information provided in this material. Any assumptions, opinions, or estimates expressed reflect the author’s judgments as of the date of publication and are subject to change without notice. Any projections included are based on various market condition assumptions, and no assurances can be made that the projected outcomes will be realized.

Swiss Transparent Portfolio disclaims any liability for direct, consequential, or other losses resulting from reliance on the content of this material. Swiss Transparent Portfolio does not serve as your financial, legal, accounting, tax, or other adviser, nor does it act in a fiduciary capacity.

⚡ If you enjoyed the post, please feel free to share with friends, drop a like and leave me a comment. I will thank you for that.

You can also reach me at: X→ @SwissTportfolio

If you enjoyed this, a follow and a share go a long way to support my work. I’ll continue sharing deep dives on asymmetric opportunities. I focus on compounding businesses, smart capital allocation, and tax-optimized investing, with a long-term lens. To stay updated, just subscribe below ⬇️.

Thanks for sharing. I am really enjoying these articles!

Congrats for the great quality content, I still think you’re underrated. I followed you on $PSIX and was lucky to double so far, very grateful for you sharing the idea. Please keep posting, I’m definitely looking forward to your next deep dives and very interested in the "move to Switzerland" playbook :)